Alex

2.5K posts

Alex

@diyreturns

Here to learn, banter and enjoy the ride. Appreciate optimism. Prefer to be roughly right than precisely wrong.

Katılım Nisan 2020

174 Takip Edilen208 Takipçiler

@diyreturns 3×$62.1M F-15Es = ~$186.3M

1×$79M KC-135 = ~$265.3M

12×$34M MQ-9s = ~$408M

Total: ~$673.3M in aircraft losses.

English

Using a lower-bound estimate for the manned aircraft and $34M × 12 for the MQ-9s, you’re already around $673M in aircraft losses alone. Most important, six American airmen were killed in the KC-135 crash. Whatever your view of the war, this is not remotely costless or bloodless. Not to mention the other lives lost and the cost of missiles and munitions.

OSINTdefender@sentdefender

The U.S. Air Force has lost over a dozen MQ-9 “Reaper” Surveillance & Attack Drones to enemy fire so far during Operation Epic Fury, with the drones lost to either Iranian surface-to-air missile fire or destroyed on the ground by ballistic missile and drone strikes, two U.S. officials confirmed to ABC News.

English

Apparently the trend on X is to either talk at length about your Claude Code process or pour cold water on AI coding in general. I thought I'd try a new spin on the genre by simply sharing my results. portfoliocharts.com/2026/03/15/por…

English

@aaron_lancaster $ELM if you believe in their approach - just one ticker

English

Is there a role for tactical asset allocation in a DIY portfolio or do the added complexity, tax and other costs outweigh the benefits? Meb Faber advocates for it & implements one in his Trinity ETF, but does it make sense for individual investors to apply it themselves?

English

@TipsWatch Thanks for the gift link.

A piece of propaganda devoid of meaningful data. Just the typical NY Times hating the rich who pay the most in taxes. Yes, we can find a way to make it a bit more fair (eliminate step us basis), but this stuff is just a political attack

English

Today's "must read" article to make your blood boil, especially if you are still working on your taxes: nytimes.com/2026/03/15/bus…

English

@aaron_lancaster Nice. He is certainly different in a good way from the standard finance podcast.

English

@diyreturns I have! I've listened to all 492 episodes and have learned a ton. It is currently my favorite podcast. :)

English

When I first got into rental real estate, I was convinced it was the only realistic way to live off my portfolio. I couldn’t psychologically stomach the idea of selling shares to fund my life. Rentals felt safer and more “real.” That view has completely changed.

English

@aaron_lancaster Have you heard of risk parity radio podcast? The author has several test portfolios like that. And you might like it in general

English

But still, it’s been an interesting real-world experiment and it’s given me a feel for the withdrawal phase psychologically. I’m keeping the experiment running and will post occasional updates here on how it’s performing.

English

@aaron_lancaster How confident are you in taking seriously SP 500 performance numbers for 1885?

English

If you could have invested $500k in the S&P 500 and $500k in Treasury bills in 1885, and withdrew $40k per year until 2026, you’re portfolio would have never depleted and would be worth $21 million in today’s dollars (adjusted for inflation).

English

@GeorgeKamel This is misleading to put it mildly.

Because nobody cares many digits is in your band account, but how many cars, houses, trips and doctor’s appointments you can actually buy with those digits.

Money is to buy things

English

@diyreturns We’re not talking inflation adjusted returns. 10% is 10%. 1 million in a 401(k) is 1 million. Regardless of purchasing power.

English

The S&P 500 having an annual average return of 10% over the last 30 years isn't my opinion, it's a fact. Google it, I dare you!

Instead of trying so hard to time the market, just spend time in the market. Stop buying and selling based on headlines and fear mongering, and make sure you're invested in good growth stock mutual funds. Building wealth is a marathon, not a sprint.

English

@MeasureTwiceMNY @GeorgeKamel For the love of god and everything financially sounds, I beg you to stop talking about returns in nominal terms.

English

@GeorgeKamel And the S&P 500 index has never had total annualized returns below 8.5% over any 30-year period.

No guarantees of future results, but it has a pretty stunning record over the past 100 years.

English

@egr_investor That’s a very good point. We are fortunate to have many tools at our disposal- no need to push into every nook and cranny of financial obscurity. Don’t understand it - don’t invest in it

English

@diyreturns I won’t go as far as saying there was anything wrong with his motives, but I have always stayed away from funds like this because they exceed my capacity for proper due diligence.

