Sabitlenmiş Tweet

SemiLover

2.2K posts

SemiLover retweetledi

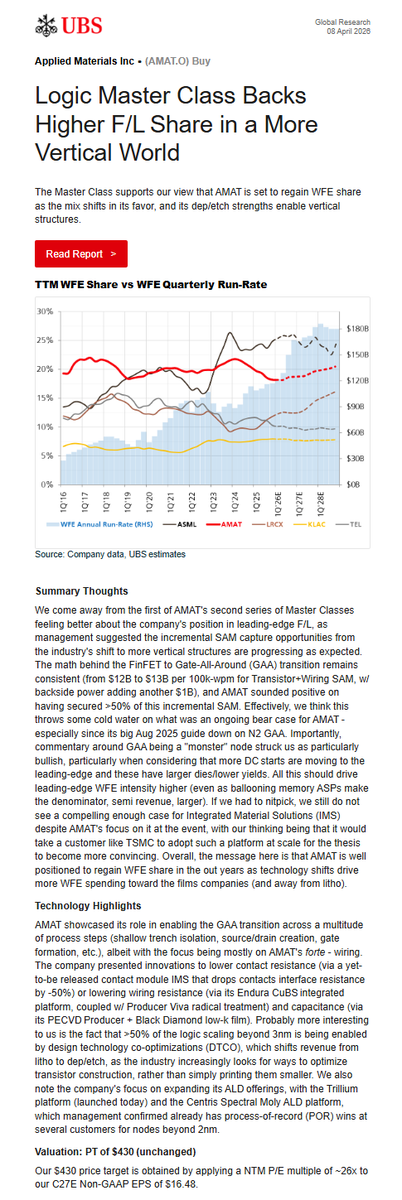

BofA: Anthropic's Claude Revenue Growth Trajectory Could Surprise AWS to the Upside

Anthropic's ARR increased by approximately $21 billion during Q1 (from $9 billion to $30 billion, see Exhibit 1), implying a quarter-over-quarter revenue increase of over $3 billion. Given that a significant portion of Anthropic's workloads run on AWS (Anthropic has reaffirmed that AWS remains its primary cloud provider and training partner), and factoring in the quarter-over-quarter increase in training-related spending, we estimate that Anthropic-related revenue alone could contribute over $1.3 billion in quarter-over-quarter growth to AWS revenue in Q1. This significantly exceeds the current Street consensus, which implies approximately $1 billion in quarter-over-quarter growth (we estimate Amazon's total quarter-over-quarter growth could reach $2 billion). Looking ahead to Q2, we project that Anthropic alone could contribute an additional $1 billion-plus in quarter-over-quarter growth.

$AMZN

English

SemiLover retweetledi

Barclays Upgrades $MRVL to Overweight from Equalweight, Raises PT to $150 from $105

Analyst comments: "The last few months of 2025 saw the stock weighed down by narratives surrounding Trainium share loss and issues with 1.6T DSPs (see our downgrade). The major change since the downgrade is that industry checks suggest optical ports should double in 2026 and double again in 2027. Our math implies that optical could grow ~90% for MRVL this year and next, even with some share shift to AVGO. We lay out a scenario below that shows that, even when eliminating MSFT entirely, assuming no unit growth at AMZN, and discounting XPU attach, we still get to ~$5 of earnings. We do not agree with those assumptions and are, in fact, more confident in MSFT ramping after the NVDA/NVLink Fusion announcement. This story will come down to executing on a well-understood and bullish forecast, and we think the narrative is shifting more toward optics, where it belongs. Our PT moves to $150."

Analyst: Tom O'Malley

English

SemiLover retweetledi

🚨🔼Marvell $MRVL upgraded to Overweight from Equal Weight at Barclays

Barclays analyst Tom O'Malley upgraded Marvell to Overweight from Equal Weight with a price target of $150, up from $105. Marvell is "first and foremost an optical company and with ports growing rapidly the market growth carries the name alone," the analyst tells investors in a research note. Barclays believes the company's optical business could grow 90% for this year and next, even with some market share shift to Broadcom $AVGO.

