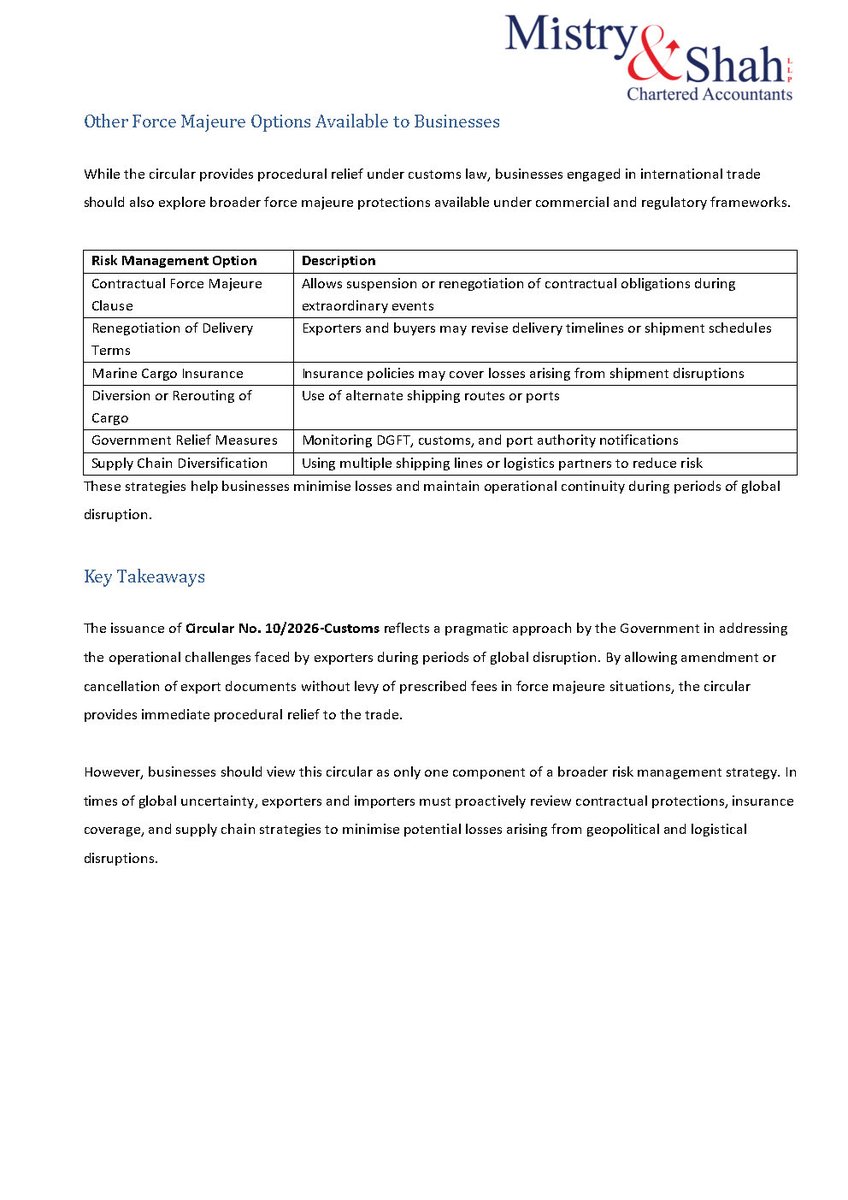

Sabitlenmiş Tweet

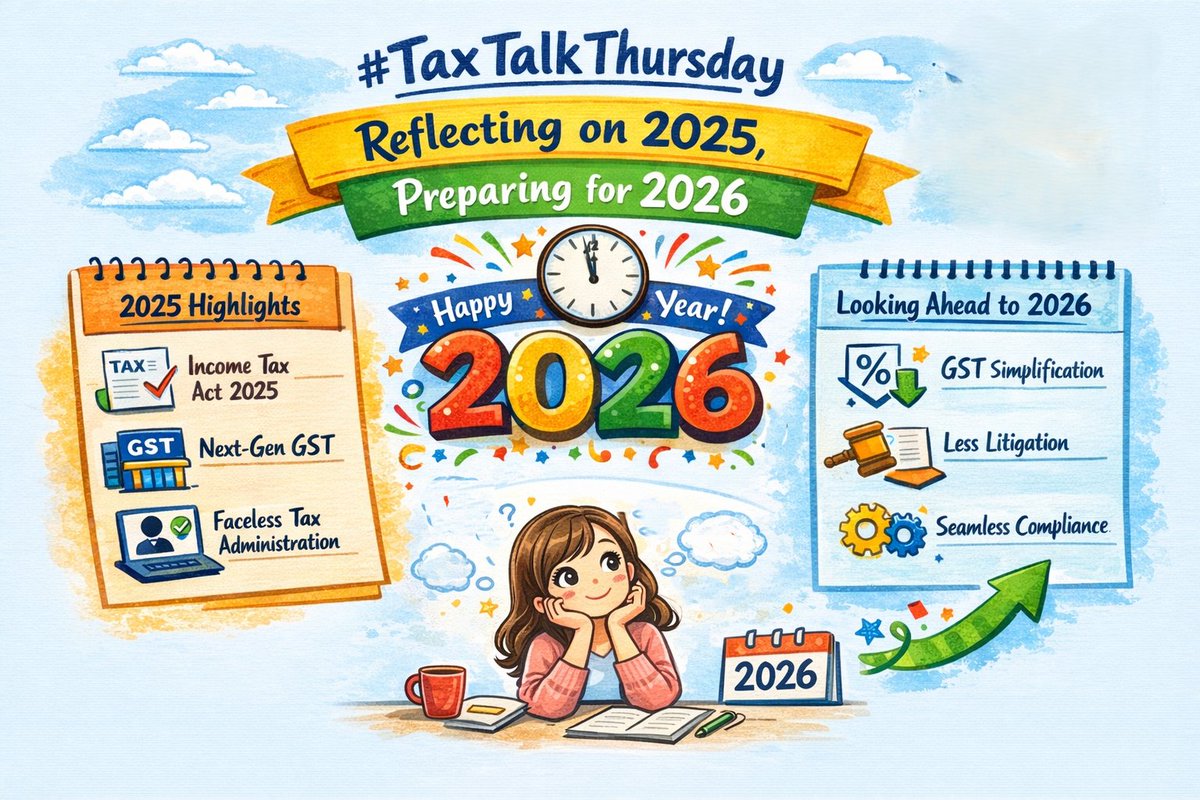

#TaxTalkThursday | Reflecting on 2025, Preparing for 2026

As we step into the new year, I would like to thank all the readers of Tax Talk Thursday for their valuable views, comments, and engagement throughout the year. Tax Talk Thursday was one of the initiatives I started in 2025, and the consistent interaction from readers has been both encouraging and motivating.

As we look back at 2025, it is worthwhile to pause and note some of the important tax reforms introduced during the year. These reforms reflect a clear policy direction towards simplification of laws, reduction of ambiguity, improved compliance experience, and increased reliance on technology driven administration.

On the indirect tax front, continued progress towards Next Generation GST remained one of the key positives of the year. Rationalisation of rate structures, improved refund mechanisms, and strengthening of digital compliance systems have gradually reduced friction in GST administration. The steady growth in the GST taxpayer base also indicates deeper formalisation of the economy and improved system maturity.

On the income-tax front, one of the most significant developments was the introduction of the Income Tax Act, 2025, replacing the long-standing 1961 legislation. The new law places strong emphasis on clarity of language and structure. The shift to a single “Tax Year”, aligned with the financial year, is a positive step that removes long-standing confusion around assessment years and simplifies compliance for taxpayers and professionals alike.

From the perspective of individual taxpayers, the enhancement of exemption limits under the new tax regime provided meaningful relief to the middle class. Stability in tax rates, coupled with higher exemption thresholds, has helped improve predictability and disposable income, both critical for voluntary compliance and economic confidence.

As we look forward to 2026, expectations remain high. Stakeholders are hopeful for further GST rate rationalisation, simplification of annual return and audit requirements, smoother system integrations across tax laws, and more effective dispute-resolution mechanisms to reduce litigation.

In a nutshell, 2025 laid a strong foundation for a simpler, more transparent, and technology oriented tax framework. The year ahead presents an opportunity to build on this momentum through consistent implementation and practical reforms.

Wishing all readers a very Happy New Year, and looking forward to continuing these discussions every Thursday in 2026 as well.

Happy reading!

@cbic_india @IncomeTaxIndia

@FinMinIndia

#TaxTalkThursday #TTT #TaxUpdates #TaxReforms #NextGenGST #IncomeTax #TaxProfessionals #CharteredAccountants #TaxCompliance #EaseOfDoingBusiness #NewYear2026

English