HareCrypta

7.3K posts

HareCrypta

@harecrypta

Open cryptocurrency community by founder @Rencrypta @Harma__ NFT https://t.co/cOfHTDJsgF https://t.co/aiM0uyq7oZ

Katılım Haziran 2022

254 Takip Edilen7.1K Takipçiler

Variational story: Privacy.

A nuance that I missed and didn't think about, and most people didn't either. Many think private perps about Paradex, Hibachi, Aster.

But Variational has a different kind of privacy.

▪️Not ZK-chain privacy.

▪️Not hidden orders.

▪️Not dark pool privacy.

It is privacy by market structure.

There is no public CLOB broadcasting your intent, size, position, entry, liquidation level, or PnL to every watcher on-chain.

▪️RFQ against OLP. You get a quote.

▪️You execute privately. OLP hedges externally.

The market does not see your flow. That matters.

In transparent perp DEX your alpha becomes someone else’s signal.

Whales get copied, faded, hunted, and liquidated. Public orderbooks are great for price discovery, but terrible if you are the signal.

Variational privacy is not full cryptographic invisibility.

The public does not see you, but OLP still sees the flow.

So this is not trustless privacy, it's more like broker-style privacy:

▪️private from the market

▪️visible to the execution layer

What about RWA Privacy?

For crypto majors, transparency helps liquidity.

For RWA long-tail and large trades, transparency can destroy execution.

Variational is betting that for RWA, hiding flow from the public market is more important than showing every position to prove decentralization.

That is a very TradFi answer and probably the right one for the first serious wave of on-chain RWA trading.

Nacho@ElNachoCrypto

10 reasons why i'm giga bullish on @variational_io: 1. top 5 by oi, despite no api/mobile app 2. team respect and study hyperliquid 3. highly focussed on rewarding users 4. all trades are private 5. rfq allows for insane capital efficiency 6. excellent liquidity, low execution costs 7. ability to list virtually any market 8. antithetical to the cex model 9. founders are quants, with proven track record 10. variational pro (details below) hard to list only 10, but you get the idea gvar

English

HareCrypta retweetledi

if you are still not trading on Variational, then let's go

Code = OMNIREN

omni.variational.io/?ref=OMNIREN

English

an ordinary working morning🐱

Me, my cat named DDOS, and Codex.

Hermes Agent is running somewhere in the background.

English

HareCrypta retweetledi

The main consensus of the Moscow Trading Forum. 👇

We are waiting for hyperinflation, strengthening of the $RUB to 70-50-30 per USD, all production manufacturers are in a stupor, only Sberbank is in chocolate, has collected liquidity and lives on interest!

Only physicists buy shares on the MOEX, companies sell everything, you need to buy industrial metals, hello $COPPER!

Shares of the US and others are on ATH, and the MOEX is in the range, what will happen to the index when the SP500 collapses?

Rencrypta.eth@Rencrypta

GM X! Flowers can be eaten, snowdrops, mother-and-stepmothers, grow at the right time of the year! Good for health!

English

HareCrypta retweetledi

The CLARITY Act Moment for Prediction Markets

I found the most under-discussed Polymarket market right now.

Law banning sports prediction markets enacted in 2026?

Only 17% Yes, there are tiny volume, but huge implications.

This is not really about sports betting.

It is the CLARITY Act moment for prediction markets.

1. The core question is

Are event contracts financial markets?

Are they just gambling with a better UI?

That distinction may decide whether Polymarket (or Kalshi) become the NYSE of real-world events…

or get pushed back into state-by-state gambling regulation.

2. The timing is wild.

The U.S. Senate just banned senators and staff from trading prediction markets.

States are fighting Kalshi over sports contracts.

CFTC is trying to defend federal jurisdiction.

Lawmakers are suddenly realizing something uncomfortable.

Prediction markets can price wars, elections, nominations, legislation and government actions in real time.

That scares them, because prediction markets do not just predict politics.

They financialize political information.

That is the part almost nobody wants to say out loud.

3. Sports is the test case.

If sports event contracts are treated as federally regulated derivatives:

✅ the whole event-market stack gets stronger

✅ CFTC jurisdiction gets validated

✅ Polymarket (Kalshi) move closer to becoming real financial infrastructure

✅ election, geopolitics and legislation markets become harder to attack

But if sports gets classified as gambling:

❌ the regulatory attack surface expands fast

❌ states get a stronger template to fight event markets

❌ prediction markets get pulled back into gambling law

❌ election and geopolitics markets may be next

4. This forecast is not just about sports.

- Election markets next.