English

SemiLover retweetledi

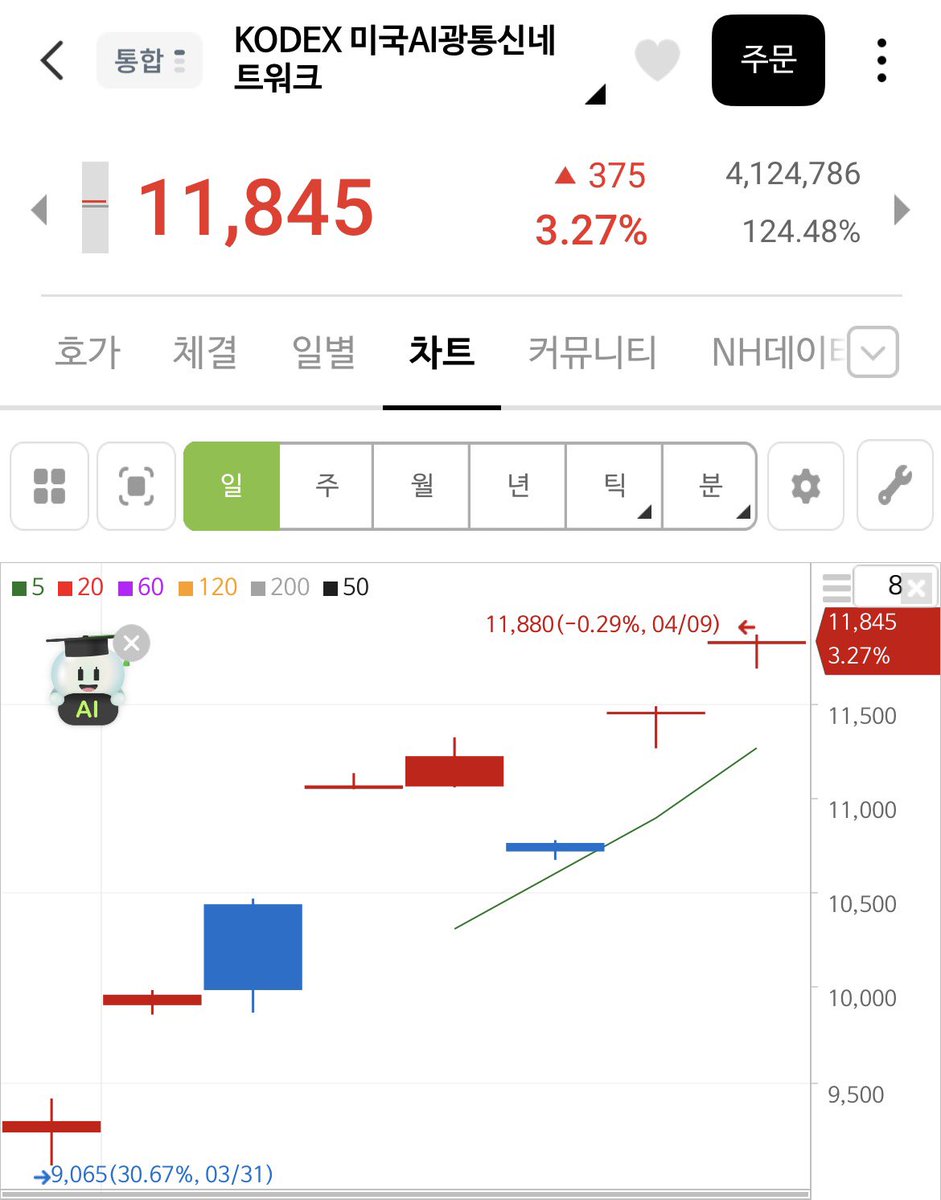

KODEX 미국 AI 광통신 네트워크

뭔데…🔥🚀

골안아파덕@Nice_Stock_

KODEX 미국 AI 광통신 네트워크 ETF 내일 상장🔥 ✅미국 AI광통신네트워크 ETF는 - 데이터의 교통정리를 담당하는 스위치부터 광통신, 무선 인프라까지 각 밸류체인의 지배적 기업을 모두 포함. - AI 데이터센터 확장을 위해 광통신이 꼭 필요함. (전력 효율 & 훨씬 먼 곳 까지 데이터 전송 가능) - 비중: 루멘텀 $LITE 약 23%, 코히런트 $COHR 약 20%, 시에나 $CIEN 약 21% 등 Source: samsungfund.com/etf/insight/ne…

한국어

SemiLover retweetledi

올해 Photonics는 시작도 안함.

