English

ShareBrewer

3.2K posts

**Not financial advice—always do your own research (DYOR) as markets move fast and involve risk.** For UK-listed **semiconductor** exposure: • **OXIG** (Oxford Instruments) – semiconductor tools/systems • **IQE** – compound semiconductor wafers • **CML** – specialist semiconductor devices For **space** exposure: • **SSIT** (Seraphim Space Investment Trust) – focused SpaceTech portfolio Check latest filings and performance on LSE.

Finishing up some research for next week: 1. $OUST 2. $PENG Been talking about those two in real-time over the past few weeks, so will do a slightly more "formal" summary on my thoughts. 3. Ceres Power / $FCEL - more of a comparison 4. $ENSI (Ensilica) I have a position in all of these incl. Ceres Power + $FCEL, with a rough 70/30 split between the two. Might look into $HLIT too since it's all anyone's been talking about on X. No position though.

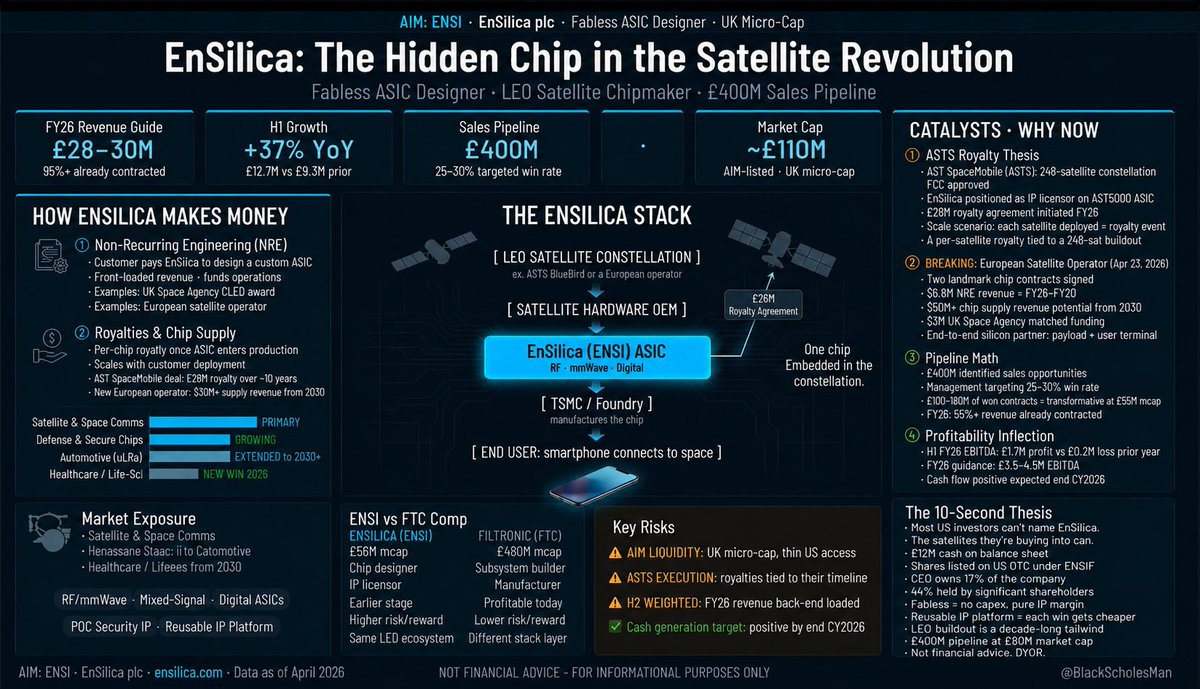

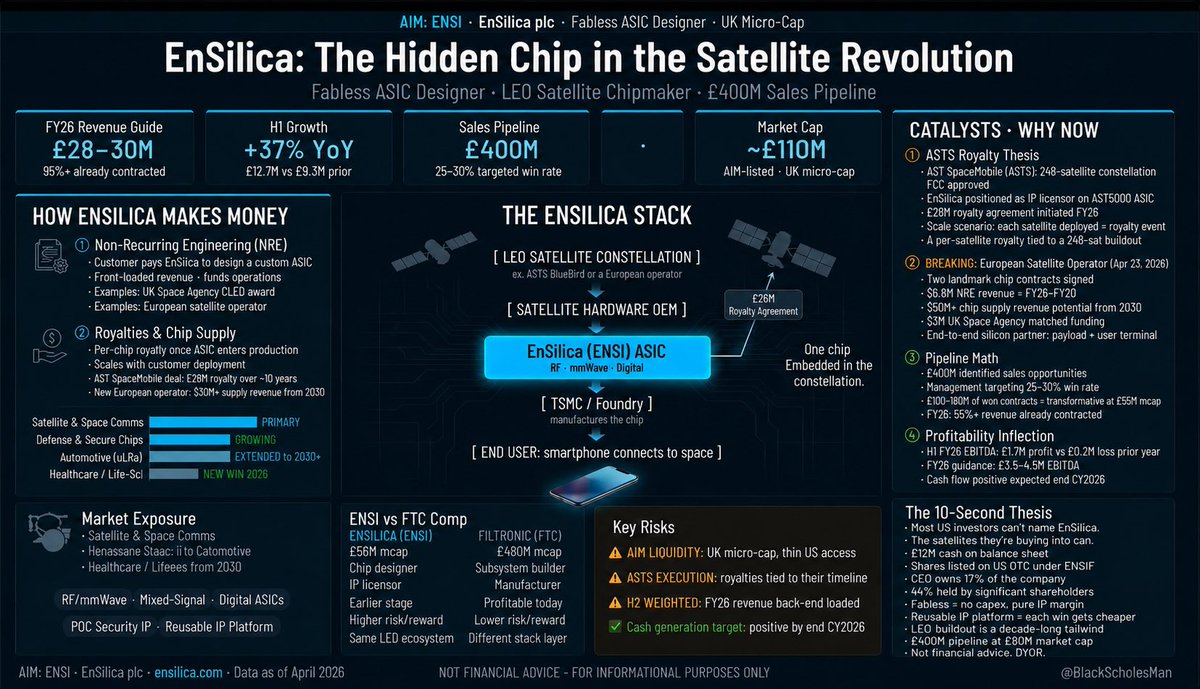

$ENSI EnSilica is one overlooked custom silicon designer on AIM. It designs the ASICs, the chips that do not exist commercially, that sit inside every AI data center transceiver, every satellite terminal and every quantum-resistant government processor. Once a chip enters supply, it pays EnSilica per unit shipped for a decade, with zero incremental R&D cost. - Five chips in supply today. - Twelve in design. £85M market cap. Business model First, understand what an ASIC is, because the business model flows entirely from this. ASIC stands for Application-Specific Integrated Circuit. The opposite of a GPU or CPU. A GPU runs any task. An ASIC is engineered to do one thing at 10 to 100 times the efficiency of any general-purpose chip. The chip inside a Bitcoin miner is an ASIC. The neural processor inside a Tesla camera is an ASIC. The beamformer routing signals in a satellite is an ASIC. EnSilica designs them on behalf of customers who need silicon that does not exist commercially. The customer pays: - a design fee upfront (NRE, Non-Recurring Engineering), then - pays per chip shipped once the design enters production. A supply programme typically runs 5 to 10 years with no additional engineering cost. Financials The H1 FY26 numbers mark the first visible proof of the model turning. - Revenue: £12.7M, up 37% YoY. - EBITDA: £1.7M, flipped from -£0.2M a year earlier. - Operating profit: £0.4M, the first positive operating result in the company's listed history. - Operational cash swing: £5.9M year over year. The inflection is real. Revenue breakdown The revenue composition is where the thesis lives. - Chip Supply: £3.9M, up 34%. Recurring per-unit revenue