- Geopolitics markets next.

- Government-action markets next.

That is why I don’t think this is really a sports market.

It is a market on whether prediction markets become finance…

or get reabsorbed into gambling law.

5. Polymarket says right now only 17% chance of a 2026 sports prediction market ban.

Is that too low or is Washington too addicted to the data these markets produce to actually kill them?

English

English

HareCrypta retweetledi

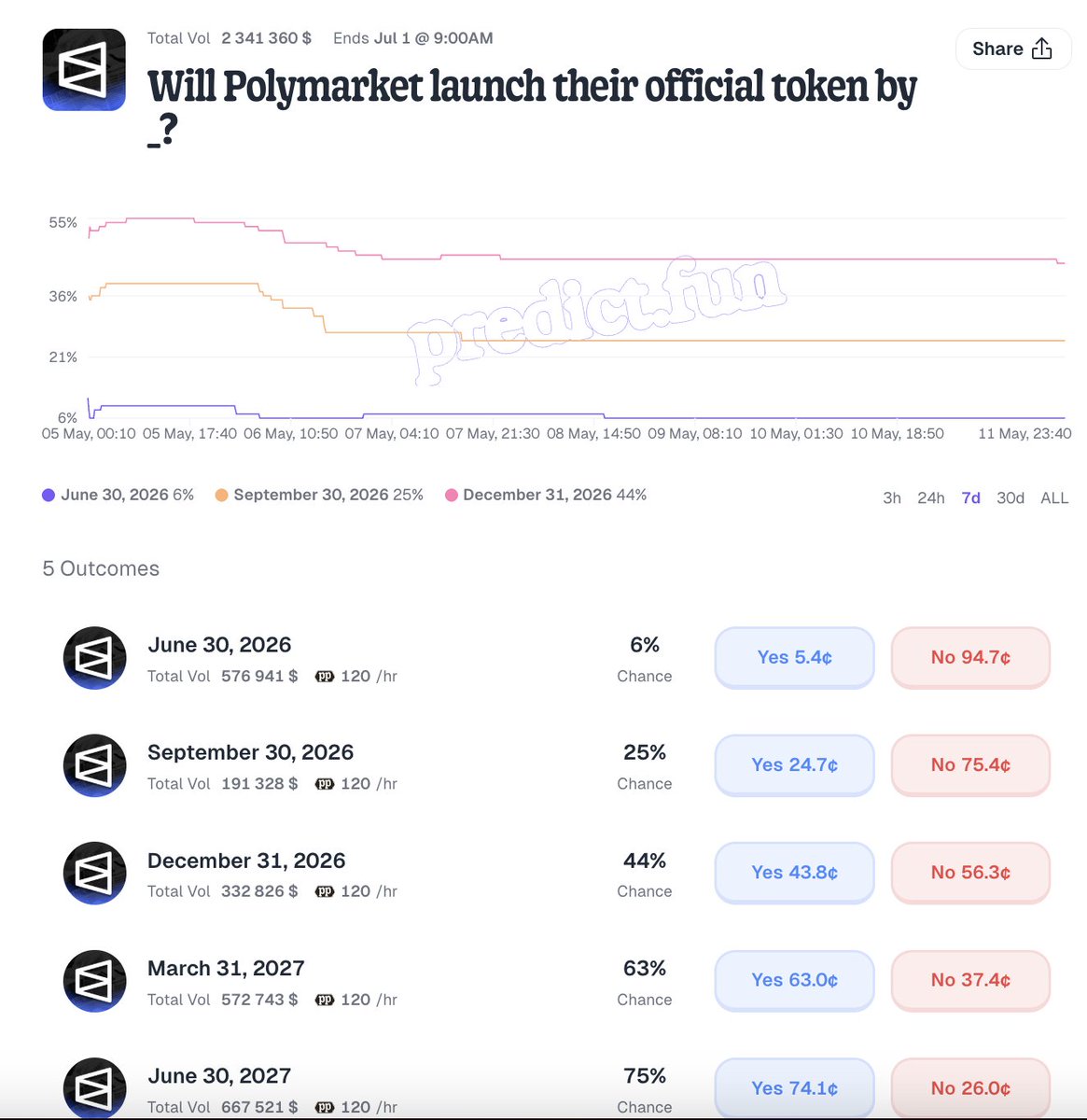

Polymarket IPO is getting louder.

