Sabitlenmiş Tweet

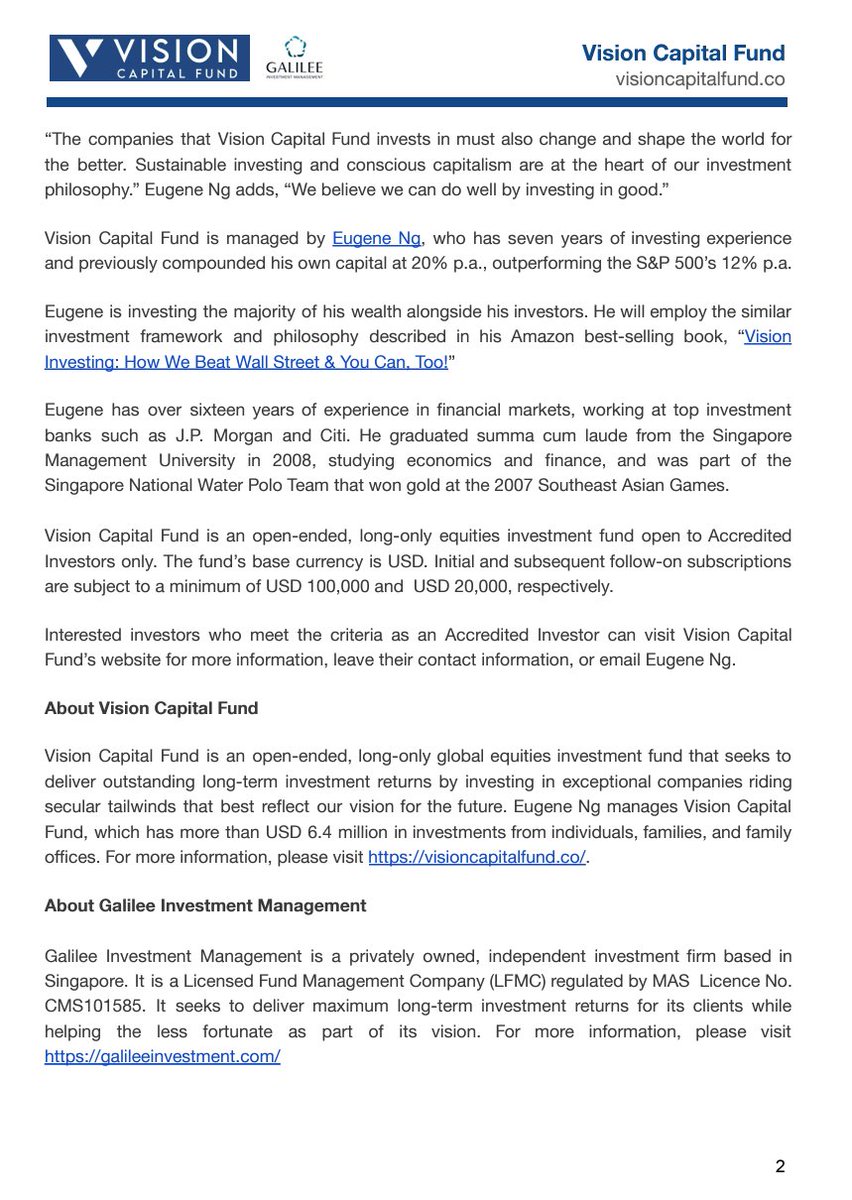

I am thrilled to announce the launch of Vision Capital Fund, which has been in the making for over seven years.

We are focused on growing wealth for generations by delivering outstanding long-term investment returns from investing in exceptional companies that best reflect our vision for our future.

Website: visioncapitalfund.co

Press Release: tinyurl.com/VCFpressrelease

Day One Investor Letter: tinyurl.com/VCFDayOne

English