단순히 NVIDIA만 봐도 엄청난데 다른 수요까지 합하면 예상도 안된다.

$LITE, $COHR, $GLW

2026 엔비디아 최신 아키텍처

: Vera Rubin

랙 하나에

GPU 72개, CPU 36개, HBM 576개

구리케이블 5184개(72×72)

그럼 광케이블, 레이져 개수는?

광케이블 0개, 레이져 0개.

랙 100개에

Spectrum-6 스위치로 연결시

GPU 7200개, CPU 3600개, HBM 57600개

구리케이블 518400개(72×72x100)

그럼 광케이블, 레이져 개수는?

광케이블 28800개(광섬유가닥 460800개), 레이져 460800개

CPO 최적화 적용 시 레이져 115200개

—

2027 엔비디아 최신 아키텍처

: Ultra Rubin (Kyber NVL576)

랙 하나에

GPU 576개, CPU 144개, HBM 9216개

구리케이블 0개(내부 케이블 최소화 기준)

그럼 광케이블, 레이져 개수는?

광케이블 0개, 레이져 0개.

랙 100개에

Spectrum-6 스위치로 연결시

GPU 57600개, CPU 14400개, HBM 921600개

구리케이블 0개

그럼 광케이블, 레이져 개수는?

광케이블 230400개(광섬유가닥 3686400개), 레이져 3686400개

CPO 최적화 적용 시 레이져 921600개

(시스템을 구성하는 기본 단위가 8배 커졌고(랙 1개 > 랙 8개 규모), 칩당 HBM 탑재량이 2배 증가(8개 > 16개)했기 때문에 총 16배(576개 > 9,216개)라는 극단적인 수치 차이가 도출됨)

한국어

@JasonrShuman —that have accumulated proprietary enterprise data over time within the semantics of their own software.

English

@JasonrShuman In my view, SaaS companies that are likely to benefit from AI are those that go beyond deterministic functions and are not just single applications, but are deeply integrated into enterprise-wide workflows—such as ERP, databases, mission-critical systems, and cybersecurity firms

English

SemiLover retweetledi

Only 7 vertical SaaS companies trade over $10B.

~30 horizontal SaaS companies do.

The reason is simple:

Vertical SaaS competed for IT budgets.

Vertical AI competes for labor budgets.

ACVs and outcome-based pricing for vertical AI businesses are already showing that.

This unlocks larger outcomes.

English

SemiLover retweetledi

$MU $DRAM Annual contracts are dead.

Samsung, SK Hynix, and Micron all moving to 3 to 5 year LTAs with hyperscalers.

Key customers include Microsoft Google AMD and other major cloud service providers such as Amazon Meta Alibaba and ByteDance.

New contract terms feature volume commitments minimum annual supply levels prepayments of roughly ten to thirty percent of contract value and pricing mechanisms to handle market volatility including minimum price floors.

Negotiations for several deals are in advanced stages or expected to finalize in the first half of 2026 with Samsung applying the new policy to contracts starting this year.

Trade Whisperer@TradexWhisperer

$MU Micron signed its first-ever 5-year Strategic Customer Agreement, moving well beyond the typical one-year deal. Ignore the FUD

English

SemiLover retweetledi

I like how writing @DiligenceStack forces me to go do research I wouldn't normally have to do on the client side. But it's making me go from from the weeds of semis and now to the soil.

All of that to say I'm now looking into Soitec lol.

English

SemiLover retweetledi

I heard people may be starting to look into $RMBS. I published (in February) an interview with their SR Fellow of Labs on how the memory industry is being pushed forward with their IP. Hope it helps.

thediligencestack.com/p/memory-infra…

English

SemiLover retweetledi

SemiLover retweetledi

I’ve been saying this for years. CPO is a process, not a product. And he’s right that TSMC is going to use this process to build a moat.

