GBDG retweetledi

The Artemis II crew named a lunar crater after Commander Reid Wiseman's late wife, Carroll. What a beautiful and touching moment.

I'm not crying, you're crying 🤧

English

GBDG

6.3K posts

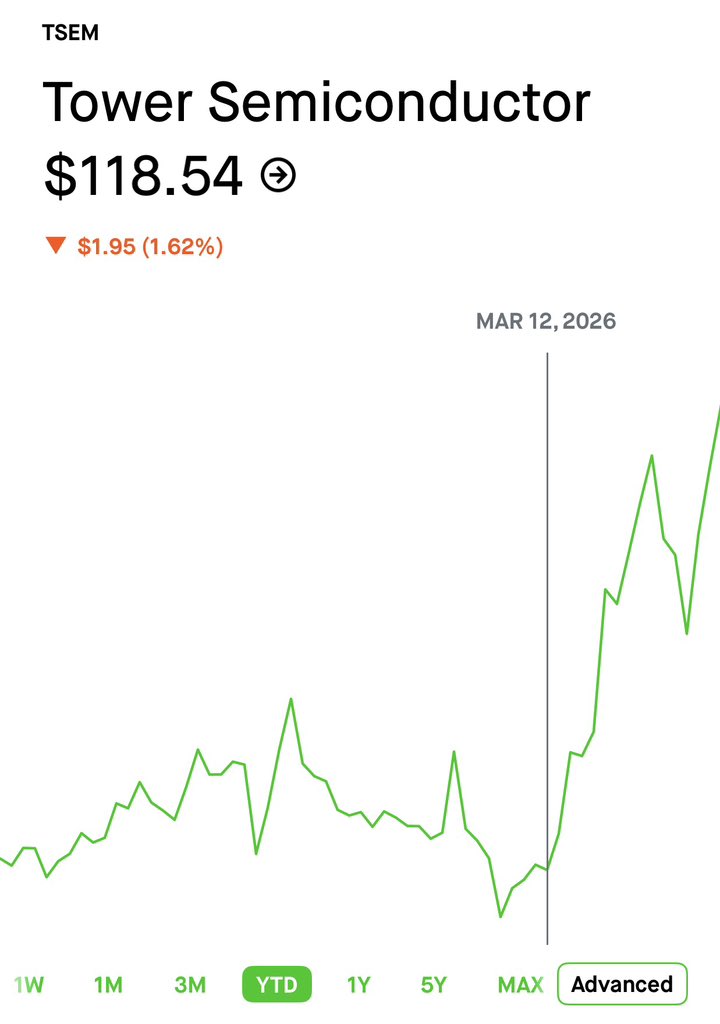

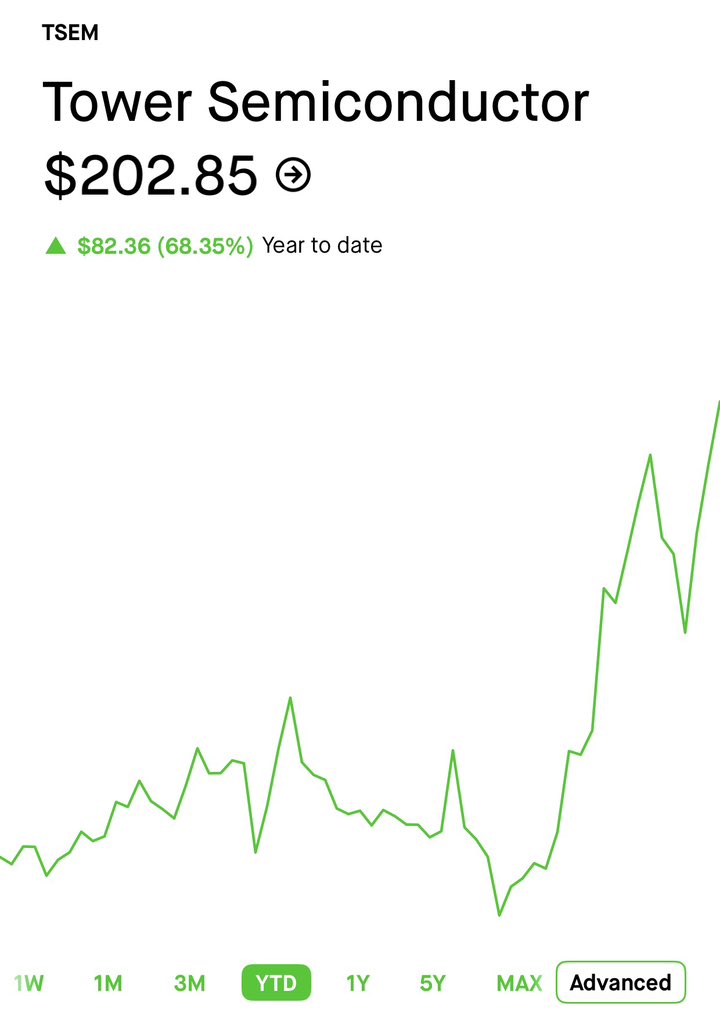

I'm long $TSEM, the $TSM of photonics. My top two picks for CPO are $SOI and Tower Semi. Given the $NVDA GTC catalyst on new photonic related architecture next week: I expect Tower Semi to get a huge catalyst. Nvidia laready directly collaborated with Tower to scale 1.6T silicon photonics last month (hint hint for GTC), likely pushing the downstream players to use it. And now, Tower is the leading supplier of 1.6T SiPh PICs and the primary foundry for scale-up CPO architectures. (the other being global foundries) From my forward est: 2028 Forward P/E: ~16.8x to ~18.1x (Tower set a target $2.84B revenue by 2028, with ~31.7% operating margin, ~$750M in net profit) The thing to note is over 70% of their planned SiPh capacity is already reserved through 2028. And photonics haven't even ramped up yet. So, I expect them to strongly beat earning projections due to extreme photonics scaling + allocations price hikes that's not modeled into projections. Also, $TSEM is heavily de-risked by 70% of capacity already being reserved. MC is likely due to $TSEM being a very obscure upstream player in the photonics supply chain. But I expect the $NVDA GTC conference to be that catalyst that brings it to premium valuations. I'm long $TSEM as an asymmetrical upside for upstream photonics foundry layer.