TradingView now shows a planned IPO date around Dec 31, 2026.

But here’s the interesting part

The PredictFun market for $POLY token did not collapse.

It still prices roughly

• 44% by Dec 31, 2026

• 63% by Mar 31, 2027

• 75% by Jun 30, 2027

So the market is not saying IPO killed the token.

It is saying something much more interesting

IPO and TGE might not be mutually exclusive.

That is the real story.

Most people are thinking about this too simply:

IPO = Wall Street

Token = crypto

Therefore one must kill the other.

I don’t think that’s the right framework.

Polymarket may become the first major test of a dual-capital-stack internet marketplace:

✅ Equity captures the company.

✅ Token captures the chain.

That is the elegant version.

- Equity investors buy revenue, data, compliance, institutional distribution, exchange economics.

- Token holders get liquidity incentives, trader reputation, market-creator rewards, fee rebates, community participation, maybe governance around non-core network layers.

The ugly version is harder:

If the token is too valuable, public shareholders ask why value is leaking out of the equity.

If the token is too weak, crypto users realize they farmed volume for glorified airline miles.

Polymarket cannot launch a random old-style governance token anymore.

• Not with ICE/NYSE capital around it.

• Not with U.S. regulatory re-entry.

• Not if it wants to look IPO-ready.

So i think that a cleaner, more institutional, utility/rewards-based $POLY token is still very much alive.

The real question is:

Can Polymarket design a token that regulators, public investors, ICE, crypto users, and airdrop farmers can all tolerate?

If yes, this becomes a new model

public company equity + crypto-native network token.

If no, IPO wins and the airdrop crowd gets diluted by TradFi. 😠

I think the most likely path is

✅ U.S. compliance first

✅ IPO narrative second

✅ $POLY later, probably cleaner and less degen than people expect

Would a Polymarket IPO make you more bullish or less bullish on a $POLY token?

Branxi@OG_Branxi

Polymarket "IPO date" - Dec 31, 2026? @tradingview does this with almost every major private company (@stripe has the same Dec 31, 2026 placeholder) No official IPO from @Polymarket For airdrop hunters: • IPO and $POLY token are different stories • Token + airdrop were confirmed (CMO said), but tied to full US relaunch, not IPO • Real signal = when they return to the US properly Best move right now: just use the platform Don’t expect the token anytime soon just because of a TradingView date