Ben Bajarin@BenBajarin

I'm glad TSMC COUPE is getting more attention of those in the weeds in optics. Our view: "TSMC is increasingly positioned to occupy the same role in silicon photonics that it came to occupy in advanced AI packaging." thediligencestack.com/p/tsmc-coupe-w…

English

SemiLover retweetledi

Are we at the top of the optics cycle?

$LITE $COHR $AAOI $POET $AEHR

What I think gets lost in this conversation is that there are really two different questions here.

The first is whether we are near the late stage of the actual optical hardware buildout. The second is whether we are near the peak of the investment cycle for optical stocks. Those are related, but they are not the same thing, and I think treating them like they are the same leads to bad conclusions.

On the physical buildout side, I do not think we are close to the peak of optical content in data centers. Data centers are still getting larger, campuses are still expanding, speeds are still moving higher, and the amount of optical content required per build keeps increasing. As long as hyperscaler and AI infrastructure spending continues to hold up, the direction of travel still looks very clear to me. More data centers, more bandwidth, more optical interconnect, more optical complexity. That part of the story still feels early relative to where this ultimately goes.

The investment side is different, and that is where I think people need to be more nuanced. I do not make decisions based on whether retail is “getting in” or whether a theme feels crowded on social media. I care much more about what the companies are actually saying and doing, how they are executing, how the stock is reacting to real milestones, and whether the earnings power is moving the way I expect.

For the names I have the highest conviction in, my view is still that if the buildout continues as expected, these businesses should grow revenue very meaningfully over the next few years, with better margins and stronger earnings power. That is the core of the thesis for me. The bigger question is not whether the companies can grow. The bigger question is whether the market continues to assign them premium valuations while they grow. That is where the real risk is.

So yes, valuation compression is always something I am watching. I do not think it is the main issue today, and I do not think we are obviously there right now, but it is always on the table. That is also why selectivity matters more here than just saying “optics” as if every company in the group is the same. They are not. Some will execute better. Some will have stronger product positioning. Some will grow into their multiples. Some absolutely will not. There are plenty of names in this space I would not touch at current levels.

That is really how I think about it. I am bullish on the broader buildout, but I am still highly selective on the stocks. I do not lump all photonics companies together, because the dispersion in quality is massive and that is where a lot of the alpha comes from. The opportunity is not just in saying “optics goes up.” The opportunity is in understanding which companies are actually earning a bigger role in the stack and which ones are being carried by theme momentum.

I also think short-term price action in this group is often more about macro and geopolitics than the underlying company story. These are generally higher-beta names. When the market gets hit, optics usually feels it more. When the market is strong, optics can move harder on the upside too. That volatility does not scare me by itself. In a lot of cases, it creates opportunity, especially when I think the fundamental story is still intact and the tape is being driven by broader sentiment.

And honestly, even in a scenario where some of these companies never make new all-time highs, I still think there is a lot of money to be made in the volatility if you really know what you own. That has been a big part of my own approach. When a stock hits a level that I think disconnects from the underlying execution, and I still have conviction in the business, that can be a very attractive setup.

So I think the right posture is not complacency, but vigilance. Stay selective, stay dynamic, stay close to the companies, and be willing to adjust

moxi@moxnq100

@crux_capital_ dont you think we might be at the top of the cycle with how retail got into photonics now?

English

SemiLover retweetledi

SemiLover retweetledi

I'm glad TSMC COUPE is getting more attention of those in the weeds in optics. Our view:

"TSMC is increasingly positioned to occupy the same role in silicon photonics that it came to occupy in advanced AI packaging."

thediligencestack.com/p/tsmc-coupe-w…

English

SemiLover retweetledi

$META has unveiled Muse Spark, the first model from Meta Superintelligence Labs and now the most powerful model powering Meta AI.

It adds native multimodal reasoning, tool use & multi-agent orchestration across Meta’s apps with larger Muse models already in development.

