Fifa Professor

4.1K posts

Fifa Professor

@fifa_professor

I suck at fifa, that why I overexplain

Zürich, Schweiz Katılım Aralık 2017

2K Takip Edilen181 Takipçiler

Wir (pokefy.de) verkaufen gerne in Europa. Und hören trotzdem damit auf.

Was kostet z. B. ein Paket nach Österreich? 14,50 € Porto.

Realität für uns als Gewerbetreibende: 135 € pro Paket bei gerade einmal zehn Sendungen pro Jahr nach Österreich 2025.

Dabei sind wir nur eine kleine GmbH aus Deutschland mit vereinzelten Kunden in Europa. Unser gesamtes jährliches Aufkommen für den EU-Export liegt bei etwa 100 Kilogramm Verpackung. Nicht Tonnen. Kilogramm.

Die Rechnung für Österreich allein: Wer als ausländisches Unternehmen nach Österreich verschickt, ist gesetzlich verpflichtet, die Entsorgung der Verpackung zu lizenzieren und dafür einen lokalen Beauftragten zu benennen, der die Einhaltung der Vorschriften garantiert und dafür haftet:

- Porto (10 Pakete à 14,50 €): 145 €

- Jahrespauschale Verpackungsbeauftragter: 450 €

- Notarkosten für die Vollmachtsbeglaubigung: 150 €

- Opportunitätskosten: 600 €

Und das ist nur Österreich. Frankreich verlangt z. B. ein eigenes Logo samt Anleitung auf jedem Versandkarton, sonst drohen empfindliche Bußgelder. Spanien, Italien, Polen: jeweils eigene Anforderungen, eigene Register. Ab Mitte 2026 kommen mit der EU-Verpackungsverordnung #PPWR weitere Pflichten hinzu.

Konzerne verteilen solche Fixkosten auf Millionen Sendungen. Für kleine Unternehmen und Selbständige wird daraus ein reales Exporthindernis. Das ist kein Versehen des Gesetzgebers, sondern ein struktureller Konzentrationsvorteil zugunsten großer Marktteilnehmer.

Dahinter steht ein System mit eigener Ökonomie: Wer Verpackungen in Verkehr bringt, muss deren spätere Entsorgung lizenzieren. Allein in Deutschland fließen dabei jährlich Milliardenbeträge an Lizenzentgelten an marktbeherrschende Entsorgungsunternehmen. Diese profitieren dabei mehrfach, über Lizenzgebühren beim Inverkehrbringen von Verpackungen über die Abholung und Verwertung der eingesammelten Rohstoffe. Komplexität ist dabei kein Fehler im System; sie ist Teil des Geschäftsmodells.

Besonders grotesk wird das im Vergleich mit Plattformversendern aus Fernost. Millionen Kleinsendungen fluten den europäischen Markt bei erkennbar geringerer Vollzugsintensität. Der europäische Mittelstand wird kontrolliert, weil er greifbar ist.

Der ursprüngliche Gedanke hinter der @EUCouncil war ein anderer: ein gemeinsamer Binnenmarkt, der Grenzen abbaut statt neue errichtet. Stattdessen: 27 nationale Compliance-Silos, die kleinen Unternehmen den Export systematisch verleiden.

Was sich ändern müsste:

1. Eine zentrale EU-Registrierung statt 27 nationaler Alleingänge

2. Eine De-minimis-Regelung für Kleinversender

3. Konsequenter Vollzug gegenüber Drittstaatsversendern statt Belastung des europäischen Mittelstands

Wir ziehen uns deshalb vorerst auf Deutschland und die Schweiz zurück, weil wir unsere Energie lieber in Produkte und Kunden investieren.

Die aktuelle EU-Bürokratiearchitektur erleben viele Unternehmen nur noch als Belastung.

Wir sind Unternehmer und keine Verpackungsjuristen, @vonderleyen , @DIHK_News, @MarkusFerber , @svenja_hahn , @nicolabeerfdp , @ANiebler

Gerne reposten - es betrifft den Mittelstand generell.

Deutsch

One performance tweet and people start confusing you for an AI bottleneck investor.