English

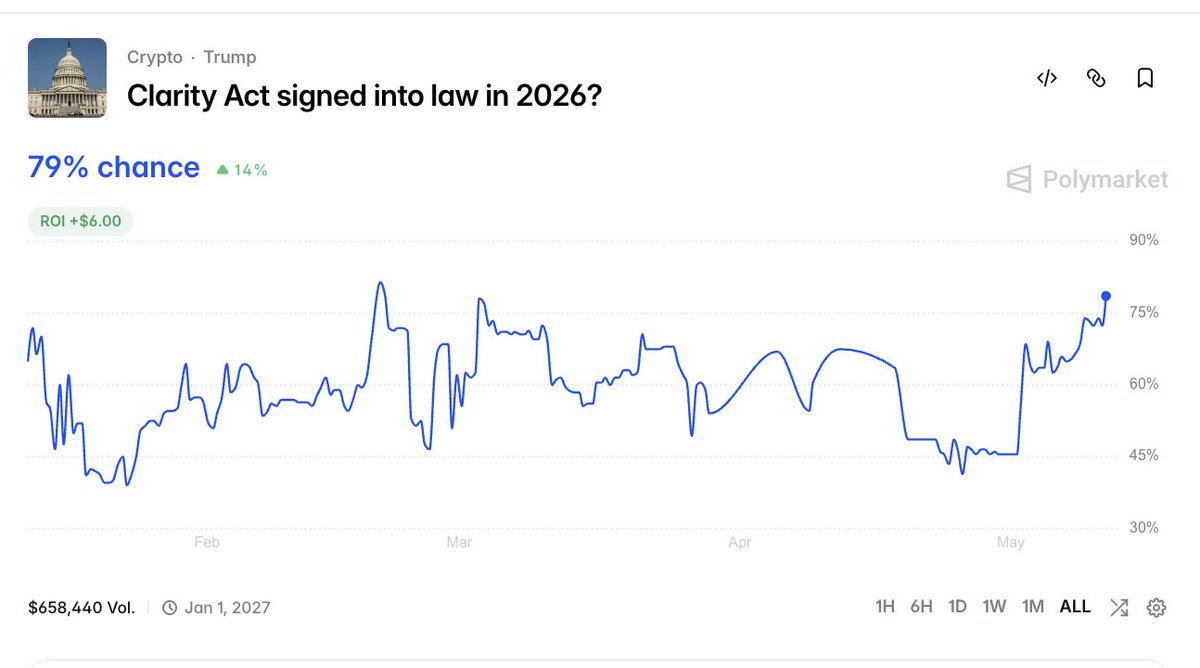

CLARITY Act just exploded to 79% on Polymarket.

Two things changed

1. Senate Banking officially put H.R.3633 on the calendar for May 14.

2. The stablecoin rewards compromise is finally public.

The rewards language is the key.

Crypto platforms cannot pay passive, bank-like yield just because you hold a payment stablecoin.

But activity-based rewards survive!

payments, transfers, wallet usage, platform usage, settlement, liquidity, staking, governance, network participation.

✅ Banks won the passive-yield fight.

✅ Crypto won the usage-rewards fight.

That is the nuance almost everyone will miss.

This bill is quietly drawing a new line in American finance

✅ Money sitting still = banking.

✅ Money moving through networks = crypto infrastructure.

It is Washington deciding which parts of digital-dollar economics belong to banks, and which parts belong to networks.

But 79% is not done.

May 14 is a committee markup, not final passage.

Clarity act still needs to get out of Senate Banking, merge with the Ag Committee piece, survive amendments,

find 60 votes in the full Senate, reconcile with the House, and reach Trump’s desk before year-end.

Next steps

• Clean May 14 markup → YES can go 85-90%

• Delay or toxic amendments → back to the 55-60%

• Bipartisan committee passage → 2026 signing becomes a real base case

• Banking lobby wins last-minute changes → market is too hot

Would you buy Yes at 79%?

Rencrypta.eth@Rencrypta

My scenarios for Kevin Warsh’s Fed nomination and the impact on the Clarity Act It is the market realizing that the April fast-track story just broke. The Clarity Act can still be politically alive, still have White House support, still have crypto industry momentum and still miss 2026 because the Senate calendar eats it alive. That’s the part traders were underpricing. The real enemy of CLARITY right now ▪️is not Elizabeth Warren. ▪️is not the SEC. ▪️is not even the stablecoin-yield fight by itself. The real enemy is time. Senate Banking still has no posted CLARITY markup date. This week the committee is focused on Kevin Warsh’s Fed nomination hearing. Tillis still seems to want more time on the stablecoin-yield language. Banks don’t need to kill the bill outright, they just need to delay it long enough. That’s the underrated game theory here: Crypto needs a law. Banks can live with the status quo. So delay is not neutral. Delay is leverage. Warsh’s confirmation does not directly decide CLARITY. He is not the crypto bill’s judge. But his hearing is taking up the same scarce Senate Banking bandwidth that CLARITY needs. 1. If Warsh clears fast, that’s mildly bullish: Banking gets its calendar back. 2. If Warsh turns into a drawn-out political fight, it is bearish: the committee loses time, the ethics/conflict-of-interest narrative gets louder, and CLARITY gets pushed deeper into May. May is dangerous. Because this market is not asking: Will the US eventually pass crypto market structure? It is asking: Will H.R. 3633 pass both chambers and get signed in 2026? That is a much narrower bet. A bill can be close and still fail that exact resolution. So here is my framework: ▪️ Markup notice this week → Polymarket probably rips back toward 60% + ▪️ No notice → 49% is not cheap ▪️ Markup slips past mid-May → 2026 odds should fall hard ▪️ Actual committee passage → Yes becomes real again ▪️ More bank/yield drama → No has asymmetric upside CLARITY is alive. But it is no longer priced like a straight line. The next catalyst is not another optimistic quote. It’s a date on the Senate Banking calendar. Would you buy YES at 49%, or is this finally where NO becomes the cleaner trade?