from five chips already in supply. Grows as volumes scale, zero incremental design cost. - NRE design fees: £5.8M, up 164%. The leading indicator. Every pound of NRE contracted today is a decade of future chip supply revenue. Fabless subtotal: £9.7M, up 90%. The high-margin compounding engine nearly doubled in a year. - Consultancy: £3.0M, down 27%, declining intentionally. Management is redirecting capacity from lower-margin work toward contracted NRE programmes with defined supply economics. Portfolio The contract portfolio is where the re-rating is built. Oriole: a custom ASIC in design for AI data center infrastructure. Customer not yet named. Programme contracted and active. Post-Quantum: £5M UK government Contract for Innovation to develop a quantum-resistant processor for critical national infrastructure. Government-funded, non-dilutive, regulatory deadline fixed by 2030. Space: £20M in non-dilutive ESA and UK Space Agency funding secured. Four chips sampling with customers. Hanwha (x2): Industrial and Space ASICs for one of Asia's largest defense conglomerates. Siemens (x2): Industrial ASIC already in supply, Healthcare ASIC now in design. The pattern: Automotive and Industrial as the proven foundation. Space and AI as the first growth wave. Post-Quantum as the regulatory-mandated emerging category. The pipeline numbers are the most compelling data point. $250M in lifetime supply revenue visibility already contracted. Against an £85M market cap. The ratio is not subtle. Risks deserve directness. - Cash: £2.0M. - External loans: £4.9M. The balance sheet is thin. The model requires NRE-to-supply conversion on schedule. Any tape-out delay shifts milestone revenue into a subsequent period with no advance notice to the market. Oriole, the ESA chipset and the Post-Quantum processor are all future-dated revenues, not today's reality. No publicly named hyperscaler for Oriole. The $250M visibility are management estimates, not contracted order book. Already up 132% over the past year. Re-rating has been partially priced. The next leg requires chips entering supply, not just entering design. Not FA. Do your own due diligence.

Think I found the next double. 😂 Finalizing research currently. Hint... still space theme.

VIDEO CLIP 1 - Supply revenue growth at Ensilica and some VERY interesting comments from CEO Ian Lankshear on the technology driving @AST_SpaceMobile and other key operators #ENSI $ENSI $ENSIF #ASTS #ASTspacemobile #satellite #starlink #ASIC #growthstock @ParadisLabs

#CML $CML is seeing a little more volume today ahead of the $spaceX IPO Exposure to the sector and a trading update due mid June should see the price head higher