@I_D_A_U_ @JavierBlas Any sense on the tone from the physical traders? See dated has come off, clearly paper got shellacked today. Wondering if CFDs start pricing tighter mkt if the actual flow thru SoH is basically unch

English

Hamilton Brewer

91 posts

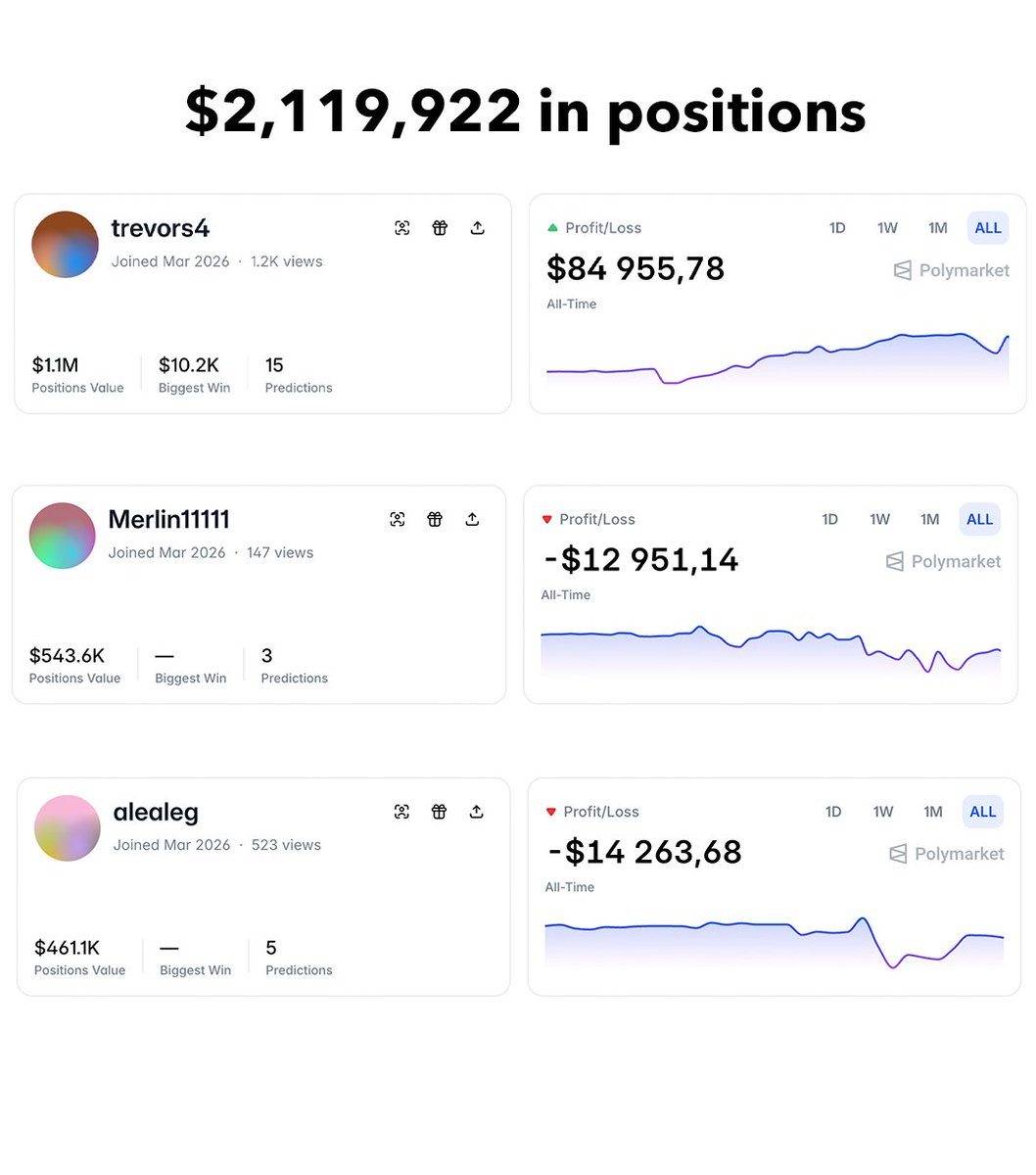

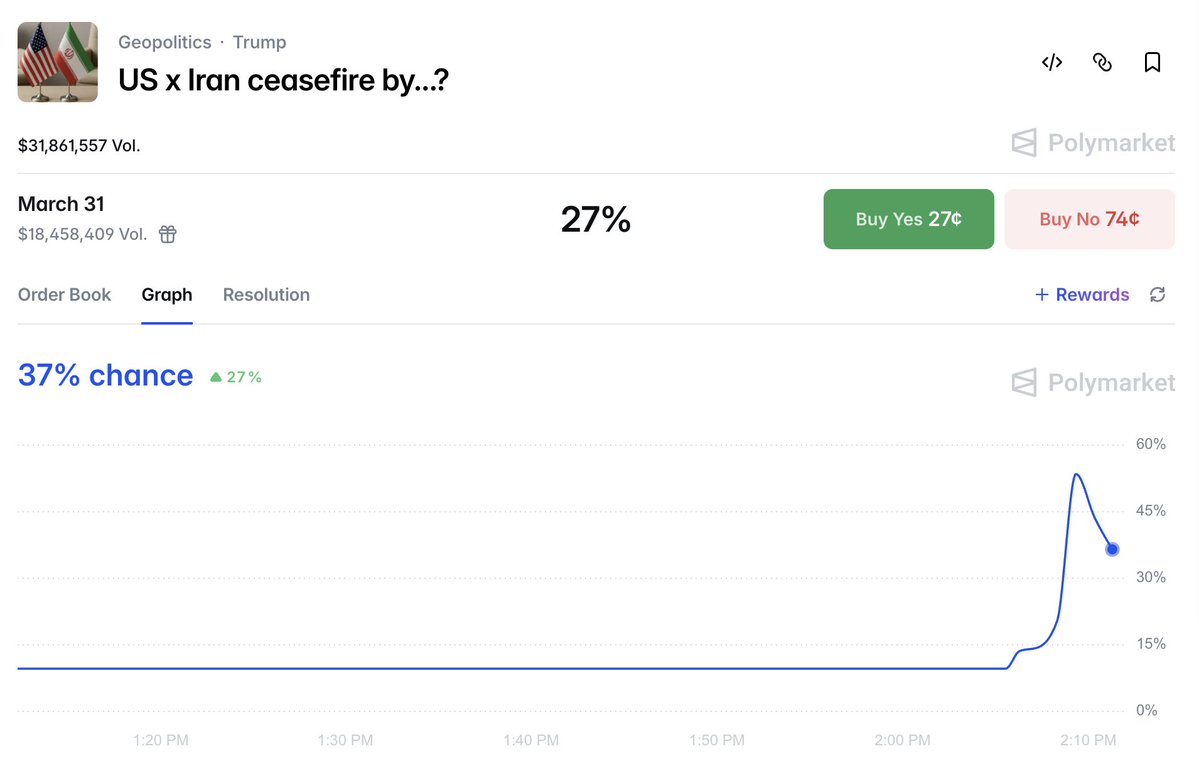

Just tracked a highly suspicious group of 10 Polymarket wallets They're trying to stay under the radar by splitting into small positions, but I caught their pattern - All in on YES for US x Iran ceasefire by Mar 31/Apr 15 - $7K to $24K in positions per wallet - 99% of positions were bought with market orders - Combined size: $160K - Payout if a ceasefire hits by EOM: +$1.04M 2 of these exact wallets previously bet YES on the US striking Iran before Feb 28 and cashed out $135k This accumulation is still happening as of today Someone is building a massive position under the radar Hard to believe these are just random users