English

HareCrypta retweetledi

GM X!

Flowers can be eaten, snowdrops, mother-and-stepmothers, grow at the right time of the year!

Good for health!

Rencrypta.eth@Rencrypta

Variational will do an airdrop in q3 1 point will be worth $1000 source: just trust us You still have 4 months to farm $VAR In the meantime, the moments of my life today

English

Variational will do an airdrop in q3

1 point will be worth $1000

source: just trust us

You still have 4 months to farm $VAR

In the meantime, the moments of my life today

Victor.hl@VictorTopDefiG

variational will do an airdrop in q3 and 1 point will be worth $270 source: trust me bro you still have 2-3 months to farm, start doing volume every day it just takes a few minutes omni.variational.io/?ref=OMNIVICTO… Code - OMNIVICTORR

English

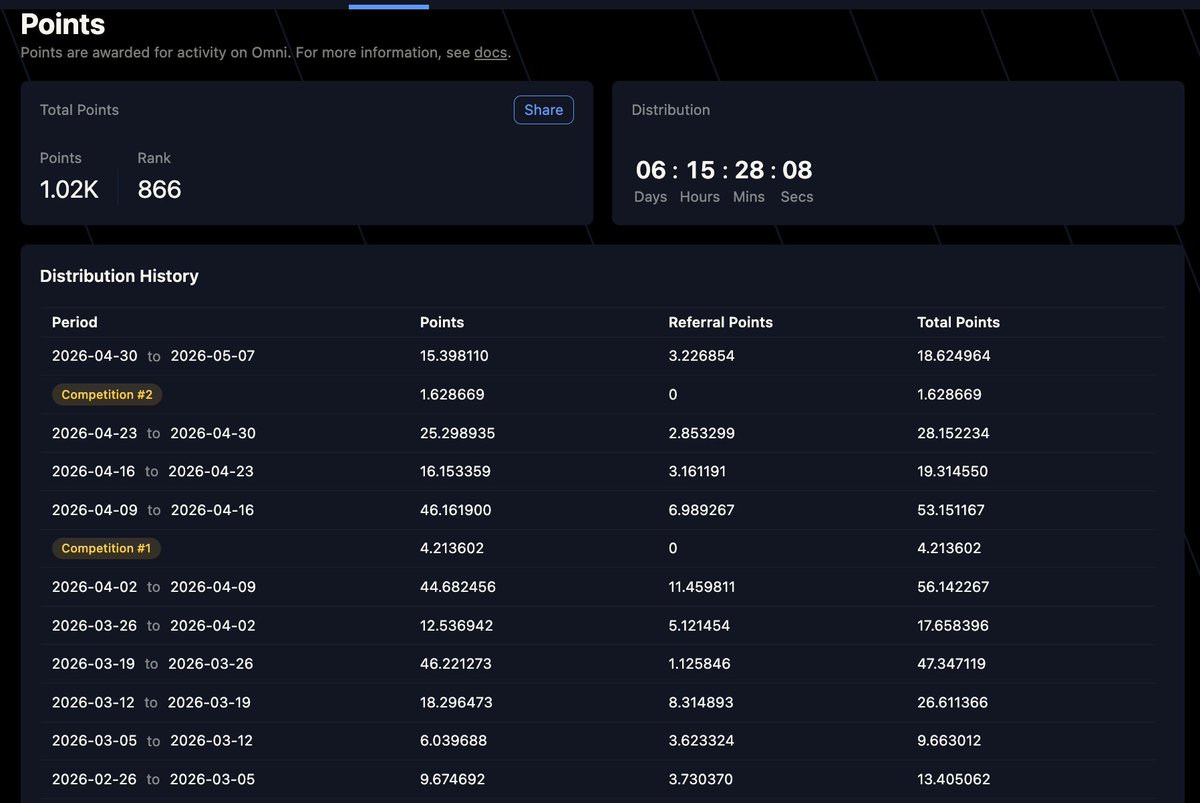

+18 Variational points by manual this week

+1.61 Points using trading bot (866 rank)

Not a lot, but honest work.

I finally learned how to develop and use a trading bot using Cloud that trades slightly profitably while also farming points.

I can gradually increase deposit.

This bot is based on looking for increases in negative funding and coin growth, and it enters these coins for a certain period of time,

earning slightly more on the funding tick or take-profit than when the stop-loss is triggered.

