I think you are misreading the document, The bond exchange proposal was to exchange old unsecured notes for new second lien secured notes. (which never happened obviously)

Go to Page 4 where the Red text is

Sauce :

sec.gov/Archives/edgar…

I was reading through old $BBBYQ SEC filings and came across something that really stood out. whatever the intentions of the affiliates and/or Purchaser, the assets had to have been secured at the end of 2022 in some way.

think back to the private bond exchanges; there was first a single investor, then an institutional group that followed by retiring their bonds for shares some time between November 14 and December 6, 2022. here is what I had never caught before:

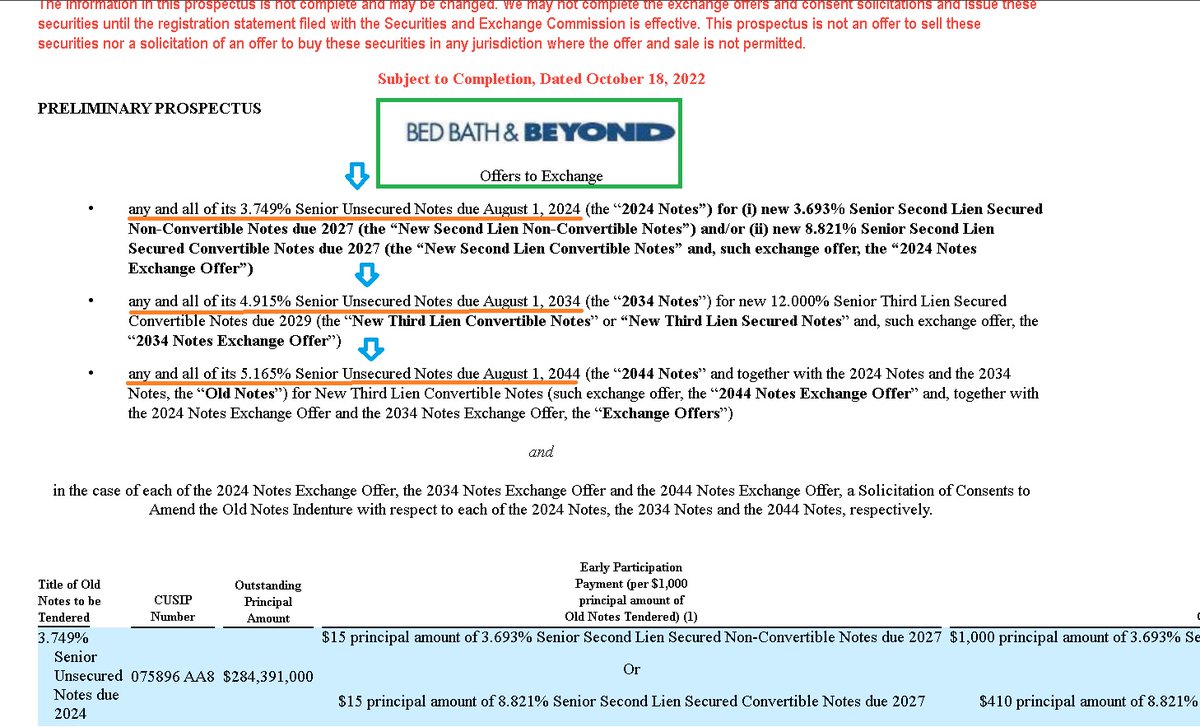

[image 1]

thanks to accounting requirements there is disclosure in the 10-Q that the exchange was performed under what is called a "troubled debt restructuring". that can only be used under very specific circumstances, say if a company discloses that it may not be able to continue as a going concern. if we dive into the math on the deal we will see that whoever participated in the exchange was friendly to the company. here's why:

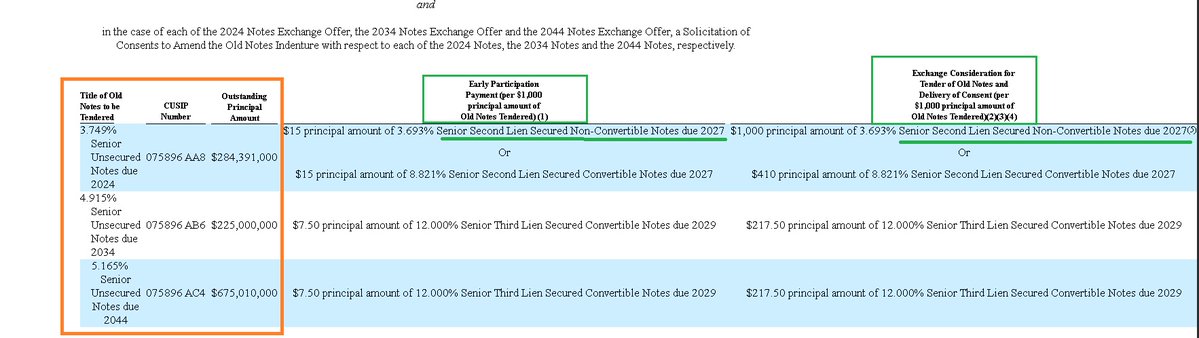

[image 2]

the aggregate principal amount retired through the bond exchange:

69.0 (2024) + 15.3 (2034) + 70.2 (2044) = 154.5 million dollars worth of bond debt.

