gautam

82 posts

5 SME IPOs opened at present & one opening Tomorrow

1• Q-line Biotech

2• Autofurnish Ltd

3• Harikanta Overseas

4• Bio Medica Laboratories

5• Vegorama Punjabi Angithi

6• M R Maniveni Foods (Opens on 22)

I will apply only Q-line Biotech & wait for Merritronix Limited

English

@investorniti Some influencers said this was under valued and they recommended it highly...what's your take

English

Connplex Cinemas

hits lower circuit of 20% momentarily

What are investors expecting here?

English

Simca Advertising SME IPO

(Closing Today)

👉Here is a very important note :

🔸QIB quota in this IPO is ~ 30%

Normally QIB quota is ~47-48%

🔸But the interesting part is,

The reduction of QIB quota is mainly due to reduction in size of anchor portion and not much from the portion open for institutions generally, which we track.

This means,

Whatever QIB demand you are seeing on screen, on closing day, data is fairly accurate and not that much inflated. You can adjust it for 20% to get exact number.

🔸For example :

If QIB demand right now is 22x,

This will mean that actual QIB demand is close to 17.5x

(reduced by 20%, actual demand here means demand in normal QIB quota situation)

🔸Given that on paper numbers are good, if demand kicks in well, it will become very interesting.

So, keep an eye till the end on overall situation, may turn out a great prospect, who knows 🙂 will post review and rest of the updates as soon as anything comes up.

#IPOAlert

English

@investorniti You mean there is a chance if we buy in preopen if there is a sub dued listing below 32 percent.

English

Recode Studios SME

Anyone who has got allotment here, sitting fine with +32% GMP.

If market doesn’t see any hiccup, might do even better.

I didn’t get this one ❌

English

@Paryan_Sharma Wats your take on value360...issue under subscribed. Gmp just started

English

From 1% GMP yesterday to Almost 15% GMP now, OnEMI has Done Really Well Post IPO Closing

Good Market Sentiments and Solid QIB Response led to this Blast

Let's See how Listing Plays

Paryan Sharma@Paryan_Sharma

Full IPO Review OnEMI Technology Solutions (Kissht) Small Risk Takers Can Evaluate for Small Listing Gains and Medium Term Holding ✅ Pointers: ▫️Kissht is a Technology Based Lender which primarily provides Digital Loans to its Customers for consumption and business needs via its Mobile Application - The Company targets India’s emerging middle class and aspirational young individuals as customers. They have more than 6 Cr Registered Users and 1.1 Cr Customers on the App. There are close to 29 lakh Active Customers who have currently taken loans - 95% Loans are Retail Unsecured Loans and rest 5% are Secured LAPs which have recently added into portfolio - From Customer onboarding, Underwriting, Disbursements to Collections, Everything takes place digitally which is very convenient for the Users and controls operational costs for the company ▫️The Company's AUM comprises on-book loans and off-book loans. On-Book Loans are the ones which are recorded on the books of Company's Subsidiary (Si Creva) and Off-Book Loans are recorded on the books of Lending Partners and company receives fixed fees and charges from such off-book loan transactions. Current Ratio is about 50-50 for On & Off Book Loans - The Company acquires customers from Social Media/SEO Campaigns (45%), Credit QR installations at Merchant outlets (23%) and Organically (24%) etc ▫️GNPA/NNPAs are looking elevated from FY25, As per management it is happening due to Accounting changes (Shift in Writing off from 90 DPD to 150 DPD) - The Company Writes offs heavy bad loans each year and such is the business nature of this industry. The More Unsecured Small Ticket Sized Lending leads to More Defaults and eventually more Written Offs. This is the reason why Credit Cost is in the range of 8-10% for this company ▫️Objects of the Offer OFS: 76 Cr, Out of 850 Cr Fresh Issue, 1) Augmenting Capital base of the NBFC Subsidiary: 637 Cr This should help company scale the on-book Loan AUM 2) GCP ▫️Financials Kissht has been Growing Rapidly, Their AUM and Disbursements have grown multifold (60-70% CAGR) which eventually led to Income and PAT Growth As per the management, FY25 Growth was slowed down due to lesser disbursements (for maintaining the quality of the book) which led down NII/PAT Average Ticket Size and User base is Growing which indicates a Positive trajectory. ROA/ROE have also shown signs of improvements during 9m FY26 ▫️Valuation Assuming a conservative 30-35% AUM Growth for the company in FY27, The Company is coming at nearly 1.2x Price to Book Multiple Giving Kissht a 1.5x FY27 PB Multiple, Upside Visibility is 25% There is Practically no listed peer of this company, it is not right to compare it with likes of Bajaj Finance or SBI Cards. This is going to be the First Pure Play Digital Lender going public in Indian Markets A few players like Moneyview and KreditBee are also coming soon with their IPOs ▫️Other Pointers - Promoters are Good - Anchor Book was Good - Demand is Negligible ▫️Risk Factors - Contingent Liabilities However it is not a major risk since these liabilities are nothing but corporate guarantees given on behalf of NBFC Subsidiary which is a normal practice for Digital Lenders - NPAs and High Credit Costs will always be a big part of such businesses - High Competition in Lending Space ▫️Conclusion Kissht is a Fast Growing Engine with good potential This segment of digital lending is expected to grow at nearly 25-30% CAGR for next few years and this company is well placed to enjoy this growth tide It is important to keep tracking the execution and quality of assets for such companies, Some Healthy Mix of Secured Loans as well as long duration ones might make a balance in asset quality I will personally apply with limited force in this IPO for Medium term, Not Expecting much of Listing Gains Overall A Fast Growing Digital Lender with Good Growth Potential coming at Reasonable Valuations Let Markets decide the Real Value of this company You can follow me @Paryan_Sharma for such insightful IPO Reviews 👍🏻 (Note: Post is shared for Educational Purposes only, DYDD before applying, This is my personal opinion abut the company) #OnEMITechnologySolutions #KisshtIPO

