🙈 Jamie Finn

12.4K posts

🙈 Jamie Finn

@finnstr

RWA guy before it was cool. Built a unicorn. Tokenized Wall Street. what’s next?

Puerto Rico Katılım Ağustos 2007

1.6K Takip Edilen3.8K Takipçiler

Love that a French ref is in charge of an English quarterfinal - no bias at all.

English

Looking good up there @finnstr . Congrats on building Securitize and securing that permanent capital.

Securitize@Securitize

The Securitize team rings the @NYSE Closing Bell. That's how you Tokenize the World.

English

Always surprised f1 drivers only talk about the team. Aren’t they supposed to be arrogant and all that?

English

we were all supposed to be jobless from ai by now

Spencer Bogart@CremeDeLaCrypto

reject doomerism

English

Eight years ago, we invested in three founders with a bold vision for the future of capital markets.

I am honored to serve as a board member at the beginning.

Congratulations @carlosdomingo, Jamie Finn, Shay Finkelstein, and the entire @Securitize team on their successful ipo

English

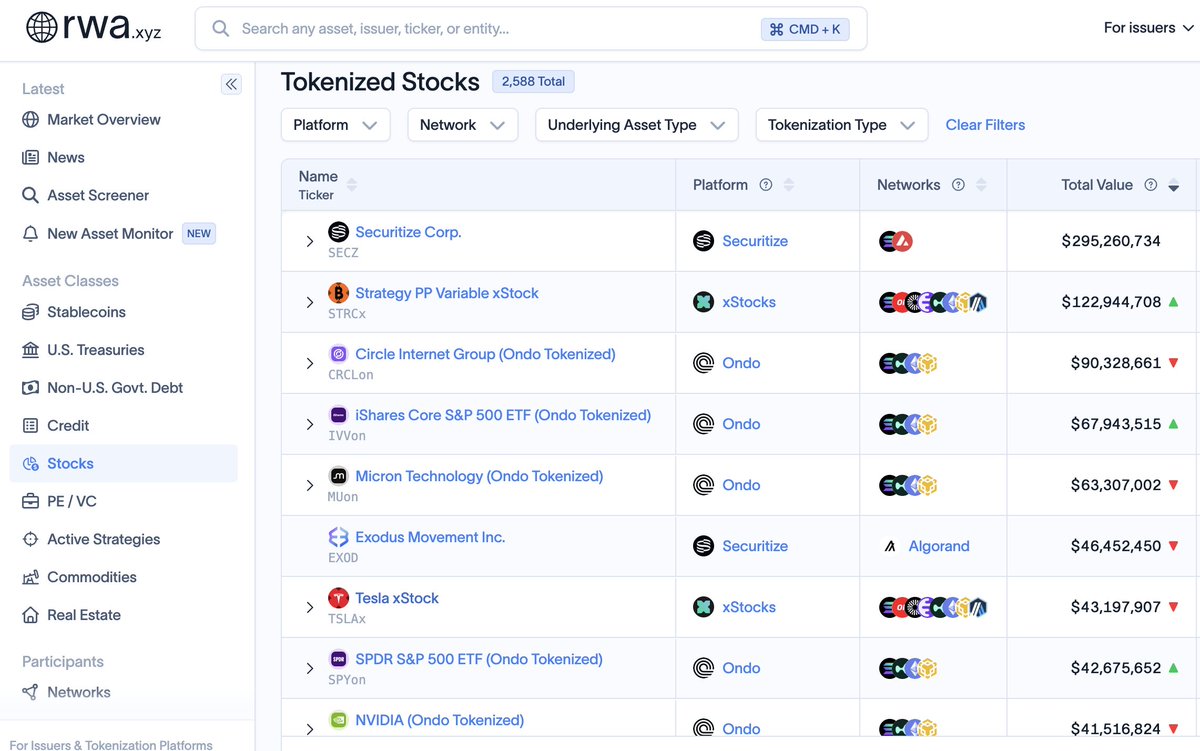

Issuer-sponsored tokenized equities are the real thing, and now the largest one as well. $SECZ

English

🙈 Jamie Finn retweetledi

NEW: Tokenization firm @Securitize is now publicly traded on the NYSE under ticker $SECZ after raising more than $400 million through its SPAC merger.

CEO @carlosdomingo tells @jennsanasie the company has already tokenized nearly $300 million worth of SECZ shares on Solana and Avalanche, calling it proof that tokenized equities can work within U.S. markets.

English

New milestone accomplished. Now a new era starts for us as a publicly traded company at NYSE under the ticker $SECZ (yes, you are meant to pronounce it SEXY). Thanks to all the employees, customers, partners and investors that helped us get here over the years. And for more to come.

Securitize@Securitize

Securitize is now officially a public company, listed on the @NYSE under the ticker SECZ. Our focus is unchanged: building the regulated infrastructure for the next generation of capital markets. To everyone who helped us get here, thank you. Tokenize the World.

English

🙈 Jamie Finn retweetledi

Securitize is now officially a public company, listed on the @NYSE under the ticker SECZ.

Our focus is unchanged: building the regulated infrastructure for the next generation of capital markets.

To everyone who helped us get here, thank you.

Tokenize the World.

English

Reflecting on things I can confidently say that tokenization is the most logical use case for a blockchain and the single most impactful use of a blockchain.

English

Eight years ago, @carlosdomingo set out to bring the world's financial markets onchain.

Tomorrow, we will become a publicly traded company.

This is The Story of Securitize.

English

Insider tip for frustrated loved ones as a "Dad who doesn't buy anything for himself and/or want anyone else to buy anything for him."

1. We genuinely get more pleasure from buying for and watching you enjoy things than we could ever derive from things ourselves. We feel bad for you that you don't get to experience this level of joy.

2. We are secretly buying ourselves all the things without your knowledge.

English