@KARLW0LF good call to take some money off the table. the earnings are usually a complete letdown when it comes to their litigation updates.. even after jury wins

English

Eugene Lee

571 posts

@greengrubbing

Dad, husband, investment coach, former Fintech/InsurTech founder, mentor, social impact investor, bboy, #HumanityFirst

$RMBS: How One Mid-Cap Powerhouse Owns the Interconnects of the Future In March 2026, investing in AI feels like the Gold Rush of 1849. Most investors are frantically buying up plots where they hope to find nuggets. But the real wealth is being built by those who control the only road leading to the mines. Rambus $RMBS is the gatekeeper of that highway. While the world obsesses over raw compute power, Rambus is solving the problem keeping engineers at Google and Meta awake at night: The Memory Wall. It doesn’t matter if your processor can handle a trillion operations per second if the data reaches it at the speed of a dial-up modem. Here is why Rambus is currently the most sophisticated "infrastructure play" in the entire semiconductor sector. 1⃣The Transformation: From "Patent Troll" to Architect Forget the Rambus of a decade ago the one that lived in courtrooms. Today’s RMBS is a fabless powerhouse that combines software-like margins (80% gross!) with a physical presence in every modern server. In 2025, their product revenue skyrocketed by over 40%, proving that the market has stopped buying their "promises" and started buying their "silicon." 2⃣The Invisible Tax: The Power of Patents and Royalties Before looking at their physical chips, we must understand the "invisible engine" financing Rambus’s innovation: IP Licensing. This is a business model every CEO dreams of. With a portfolio of over 2,500 patents, Rambus owns the foundational blueprints of modern memory architecture. This is effectively an "invisible tax" on the entire industry. Giants like Samsung, SK Hynix, and Micron pay Rambus regular Royalty Payments just for the right to manufacture their own DRAM and Flash memory. This is a stream of pure cash that flows regardless of whether the hardware market is hitting a temporary slump. In 2026, these license agreements are structured to scale with the sheer volume of gigabytes being moved and in the era of AI, we need astronomical amounts. This "cushion" allows RMBS to invest heavily in R&D without touching a cent of debt. 3⃣The Product Portfolio: Where the Heart of AI Beats Rambus isn't a "general" tech company. They dominate three precisely chosen niches that act as the primary bottlenecks of modern computing: ➡️DDR5 RCD (Registering Clock Driver): Their "cash cow." RCD chips are the brain of server memory modules. Without them, signals at DDR5 frequencies (6400 MT/s and beyond) would simply degrade. Rambus controls nearly half of this market, and every new iteration (DDR5.1, DDR6) commands a higher Average Selling Price (ASP). ➡️HBM4 Controller IP: This is where the AI magic happens. HBM (High Bandwidth Memory) is stacked directly next to accelerators. Rambus provides the complete IP stack (PHY and Controller) that manages this massive traffic. Their latest HBM4E controller, unveiled this quarter, is the industry benchmark for performance. ➡️CXL (Compute Express Link) Fabric: This is the future. CXL allows for "memory pooling," where RAM isn't locked to one server but flows wherever it’s needed. Through strategic acquisitions (like PLDA), Rambus is now the leader in designing these data "switchboards." 4⃣The Moat: Why Competition Struggles RMBS’s primary rivals in the IP segment are Synopsys (SNPS) and Cadence (CDNS) - the giants of EDA. However, Rambus has the advantage of hyper-specialization. While Synopsys designs "everything for everyone," Rambus focuses exclusively on the Processor-to-Memory interface. This narrow focus allows them to deliver lower power consumption and lower latency—the two metrics that decide multi-billion dollar server contracts. 5⃣Financials: A Cash-Generating Fortress In 2026, Rambus is a financial stronghold: ➡️Cash Flow: Over $760M in cash and zero debt. This has allowed for aggressive buybacks, reducing the share count by over 10% in the last two years. ➡️Resilience: Even if chip sales cool down (cyclicality), their Licensing IP segment provides a high-margin, consistent cash flow from the world’s largest chipmakers. 6⃣The Reality Check (Risks): Any serious investor must consider the risks. ➡️First: Valuation. With a P/E ratio hovering around 48x, there is no room for error. ➡️Second: Geopolitics. While the IP model is safer than selling physical GPUs, tighter export restrictions to China could hit their Asian partners, indirectly affecting Rambus’s royalty stream. ➡️Finally, the slight "hiccup" in OSAT (testing/packaging) supply chains seen in Q1 2026 reminds us that even fabless companies are tied to a physical world that can be unpredictable. ⬇️The Verdict Rambus isn't a "meme stock." It is a technical, highly profitable, and systemically essential company for the AI revolution. If you believe the world will need more data moved faster every single year, RMBS is a foundational block for your tech portfolio. It’s a play on the logistics of bits. And in the world of AI, logistics is everything. Let's discuss 👇 What do you think about $RMBS?

Short $IONQ. $IONQ Enters its distribution phase. Lost its 200DMA and didn’t pick up momentum at all under the 1W HMA. See volume. Volume spiked up during the prior weeks sell off. And now more volume coming in. Last good support $36. But if this is lost, I think we’re seeing $30 this week from this $39 levels. And from there lower. NFA

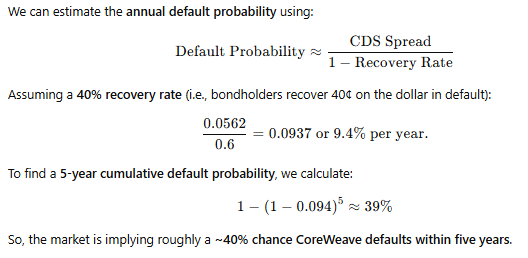

CDS for the AI companies today... nothing to see here.

"I have no idea how he pulled it off. I really believe he is the No. 1 pitcher in the whole world." - Shohei Ohtani on @Dodgers WS MVP Yoshinobu Yamamoto

Yoshinobu Yamamoto on the road in Toronto with the Dodgers down 1-0 in the World Series: 9 IP 4 H 1 ER 0 BB 8 K 105 pitches 17 whiffs What an unbelievable performance when the Dodgers needed it most.

I've finally digested the data that Uniqure presented on AMT-130, their gene therapy for Huntington's disease, which just announced a positive trial readout with 75% slowing of disease progression. Here is a blog post with my take on the announcement: cureffi.org/2025/10/08/amt…