English

@ipo_agarwal Sir...I respect your views ..but exceptions are there ...in Speciality medicene despite 1 percent qib, it was subscribed more than 100 times in that category which was a big positive...we can't ignore than

English

Value 360 Communications SME IPO opening today - Less than 2% QIB & 65% Retail

Don’t know how this IPO will perform but previous many IPOs with less than 2% QIB has listed at 20% Discount

If any App / website shows any kind of GMP then it’s safe to assume that it’s FAKE

English

@ipo_agarwal No...but one should not ignore every IPO just by the logic of 1 percent qib...other things like valuation...financials...peer comparison...growth prospects also matters

English

@ipo_agarwal What about Speciality Medicine...only 1 percent qib was there.

English

@iamrakeshbansal When you are giving business you are most welcome...and when you take it back things are not so smooth ...it's As simple

English

In most banks you can easily open FDR online.

But the same FDR you cannot break (pre-close) online.

You have to visit the branch.

Very inconvenient! Banks should allow both opening and breaking online.

What do you think?

English

@ipo_agarwal Is it a positive sign or a negative sign if a single buyer showing so much of interest

English

Today TIPCO Engineering India got listed just above IPO Price of 89 ₹ with 9.62 lakh shares in Pre Open

Out of that 9.28 lakh shares or 96.45% of pre open volume were bought by one Buyer

Just imagine number of lower circuits if that buyer wasn’t there? No RETAIL BUYING IN IPOs

English

@ipo_agarwal What's your call for tomorrow...will it hit another LC or there could be buying seen

English

29 Cr ki selling karke

6 months baad, 66 lakhs ki buying kare..

to wo hai asli promoter group 💪

English

@investorniti Your prediction for tomorrow sme listing...could give some gains...i know a very risky call

English

Sir,

If you look at the bigger picture,

✅ India is still a small cap compared to a giant like US.

US : ~ $69 Trillion Mcap

India : ~ $5.3 Trillion Mcap

US market is 12 times bigger than ours.

In 50 years, this difference will be reduced to 3-4x

I would humbly request you to forget India of the past, so that your thoughts shifts to compounding, to what is about to come.

Comparing return of both eras is not the correct way to look at things! Sachin & Virat can never be compared. A 12% now might be as good as 15% then, but on paper, it may look less.

Dr Sudhir Kumar MD DM@hyderabaddoctor

@InvestorOfJAMMU Some say that the next 25 years would not be as great as the previous 25 years (in terms of returns), and we need to moderate our expectations from equity, including Nifty. What is your view?

English

@AnilRelan4 Sir you need a reliable grey market dealer for that.. unfortunately not able to find one...most of them are fraud

English

This is no time to go open with any fresh paper ,it is big time to sell and apply,all powerica sold in advance all

CPMDI was also sold in premium.

Also got 1 allotment in highness micro

Already sold around 29₹ premium both LOTS.

