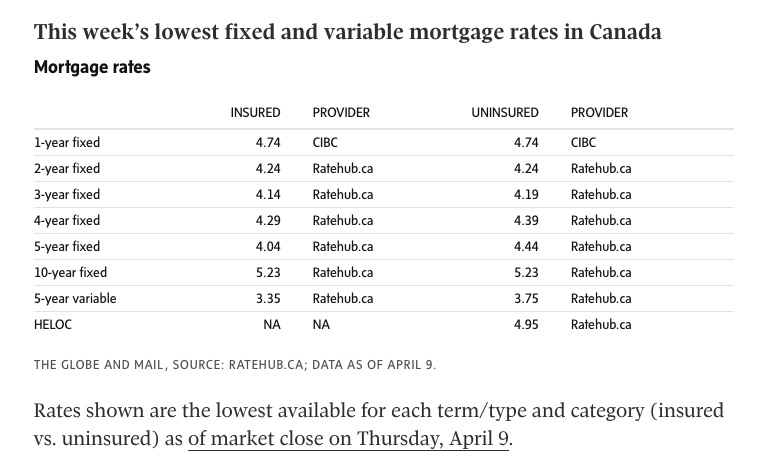

.@globeandmail: You say "Rates shown are the lowest available" in Canada, but there are many lower rates.

Your source (@ratehub) does not disclose all rates. That's not in its interests because it's a lead aggregator (for itself). Change your wording so consumers aren't misled.

Tips on student loans from a 20-year old: use the money only for school; live like a student when you first get a full-time job. Bonus, universal tip: don't carry a credit card balance!

In this month's roundup: A financial foundation is about more than just dollars, but our giveaways are mostly about dollars💰 highinterestsavings.ca/2026/03/savers…

Here’s an hour long video that explains the basics about the different investment accounts available in Canada and how they work (non-reg, RRSP, TFSA and FHSA).

Note: this was a live presentation to the young adult family members of @TIERWealth clients, so the first 5 minutes speaks to that. If you want to get straight to the educational content skip to about the 5 minute 30 second mark.

youtu.be/enP7NiV6wWQ?si…

My thoughts on TFSAs: just invest.

Ideally in one TFSA.

Even better a self-directed TFSA.

Even better a self-directed TFSA in stocks or equity ETFs for income and growth.

And just keep buying more of that.

This year’s RRSP deadline is March 2 if you want to deduct the contribution(s) on your tax return for 2025. Want to brush up on your RRSP knowledge? Take our RRSP quiz! highinterestsavings.ca/rrsp-quiz/

I heard this recently…

"The TFSA and RRSP are identical if your tax rate when you contribute is the same as your tax rate when you make a withdrawal. The only difference between them is that you know what rate of tax applies to your TFSA investment, and you do not know what rate of tax will eventually apply to your RRSP."

Not true. There are many differences between them:

1. With a RRSP you can eventually get a pension credit by transferring money into a RRIF and then withdrawing it when you are over 65. You will never get a pension credit due to a TFSA withdrawal.

2. You can use a RRSP (in combination with a RRIF) to split 50% of the income with a spouse once you reach age 65. You can't do this with a TFSA.

3. With a Spousal RRSP you can lower your taxable income, and then shift 100% of the future income to your spouse. You can't do this with a TFSA.

4. With a RRSP, when you die with a minor child, you can shift the tax away from the deceased’s final tax return and have it taxed in the child’s name by using the RRSP proceeds to purchase a ‘term-certain annuity’ that pays the income out in equal parts annually from their current age until age 18. You can't do this level of estate planning with a TFSA.

5. If you die with a minor who was disabled, you could roll the parent’s RRSP on a tax-deferred basis into a RRSP for the minor (no contribution room required) or into a RDSP for the minor (subject to $200k lifetime contribution limits). With a TFSA you don’t have these same rollover options.

6. If you die with an adult child, who has a disability, and also was financially dependent on the deceased, then the RRSP of the deceased can avoid being taxed on the final tax return by either: rolling it into the adult child’s into RDSP, RRSP, or by buying a life annuity for them.

7. US income in a TFSA is subject to non-recoverable foreign withholding tax, this withholding tax does not apply to RRSPs.

8. TFSA withdrawals create new contribution room as of January 1 the following year. RRSP withdrawals do not create new RRSP contribution room.

There are many more differences as well.

So while the accounts are often said to be comparable on the surface, if tax rates are the same on contribution as they are on withdrawal… when you dig into the details there are many nuances and differences.

Also, I’ll just say that RRSPs are pretty cool for planning… so many tricks.

In this month's roundup: free transfers are coming, tiered rates are here, and everybody loves a good quiz if the scores are anonymous and it could save you money, right? highinterestsavings.ca/2026/02/savers…

In this month's roundup: some savings account interest rates have gone up; EQ Bank buys PC Financial; National Bank buys Laurentian Bank's retail operations highinterestsavings.ca/2025/12/savers…

The highest savings account promo rate is currently at... TD Bank?!? It has a targeted 4-month new deposit promo for existing customers offering 4.90% between October 1, 2025 and January 31, 2026.

In this month's roundup: Neo Financial offers 2.90% if you have at least $20K; Qtrade becomes the 5th Canadian no-commission online brokerage; cash back offers highinterestsavings.ca/2025/11/savers…

If National Bank actually valued Motive Financial, they would have probably kept a separate brand. Sadly, it is not a realistic expectation that National Bank would improve its own offerings as a result of the acquisition.