English

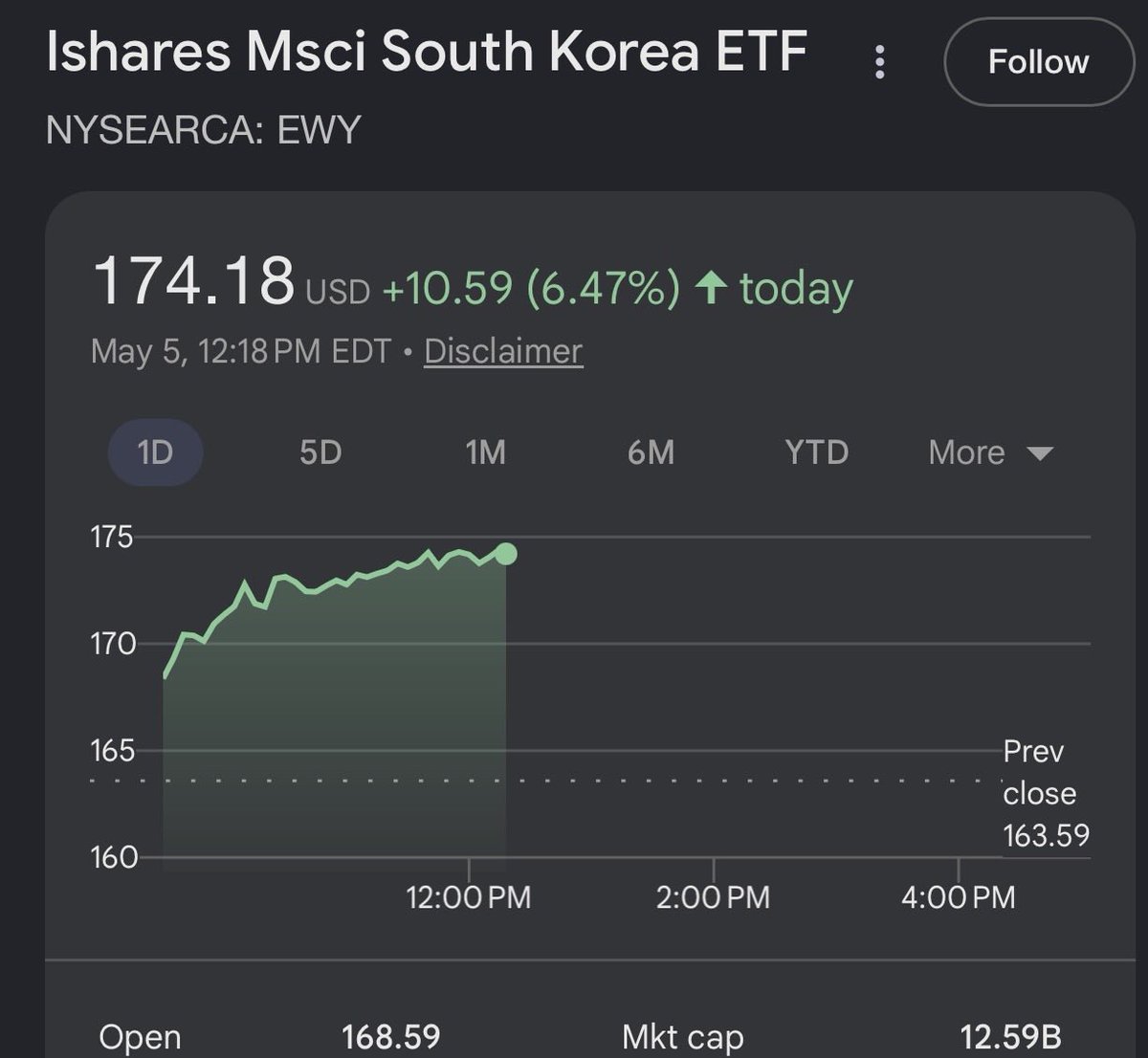

@ReneSellmann Have you seen the Korean stock performance after becoming available at ibrk?

Japanese AI buildout / semi related stocks doing super well, so it's actually more this theme vs the rest