English

I remember @larryswedroe being very big on this private credit fund. I wonder what his thoughts are now

Nick Nemeth (Mispriced Assets)@NickNemo17

$CCLFX. $32.5 billion. The largest interval fund in America. In 2021, ZERO borrowers were paying interest in IOUs. By September 2025: 188. And they thought: no losses, no redemptions. Read this. Cliffwater tells investors: "96% first-lien senior secured." "10% distribution yield." "Minimal losses." I parsed every position in their N-CSR filings on SEC EDGAR. All of them. I cross-referenced borrower names across every semi-annual filing. At least 53 borrowers were cash-pay in earlier filings. They used to pay cash interest. Then they couldn't. The loan was amended to PIK to avoid a technical default. Amend and extend. Cliffwater marks most at par. $1.24 billion. Five names that tell you everything: 1. WEALTH ENHANCEMENT GROUP — manages $136B in client assets. Can't service interest on its own subordinated debt. Holds a $23M tranche at 15% PIK — zero cash on that tranche. CW blended mark: 82c. My mark: 42c. The wealth managers can't manage their own leverage. 2. APEX SERVICE PARTNERS — HVAC rollup, 200+ companies, 43 states. Was cash-pay 2021-2024. Now holds 14.25% PIK sub-debt tranches paying zero cash. CW: 90c. My mark: 39c. Your AC repairman's parent company is paying its subordinated lenders in IOUs. 3. CPF DENTAL — dental chain. SOFR + 9.25% plus a 4.25% PIK component. All-in rate: ~18%. Maturity: December 31, 2025. The loan was due three months after the filing date. CW marked it at 99.7 cents. My mark: 64c. 4. PPV INTERMEDIATE HOLDINGS — healthcare. The name is the evidence: "Intermediate Holdings" = structural subordination. Sub debt. 13.75% PIK tranche, zero cash. CW: 97c. My mark: 37c. Behind SBA loans, revolvers, equipment lenders, tax liens, pension obligations, and every operating company creditor. Sixty cents of overstatement on a tranche paying nothing. 5. iCIMS — HR tech/SaaS. Was cash-pay from Mar 2022 through Sep 2024 in every filing. Now 10.07% PIK. The software company can't pay its interest bill. CW: 96c. My mark: 84c. Generous. Very generous. Even with a modest haircut, that's a confirmed credit event they won't recognize. The playbook: Borrower can't pay (SOFR went 0% to 5.3%) --> Amend to PIK (no default recorded) --> Extend maturity --> Mark at par (97% Level 3, no market price, Cliffwater sets its own marks) --> Book PIK as income ($57M of PIK interest in six months ended Sep 2025 alone) --> Collect fees Why they do it — the incentive: Cliffwater charges a 1% annual management fee on net assets. At $32.5B, that's $325 million a year. Every dollar of markdown reduces the fee base. Permanently. The incentive to not mark down is $325M/year. And here's the fund-of-fund layer they don't talk much about: six of their top ten holdings are CLOs, BDCs, and fund vehicles that charge their own fees underneath. Silver Point CLO ($1.4B), Barings Private Credit Corp ($919M), BlackRock Shasta CLO ($600M), Golub Capital, Blue Owl, AGTB. Your grandmother is paying Cliffwater 1% to invest in other funds that charge another 1-2%. Fees on fees on fees. On assets marked by the people collecting the fees. Cliffwater reports a non-accrual rate of 0.42%. I identified at least 53 borrowers that converted from cash-pay to PIK — borrowers that stopped paying cash interest. That is not 0.42%. That is systematic restructuring to avoid classification. Amend the loan before it hits non-accrual, and the number stays low. "First-lien senior secured" — on hundreds of holdco/intermediate/bidco positions, the collateral is equity of the subsidiary. Not the factory. Not the receivables. Not the cash. In liquidation: IRS eats first. Pensions eat. SBA eats. Revolvers eat. Equipment lenders eat. Employee claims eat. MCAs eat. Trade creditors eat. Then maybe the holdco "first lien" gets the scraps. They call that 96% senior secured. 97% of this fund is Level 3 — no observable market price. Cliffwater determines the value. Cliffwater collects the fees. Cliffwater reports the yield. And investors see 10% distributions and think it's safe. Remember that they went after unsophisticated investors. Retirement accounts. Your grandmother's financial advisor put her in this. First out gets the most out due to Cliffwater's bogus marks. Redemption requests just hit 14% in Q1 2026. The fund caps quarterly repurchases at 7%. This is the beginning. Every data point from their own N-CSR filings on EDGAR. CIK 1735964. Verifiable.

English

@egr_investor @larryswedroe I guess you always have to question motives

English

@diyreturns @larryswedroe Swedroe was the first thing I thought of when I saw this post.

English

Taxes can be considered a secondary consideration in planning.

Instead, the priority should be your life goals.

If paying taxes gets you to your life goals (like buying that next house), then doing so makes sense.

