@ChartGuys This is why we are here, the OG Chart Man! - sometimes when you lose your confidence, you can lose your talent. Keep it - it's hard not to be confident when you are the best.

English

Eli Chase

275 posts

You need to have a high degree of mental illness to be trading this market

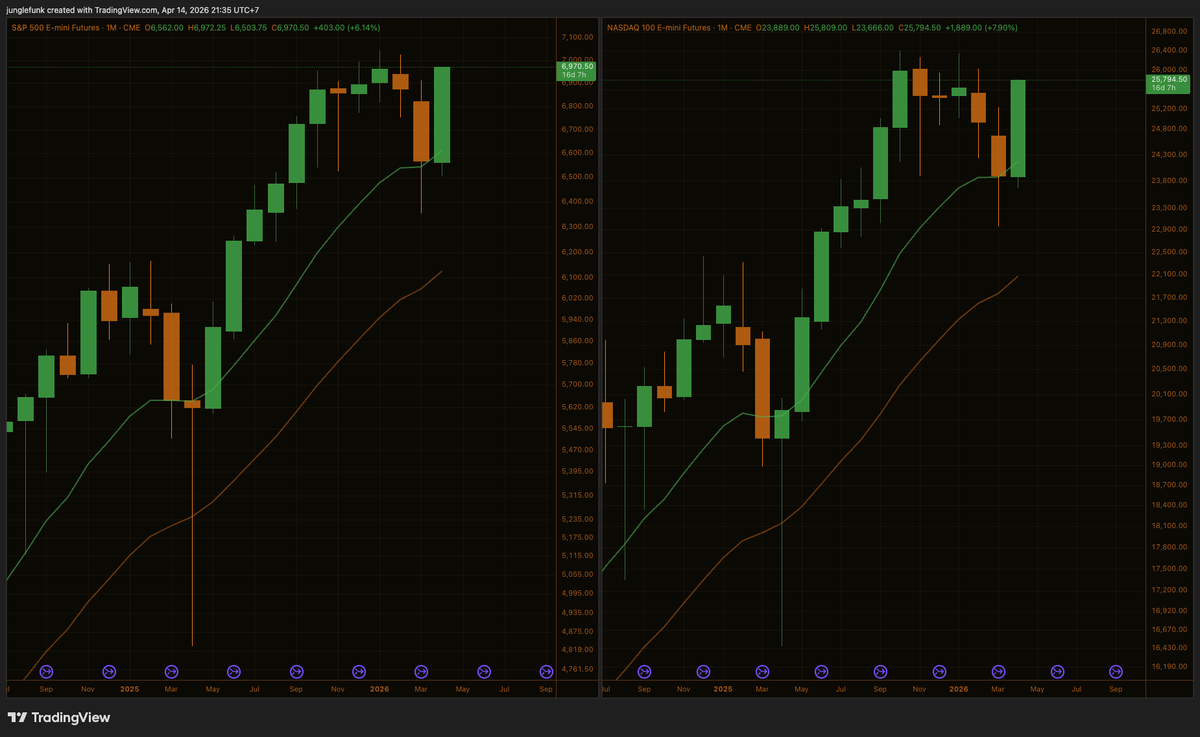

What if $ES and $NQ are monthly bull flags clean off of 12ema? $SPY $QQQ

I want to die completely broke. When I tell people this, I usually get one of two reactions. Either they assume I’m joking, or they assume I’ve lost my mind. Sometimes both. So let me clarify before anyone forwards this to a financial planner in panic. I don’t mean reckless. I don’t mean irresponsible. And I definitely don’t mean unprepared. What I mean is that I don’t want to die having optimized my entire life around a number that only matters when my ability to actually use it is gone. We talk constantly about the time value of money. A dollar today is worth more than a dollar tomorrow because it can be invested, compounded, and put to work. Time increases its potential. Life, however, works in the opposite direction. Time doesn’t increase the value of experiences – it usually decreases it. Certain experiences are simply more accessible, more enjoyable, and more meaningful at specific stages of life, and no amount of money later can fully replicate them. When you’re younger, you’re sitting on an asset that quietly depreciates every year: health, energy, physical capability, curiosity, and a tolerance for discomfort. A dollar at 35 buys a fundamentally different life than a dollar at 75. Pretending otherwise is comforting, but it’s not honest. Life has a time value too, and it doesn’t compound. When people hear “die broke,” they often picture irresponsibility or excess. That’s not what I’m describing. I’m talking about intentional depletion – using money as a tool to maximize life while you’re able to live it, rather than stockpiling it indefinitely for a future version of yourself that may not exist in the way you imagine. Saving matters. Security matters. Optionality matters. But past a certain point, additional saving delivers diminishing returns while the cost of waiting keeps rising. Saving for retirement makes sense. Over-saving at the expense of living doesn’t. We’re taught to treat retirement as the main event – sacrifice now so you can enjoy later. Delay life so you can eventually live it. But that framework assumes a lot: that your health cooperates, that your energy remains, that your relationships are intact, and that your interests don’t change. Most of all, it assumes experiences are interchangeable across time. They aren’t. The trip you take at 35 is not the same trip at 70, even if it’s first class. Skiing with your kids, traveling with friends, pushing your body, starting something new – these things are perishable. They don’t age gracefully, and postponing them doesn’t preserve value. It destroys it. There’s also a strange moral judgment baked into personal finance culture that equates delayed gratification with virtue and present enjoyment with failure. I don’t buy that. There’s a meaningful difference between consumption that disappears and spending that compounds in memory, perspective, relationships, and confidence. Experiences don’t show up on a balance sheet, but they pay dividends in ways that money never can. Your memories are what matter in the end, not your net worth. This way of thinking has also changed how I view legacy and what I want to give my kids. I don’t care about leaving behind generational wealth the way I once did, especially not as a lump sum that shows up only after I’m gone. If I’m going to give them anything meaningful, I’d rather do it while I’m alive – when it can actually shape who they become. I want to use my resources earlier to give them experiences, exposure, and tools that help them build confidence, curiosity, and resilience. Travel that broadens perspective. Opportunities that stretch them. Lessons about money, risk, work, and independence learned through experience, not inheritance. I want them to understand how to create value, how to adapt, and how to rebuild if things fall apart. I still want to leave them with enough. But “enough” isn’t a massive number waiting at the end of my life. Enough is a foundation, plus the skills to stand on their own. Unlimited money can become a crutch. Capability is freedom. I’d rather they inherit confidence than comfort – and I’d rather be around to help them learn it than hope they figure it out after I’m gone. Everyone talks about the risk of running out of money. Almost no one talks about the risk of running out of time. And even less people talk about the tragedy of wasting valuable hours of your youth working for money that will never get spent. What a waste of your valuable time. We’re very good at smoothing consumption – using money, planning, and credit to keep life stable while quietly deferring the things that actually make it meaningful. From the outside, everything looks fine. Under the hood, life is being postponed. The biggest gamble isn’t that you won’t have enough someday. It’s that someday arrives and you’re no longer capable of the life you spent decades planning for. I want to die broke not because I don’t value money, but because I value life more. I want to use my resources to create memories while they’re available, not just affordable. To save enough to be secure, but not so much that I defer living indefinitely. To leave my kids with a foundation, not a cage. I don’t pretend this is the right answer for everyone. I don’t even pretend it’s my final answer. But if the time value of money matters, then the time value of life matters more.

🔥 JUST IN: Standard Chartered raises $ETH forecast to $7,500 by end-2025 from $4,000, and to $25,000 by 2028.