English

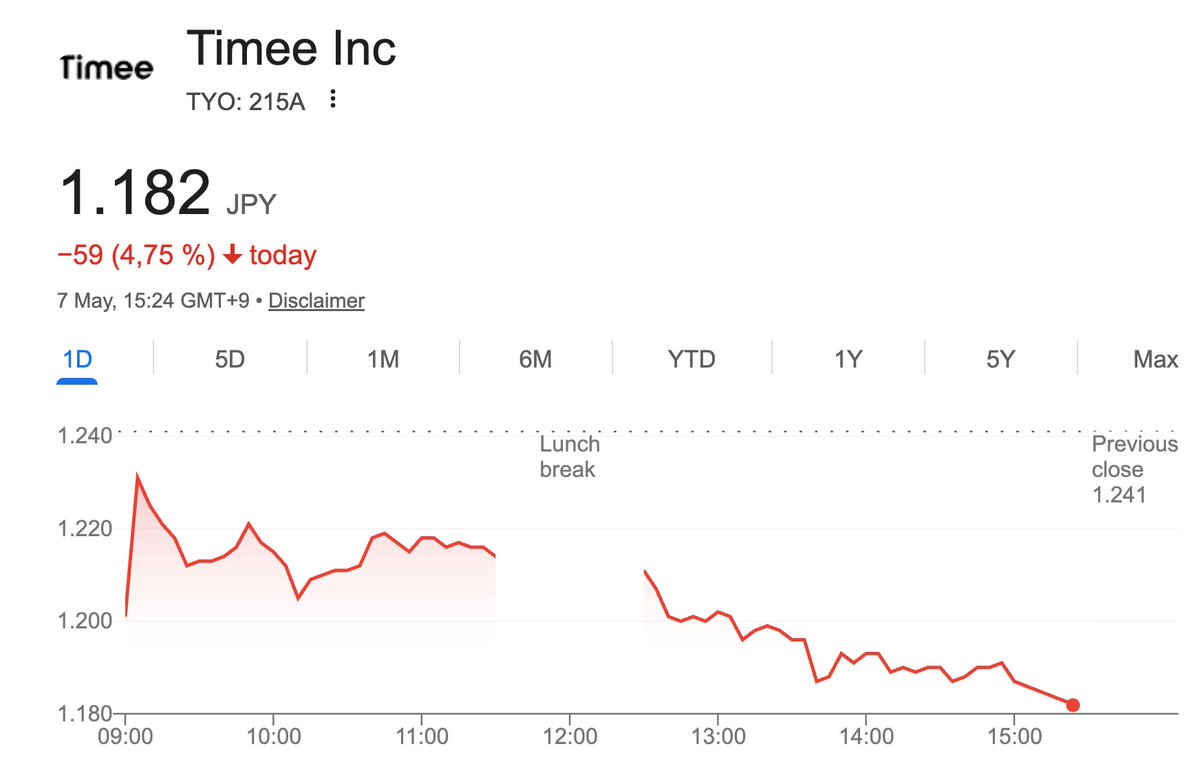

While US stocks 🇺🇸 are soaring, some Japanese stocks are struggling $NTDOY $7974 $215A

English

English

There’s probably a pod at millennium that just runs a strategy of front running @insane_analyst @jukan05 @aleabitoreddit & @zephyr_z9 tweets all day.

English

Here is how to work your way through the Anthropic puzzle:

Anthropic employs an individual named Pedram Navid, who has some job working as an influencer there.

In 2022, I was running a small business fixing up software and data engineering messes for different companies.

Pedram and his chaperones at VC firm Amplify Partners came after me and my business. They staged a whole phone and chat group game of getting people to cancel my LinkedIn account and boot me off of forums because my business was focused on cleaning up rat nests of code that were created by the products they promoted.

Pedram and Amplify Partners stole money from me, damaged my reputation, and came after me because:

a. My name

b. I was running a business cleaning up their messes

So Anthropic is at an en passant here, given that I move stocks around and a number of human and automated loops use these AI systems to trade these stocks. It is a mess, though they have plenty of money and resources to figure this out.

I can be forgiving of Pedram as an individual if he shows remorse and regret and I do believe he has grown up a bit, but this is a difficult situation for all involved given the recursion and the geopolitical factors.

Anthropic simply needs to do better, and more broadly we need to move toward a society where companies are not just pulling in random people from elsewhere in the world to come to the US to attack American businesspeople. This is all low trust nonsense. It makes me sick.

Until this is resolved, I expect Anthropic to remain behind OpenAI. It is up to them.

English

Long FAB (TSMC, Samsung, INTC, MU, SK Hynix, GFS, UMC, ON, TI) vs. Short FABLESS (AVGO, Qualcomm, ARM, AMD, NVDA, MediaTek)

Equal Weighted

Remind me in 12 months

English

Ich hab Claude nach den verlässlichsten Autos gefragt die man heute kaufen kann/soll und das hier hat er am Ende rausgehauen.

Stimmt oder stimmt nicht?

Deutsch

@TweetsOfSumit "Bereuen" kenne ich eher im Kontext von "selber bauen"

Deutsch

Gibts jemand der es bereut in Deutschland ein Eigenheim gekauft zu haben und würde lieber wieder Mieten?

Deutsch

Ex-JPMorgan banker files wild new claims - including lurid threesome invitation - days after viral with 'fabricated' sex slave allegations trib.al/7Waz3xk

English

@Biohazard3737 I feel like a lot of people on X who have been right about a lot of stuff recently seem to like Nebius. But it might all be the exact same trade

English

Scott Jennings claimed I got in his face; Watch what actually happened in the full CNN segment.

He throws a personal jab... then folds the second he gets pressed.

Scott loves to dish it but can’t take it.

English

@yianisz What's you take on the acquisition?

Needs to go well, no?