Rencrypta.eth@Rencrypta

100+ Liquid RWA markets is not the alpha. The alpha is whether Variational can turn off-chain dealer balance sheets into an on-chain execution API. CLOBs try to recreate liquidity. RFQ routes to where liquidity already lives. If they nail fills, spreads, and uptime, this becomes a real RWA market-structure shift 👇

English

HareCrypta retweetledi

Who are still not trading on Variation yet? OMNIREN

omni.variational.io/?ref=OMNIREN

English

Rain and sun 🌧️🌤️

It's a wonderful day!

Like vibecoding and content factory - a hybrid state of life!

Rencrypta.eth@Rencrypta

GM X! Sport TV shows you a forest show! Meanwhile, dinosaurs wake up in the crypto $ICP $KSM $TAO take off!

English

HareCrypta retweetledi

TGE $POLY launch at 46% possibility this year.

An interesting bet has emerged, and the Volume is quite good $2mln

That means people are already significantly risking their money.

A good indicator to track.

Said@said116dao

A couple of days ago, the Polymarket senior intern said the airdrop was coming "very soon" But in reality, the chances of the token being launched haven't changed since he made those remarks TGE odds this year are only 45% 45% doesn't look like “very soon” [Bet] - predict.fun/market/will-po…

English

GM X!

Sport TV shows you a forest show!

Meanwhile, dinosaurs wake up in the crypto $ICP $KSM $TAO take off!

Rencrypta.eth@Rencrypta

GM X! The forest heals and cripples while opening up the sore! $BTC is slowly moving towards $84k.

English

GM X!

The forest heals and cripples while opening up the sore!

$BTC is slowly moving towards $84k.

Rencrypta.eth@Rencrypta

Gm X! I breathe with my free chest, I breathe with the wind, I breathe with passion and love for the roads!

English

HareCrypta retweetledi

RFQ (Variational) vs CLOB in RWAs is not a frontend debate.

It is a balance sheet debate.

CLOBs are great when liquidity already wants to be public.

$BTC $ETH $SOL are top perps, these markets have natural two-sided flow, active MMs, arbitrageurs, scalpers, basis traders, and enough attention to keep the book alive. In that world, a public order book is powerful:

visible bids/asks, transparent depth, real price discovery, limit orders, maker strategies, and a market everyone can inspect.

But RWAs are different.

The problem with perps on everything is not the matching engine.

The problem is that every new market needs risk capacity.

Oil needs liquidity. $XAU needs liquidity. $AAPL needs liquidity. USD/JPY needs liquidity. Japanese equities need liquidity. Korean stocks need liquidity. Every ticker becomes its own cold-start problem.

A CLOB does not create liquidity. It displays liquidity.

That is the uncomfortable part.

For long-tail RWA, the real liquidity already lives somewhere else:

dealers, OTC desks, brokers, CEXs, TradFi venues, non-bank market makers, and internalized flow networks.

Rebuilding that depth on-chain ticker by ticker may be elegant, but it is brutally inefficient.

That is the bull case for RFQ.

Don’t force every market to bootstrap a public book from zero.

Ask multiple dealers for a quote, route to the best one, settle with stablecoins, keep margin on-chain, and let LPs hedge wherever the deepest liquidity already exists.

For large trades and thin markets, this can be better. Less signaling. Less information leakage. Better size-aware execution. Faster market launches.

More realistic access to RWA liquidity.

But RFQ has its own dark side.

A bad RFQ system is just opacity with a nice UI.

Zero fees can simply mean the fee is hidden in the spread.

Users may not know whether they got best execution. Dealers can widen quotes or stop quoting during stress. If only one or two LPs dominate, the venue becomes dependent on their balance sheet and risk engine.

So the real answer is not CLOB vs RFQ.

CLOB wins where markets are liquid, public, and naturally active.

RFQ wins where markets are fragmented, thin, block-sized, or hard to bootstrap.

Crypto majors look like CLOB markets.

RWA long-tail looks like RFQ markets.

The endgame is probably hybrid model:

public books for price discovery,

RFQ for size, dealer networks for external liquidity, on-chain margin, stablecoin settlement, and routing engines optimizing for best execution.

The winning venue will not be the one with the purest architecture.

It will be the one that gives traders the best fill.

Variational@variational_io

English