$SIVE has gotta be the highest upside stock I’ve seen in this market since $AXTI? No way markets missed the CW laser light source for Jabil, Marvell (Celestial via $POET), O-Net, Ayar ( $NVDA, Mediatek backed)… At a $140M valuation. ($350m now) Not only do you get the most direct laser exposure to future CPO scale up? But also this cycle’s 1.6T pluggables with $JBL (formerly Intel Silicon Photonics division) coming soon. With Win Semi bridge capacity scaling needed for hyperscaler supply chains. Don’t think 99.9% of people realized the sheer scale of this yet.

Warning: The entire AI industry will likely be bottlenecked by two companies: 1. $AXTI ($700M) 2. $SMTOY ($31.7B) Which both control 60–70%+ of the world's InP substrates. Future $NVDA, $GOOGL TPU v7 pods, $META, $MSFT, $AMZN hyperscaler clusters require InP-based lasers and receivers. $AVGO, $LITE, $COHR use for EMLs for 800G/1.6T transceivers, DFB lasers, and other optical infra. Without InP substrates, the supply chain falters. After looking at TPU BOM to Maia BOM, it looks like future ASICs + GPUs + hyperscaler deployments are heavily reliant on photonics. And two vendors could freeze the global InP substrate market covering nearly all of: - Hyperscaler optics (TPU pods, etc) - Optical transceivers (5g, data) - LiDAR (robotaxis, drones, military) -Optical Modules (interconnect clusters) - Silicon photonics laser dies (Nvidia’s future co-packaged optics and Intel/Broadcom SiPh engines use InP CW laser arrays.) Since these companies make up majority of the market supply: -AXTI (est. ~30–35%) -Sumitomo (est.~30%) - JX Nippon (est. 10-15%) That’s it. (eg. 2021 industry note from Yole states that "Sumitomo Electric + AXT together had “more than 75%” of the InP substrate market") Hyperscalers/AI are moving toward photonics but the entire AI industry is fragile. If either $AXTI or $SMTOY stop supplying materials, the entire future AI buidlout gets crippled. It's even crazier that a $700m company could become the the center of it all. InP substrate will likely one of the biggest bottlenecks alongside HMB as the AI industry shifts to photonics.