English

@JasonrShuman Is it correct to say that if legacy SaaS companies such as ServiceNow or Salesforce successfully transition to an agent-based usage model, their potential growth rates would increase?

English

SemiLover retweetledi

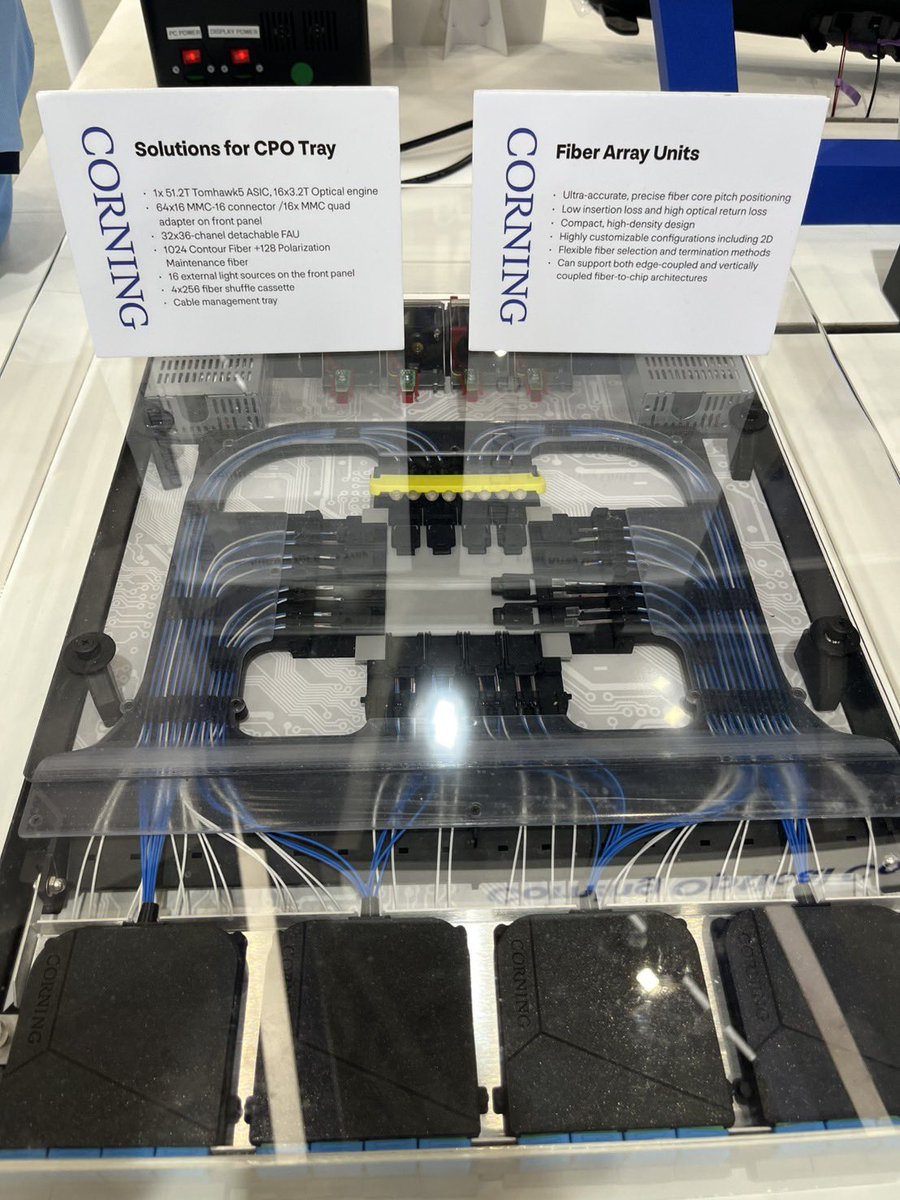

#Corning offers a full-stack CPO optical connectivity solution ranging from SiPh chips to front panels, including detachable FAU, Multi-path interference optimized and bend-insensitive fibers, specialty polarization-maintaining fibers, fiber management tray, internal fiber shuffle, and MMC high-density connectors with blind-mate design support.

open.substack.com/pub/tspasemico…

English

SemiLover retweetledi