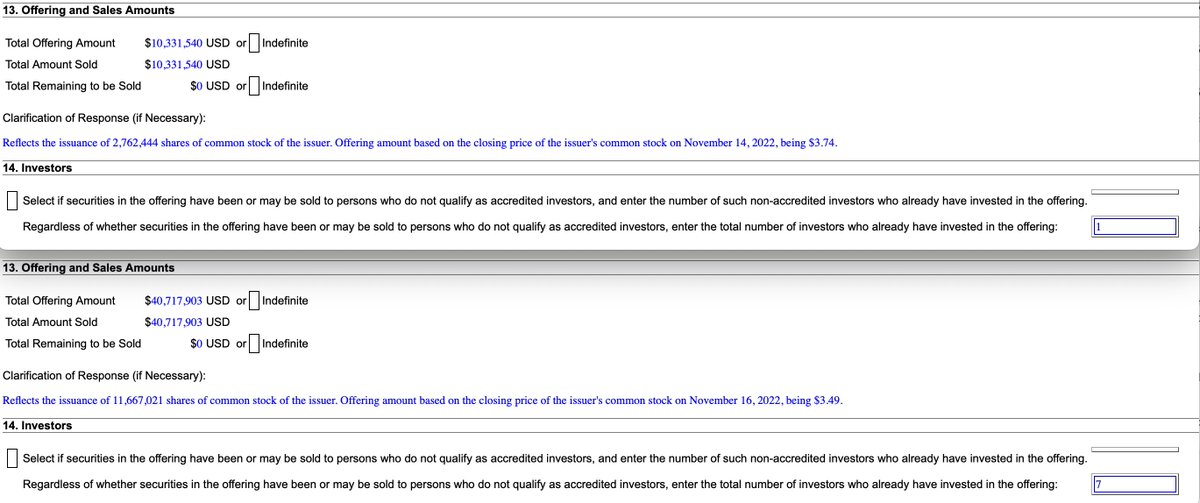

[image 3]

but investors only received:

first Form D: 2,762,444 shares which was an offering amount of 10,331,540$;

second Form D: 11,667,021 shares which was an offering amount of 40,717,903$;

10,331,540 + 40,717,903 = 51,049,443$.

[image 3]

154.5 million of debt was retired in exchange for 51 million dollars’ worth of shares. the bond holders exchanged at 0.33 on the dollar when they could have just sold them on the open market at the time for a better return plus the individual investor gave the Company another 3.5 million dollars cash for 0.9 million additional shares.

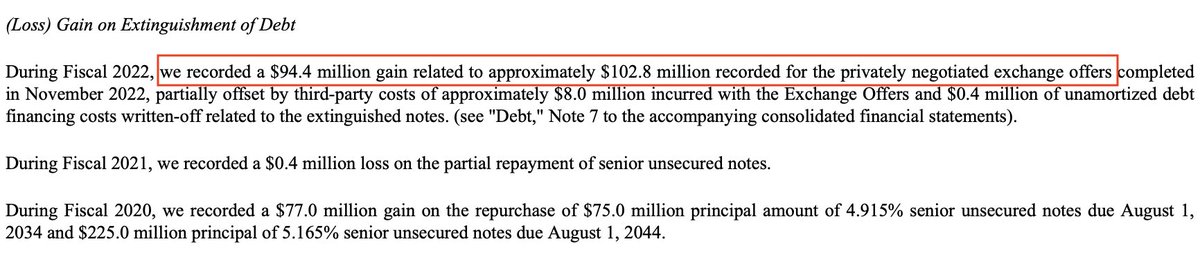

the Company obviously benefitted tremendously from this deal, recording a 94.4 million dollar gain (the net difference) on their 10-Q. who would do that? the only way it makes sense is if the former bond, then equity holders received something more than just the shares in return. the only alternative explanation is preferring to lose money over open market sales to help the Company.

[image 4]

fun little side fact, looking at the TSO from the 10-Q (which was late!) if you look at the share amount received by the institutional group they total 9.9444% ownership, just under 10% with no way to round up to 10% and be labelled an insider. two more fun facts, the Company filed that their 10-Q was going to be late on the same day the bond exchange was finally terminated with no more extensions, and, the "troubled debt restructuring" was only revealed in the 10-Q itself, over a month later.

to summarize: no investor retires their senior, secured debt instrument for junior, unsecured equity at a loss compared to open-market price to help the Company's balance sheet, unless they got something in return. this exchange retired 25% of all 2024 bonds, an imminent insolvency risk at the time.

so.. what did they get?

@dirtevader It has been very disappointing how many people over the last few years have turned out to be shills, neurotic as hell or completely retarded.

@markt83101520 Today is also last day of trading in BBBYQ timeline (tenet theory). So no surprise proxy filed today, and gives the vote on July 7th which gives us this window for all this to happen.

Assuming Ryan wants the yq cash to show up on their earnings balance sheet, that means we need the waterfall before June 9th. It also means acquiring and merging BBBY before since that is the step orior imo. No wonder BBBY started running, we going to 100 mf'ers

I will be voting

✅ YES to everything proposed by the GameStop board

The only people voting NO are frustrated and emotional, and have lost faith and confidence in their investment.

I trust Ryan is aligned with shareholders.

I trust him to take this rocket to $100bn M/C 💥