English

@Tanmay_31_ Promoters continuouslly selling and reducing their stake is not a cause of problem ...what's your opinion

English

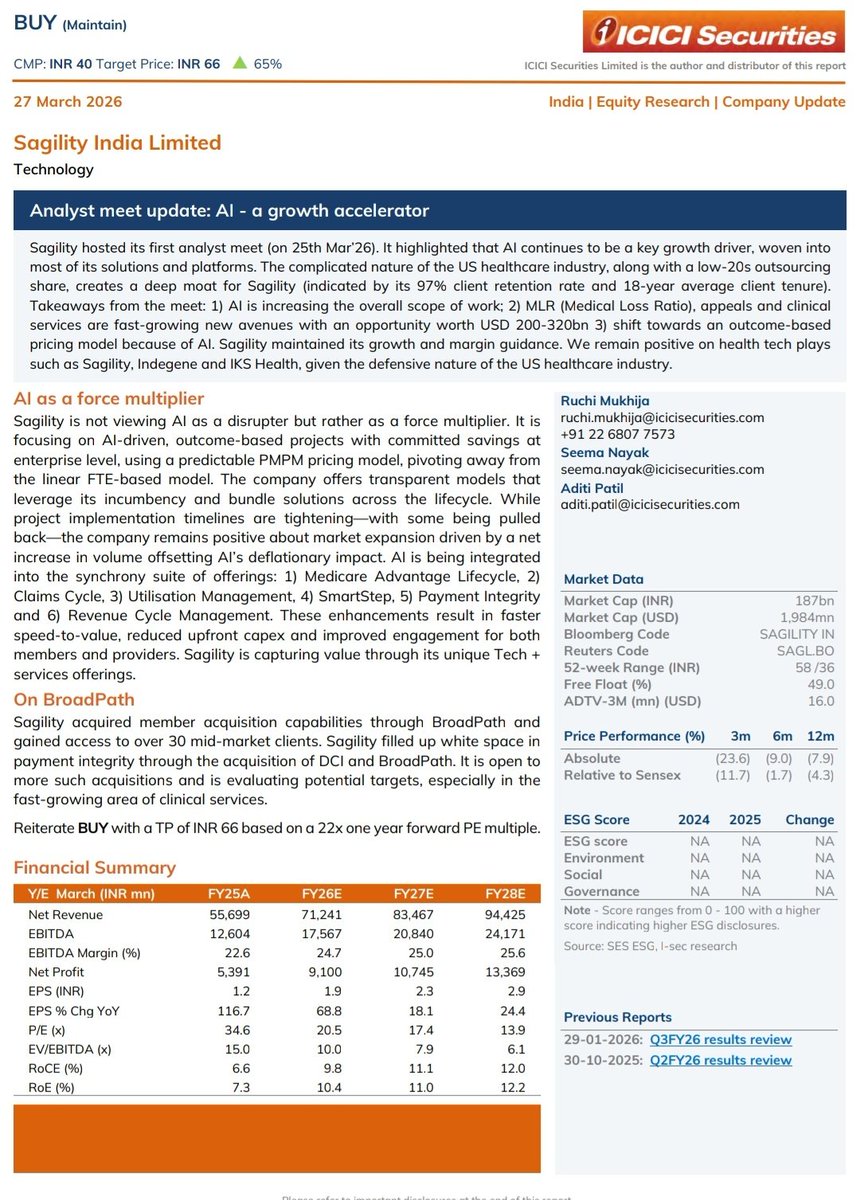

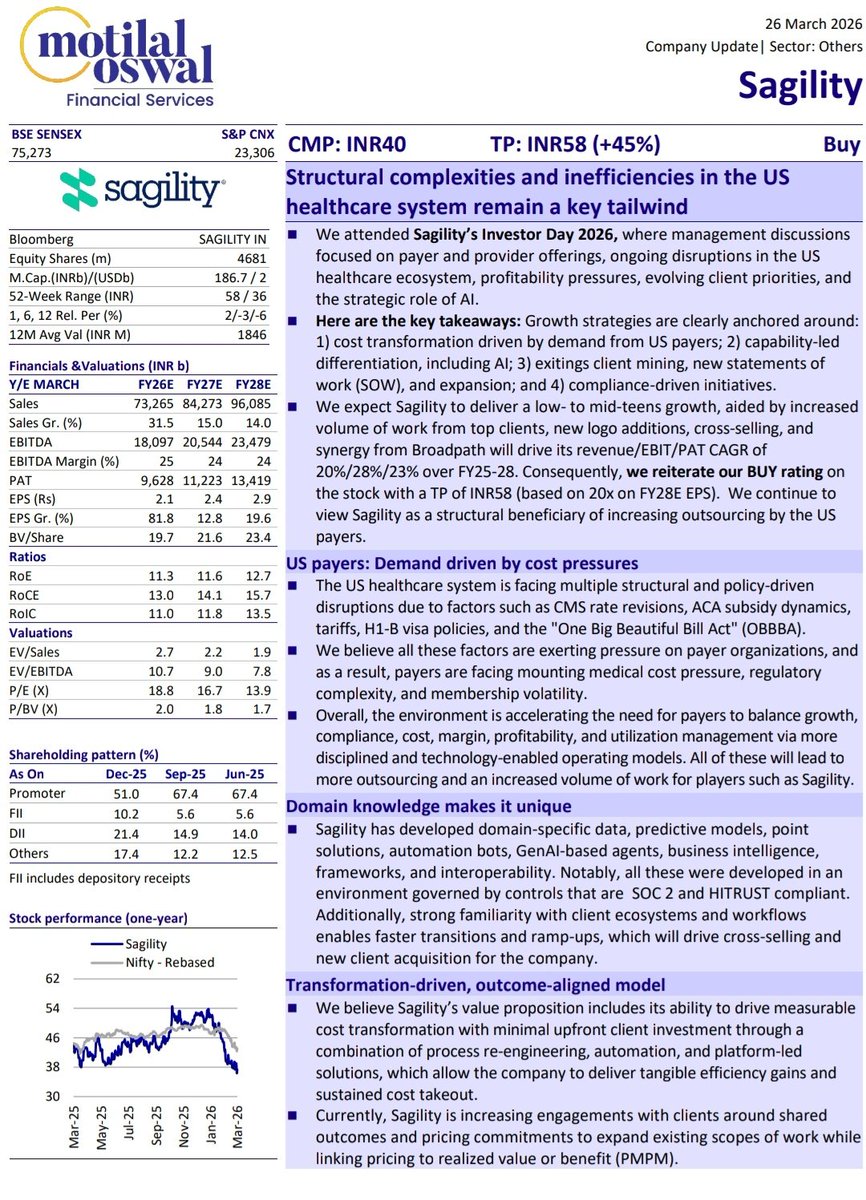

Two Brokerage Reports this week on Sagility India Limited

▪︎ ICICI Securities Maintains BUY Rating For TP : 66 (65%⬆️)

▪︎ Motilal Oswal Initiates Coverage With BUY For TP : 58 (45%⬆️)

"Structural complexities and inefficiencies in the US

healthcare system remain a key tailwind"

"AI - A Growth Accelerator,

AI - A Force Multiplier"

English

@investorniti Did you notice only 2 Qib applications bidding for 3.2 times...does these Qib are real or fake ...please advice

English

Last date, Final Update :

🌟 Tipco Engineering SME IPO

- Engaged in manufacturing and supplying industrial machinery for various industries

- Decent Financials

- Decent Valuations

- Below Average Demand

- GMP 0%

- I have applied just 1 ✅ because i saw something in the data which you normally don't see. So, trying to test the logic. Can be very expensive learning too 😅 if goes against. Risk averse should think otherwise❌. Also, numerous options on 27th March to consider for applying.

- Waited till final moments here to get an idea, that's why late input.

*** Disclaimer : This review is for educational purpose based on RHP filed by the company. All the details are public and analysis of the same is done to give readers insights of my understanding. Kindly do not consider this update as an investment advice.

#IPOAlert

English

@GuruShareMarket You unnecessary create confusion

....after 1k repayment to each...your net borrowing is 98k...97k you purchased laptop and 1k you have in your pocket...As simple

English

I borrowed 50k from Dad and 50k from Mom to buy a Laptop that costs 97k.

After the purchase, I had 3k left.

I returned 1k to Dad and 1k to Mom, and I reserved 1k for myself.

I now owe Dad 49k and Mom 49k also.

49k + 49k = 98k plus 1k I reserved for myself, which is 99k.

So where did 1k go..?

English

Today I have received LPG Cylinder !

LPG cylinder costs me ₹976 as ₹60 increased.

I have offered ₹1,000 to Delivery person but he has no change, because he has only ₹500 Notes.

I am wondering he is delivering 30-40 Cylinders a day means ₹25 per cylinder he is earning ₹1,000 a day.

Monthly~ 30,000 + Salary 🤯

English