English

@PittsburgWizard @SchizoLLC @asymmetricinfo You should really look into public sector unions if you care about corruption

English

@diyreturns @SchizoLLC @asymmetricinfo Having a class of people that can corrupt any government from state to federal to across the planet is deeply authoritarian and obviously needs to be put in check.

English

I suspect that Washington State will see more capital flight from the millionaire income tax than they would have from a broader income tax even if the top rate was the same, because the signal it sends is “You are the only people we are willing to tax. Get ready.”

English

@PittsburgWizard @SchizoLLC @asymmetricinfo As usual, the claims are about helping the poor, the actual practice is about hating the rich

English

@SchizoLLC @asymmetricinfo Reducing the amount of money rich people have to corrupt our government is good. I’d love for California to be more efficient in the usage of tax dollars. Capping the rich is a good by itself.

English

As a lifelong Floridian, it’s amusing to see a place go from being universally mocked by the business and cultural elite for hanging chads and Florida Man to becoming the shining example of good governance.

That said, it’s sad (and a bit cowardly) to see so few of our famous newcomers acknowledge the real reasons why they’re uprooting their family offices and businesses and social lives after years of exporting West Coast morality to everywhere but here.

Just admit why you’re coming. No one is moving here for the weather.

English

@HedgeDirty As usual, the claims are about helping the poor, the actual practice is about hating the rich

English

People need to start recognizing that this is *the point* of wealth taxes. The people that propose them are fine with making everyone poorer and shrinking the tax base if the payoff is that anyone with the ability to challenge their dominance flees elsewhere

Megan McArdle@asymmetricinfo

Norway saw a massive exodus just from slightly raising its wealth tax. I don’t understand why people were so sanguine.

English

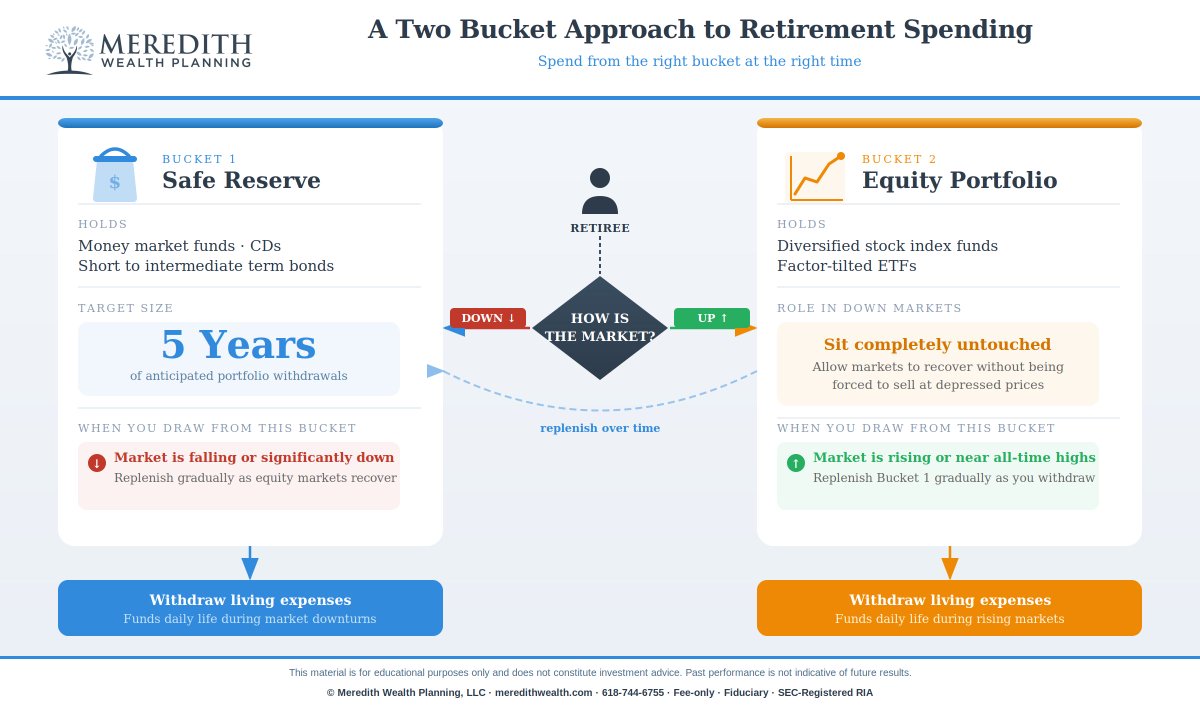

@MarkTMeredith Is this any different from 80/20 (4% withdrawal rate) portfolio?

English

I've always liked the two bucket strategy for retirement spending. It is not perfect, but it is very good.

English