English

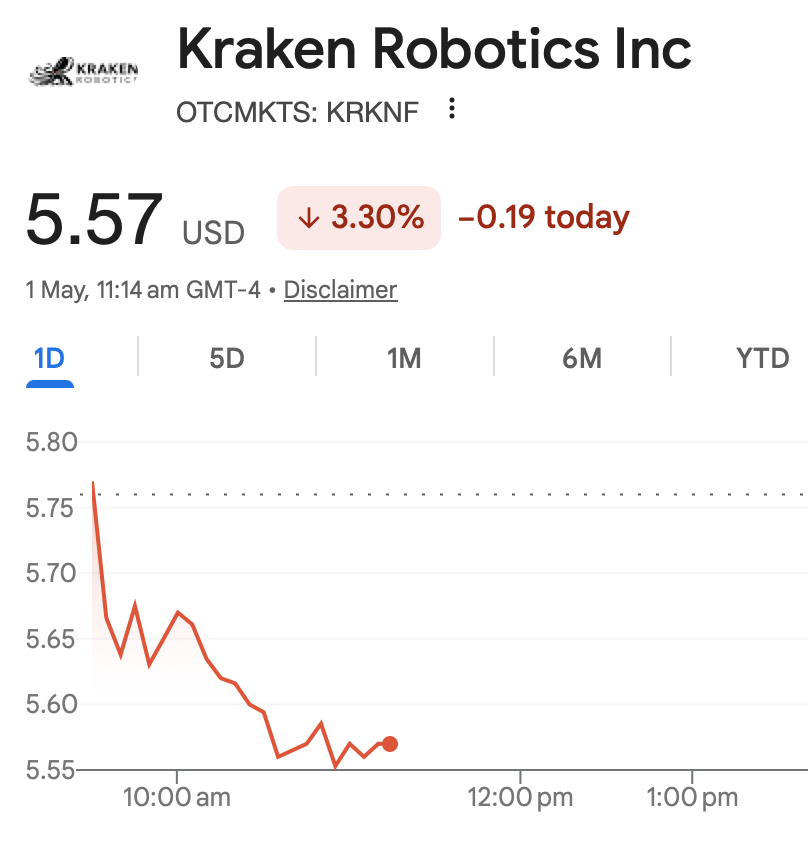

$KRKNF is one of the few positions I genuinely sleep well at night with..

Not because it’s not volatile, it clearly is. But because underneath the noise this is a company executing, scaling,and lining up real catalysts.

Orders keep coming, margins improved, Covelya is about to transform the business but let’s be honest, that’s not even the main event.

The real unlock is still ahead: TSX (and eventually NASDAQ) uplisting.

That’s when this stops trading like a niche small-cap and starts attracting serious capital.

Until then, it’s just volatility around a story that’s quietly getting stronger.

Anything below <$6 is a gift..

English

@fifa_professor I size based on volatility so naturally smaller names get smaller weight unless I see something I’m confident in.

I like some small names but I’d rather not share with the world.

English

It’s looking more likely that most of the people who escape the permanent underclass won’t be employees at big AI labs but mainly people who decided to full port semis for the next 3 years.

Moose@Brownmoose

POV: It's 2030 • $NVDA is at $650 • $SNDK is at $4800 • $AMD is at $2100 The AI hype was not a bubble and you are still sidelined.

English

@MoodyWriter13 Sorry, that's not an actual revenue related scenario

English

@MoodyWriter13 Price surges thanks to retail and then strategic acquisition with a premium by some other bubbled company?

English

I recommend that everyone, especially with stocks where there’s a lot of writing and very little math, run a few scenarios for the future. Let’s take LPKF.

Mega bull scenario for glass revenue (plateau from 2029–2030):

LIDE equipment: 8 to 12 major customers scale into mass production, each needing 5 to 15 systems. At 20 to 40 new systems annually and €1.5 to 2.5M ASP, that’s €40 to 80M. Platform upsell (NeXaR Ablate, Bond, Direct Write): 2 to 3 additional systems per customer, adding €15 to 30M. Foundry services for smaller customers (quantum computing, MEMS, prototyping): €10 to 20M, limited by site capacity. Recurring revenue from an installed base of 80 to 150 systems (service, spare parts, upgrades): industry standard is 5 to 10% of installed value annually, so €10 to 25M. CPO/waveguide equipment, if adopted from 2028 to 2029: 5 to 10 Direct Write systems at €2 to 3M ASP, so €10 to 30M.

Mega bull total: €85 to 185M annually from glass by 2030, a doubling of today’s total revenue, from the glass business alone, on top of the legacy business.

What that means for valuation: At €150M glass revenue, 20% EBIT margin and 25x EBIT multiple, both optimistic, the glass business alone would be worth ~€750M. With the market cap already at ~€470M today, I don’t see 10x potential here. Even in this wildly optimistic mega bull scenario, we’re looking at a 1.5x at most. And that assumes every single optimistic assumption plays out simultaneously.

Does anyone have an even more optimistic revenue forecast they’d like to share and walk me through? I’d be happy to take a look and potentially revise my assessment.

English

he's like the retarded forrest gump

Clavicular Updates@Clav0Updates

Clavicular begins his expedition to Epstein’s island, Little Saint James, to film a stream there 👀

English