E_Hendō

2.6K posts

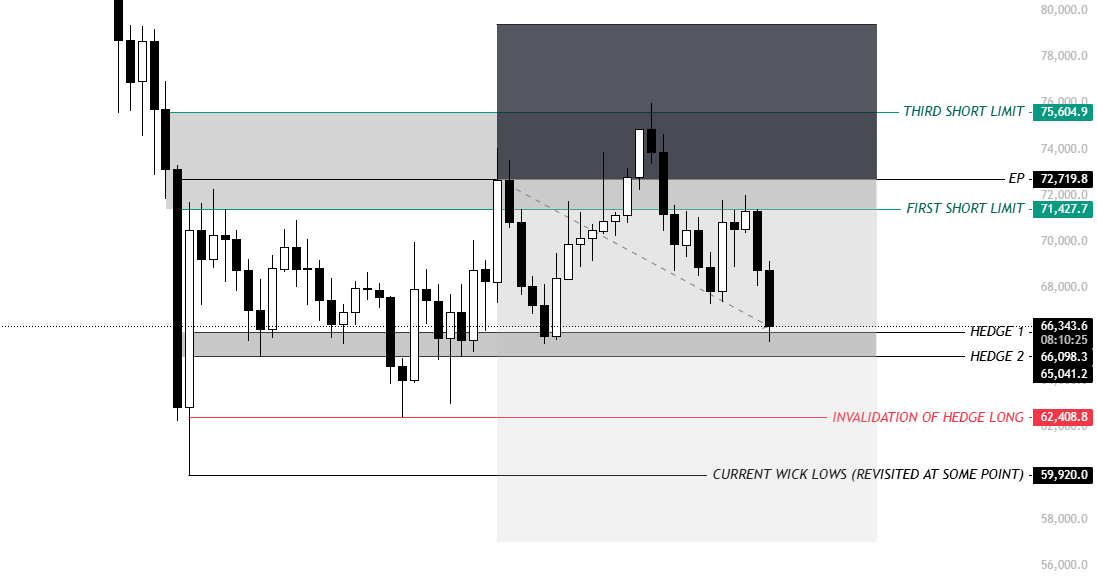

$BTC Just to reiterate, I am still short, nothing has changed. This is a HTF position, and I expect it will take time to develop. I am not aiming for a direct move to the 60s, but rather chop/bleed within a range. My current short could take 1–3 months to play out, and I am prepared for that. As I’ve mentioned before, I twap in and out of my positions in certain areas to compound gains within the range. Yes, we may see additional hunts or roundtrips, but the market remains range bound until proven otherwise, and the overall trend is still bearish until confirmed otherwise.

I am honored and grateful to be appointed by President Trump to the President’s Council of Advisors on Science and Technology (PCAST) and to be named Co-Chair along with OSTP Director Michael Kratsios. PCAST is the principal body of external advisors tasked with shaping science, technology, and innovation policy for the President and the White House. Thirteen of the world’s most accomplished leaders in science and technology will join us as this PCAST’s initial members. Together we will make policy recommendations to ensure that America leads—and wins—in artificial intelligence and other cutting-edge technologies. I look forward to working with the initial members: Marc Andreessen, Sergey Brin, Safra Catz, Michael Dell, Jacob DeWitte, Fred Ehrsam, Larry Ellison, David Friedberg, Jensen Huang, John Martinis, Bob Mumgaard, Lisa Su, and Mark Zuckerberg. Thank you to President Trump for his visionary leadership on technology policy which attracts the top luminaries in their fields to serve. It is an honor to be part of this distinguished group.

New position opened in small cap stock in new thematic basket at whop.com/stocktalk

@JoshMandell6 @CedYoungelman Sorry my brain is not catching up even after asking Grok about your answer @JoshMandell6 😅 I think I am almost there but can you clarify “the two products put together” I see your pov and cap the BTC accumulation, but I am still unsure🤔

I'm sorry to all my CT followers that by buying a $IBIT at 69420 equivalent. I essentially destroyed all future price volatility. Perhaps I will sell just so it can move again.