Yegor

189 posts

Yegor

@imyegor

Risk & Capital Manager I decide where my time, money, and attention go Act → Learn → Adjust → Grow

Miami, FL Katılım Temmuz 2025

40 Takip Edilen57 Takipçiler

@imyegor @BullflowIO Did you read the huge XLV thesis? Hardly a gamble but def a crazy contract I wouldn’t put a lot into lol

English

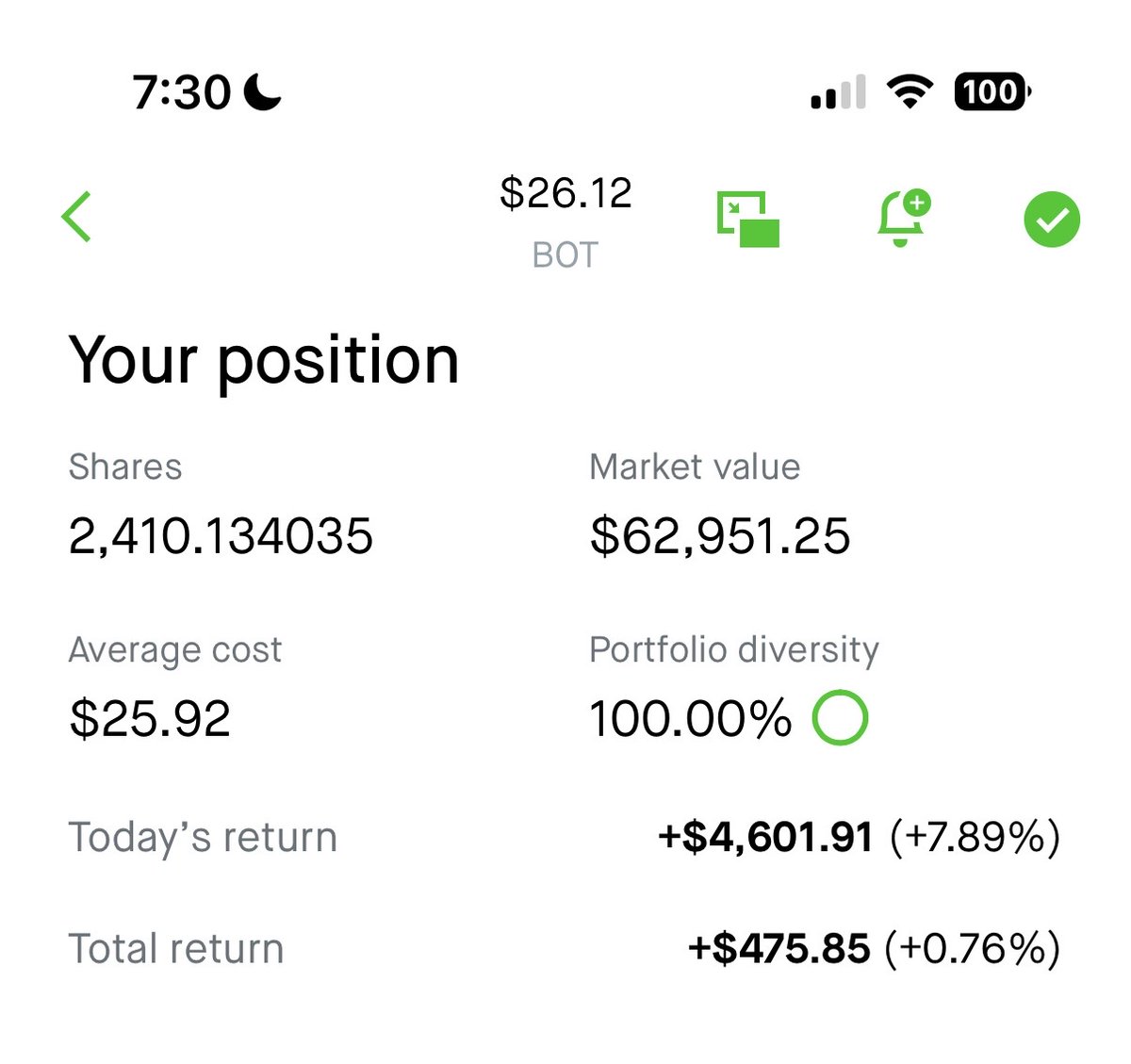

$XLV $600K into July 161c @ .65

I know why...

$CURE

AllllSevens@SevenParr

1 like & less than 1500 impressions on this... 🤨 But institutional money sure is interested... $XLV with significant dark pool activity today. Nothing crazy but I've outlined quite the compelling thesis below. This is a top focus of mine. $CURE

English

Yegor retweetledi

Been digging into $UMAC, trying to understand why the analyst numbers seem so off compared to CEO Allan's statements and my own guesstimates.

The consensus FY27 revenue is about $50M.

A recent Litchfield Hills report targets $50M top line for FY '27.

Needham has a FY26 estimate of $40M (raised from $25M after Q1) and a "clear path to a $100M run-rate by FY27", which implies Q4 27 at $25 M. Scale that back through the year for a FY target of about $55M to $65M

Roth Capital and Jones Trading give a $25 and $20 PT respectively, but I can't find explicit top line projections. Working backwards I figure they're modeling about $50M in FY27.

CEO Allan Evans, on the other hand, has been pretty consistent across multiple channels (AlphaWolf, the Q1 call, and the White Diamond piece). The targets he keeps repeating:

- 1,000+ employees

- 100-120K motors a month

- 140K sqft of factory footprint

- $250M top line FY27 from the Drone Dominance Program alone

This is a $200M discrepancy on the top line between Allan's commentary and analyst targets. Sooooo.... what gives? Either Allan, or the analysts, are off by an order of magnitude. This is the kind of gap worth digging into.

I want to zoom in on the headcount, both because it's something Allan has articulated as an indicator, and because it stood out to me in the CC+Shareholder letter.

To give a quick timeline, as reported in the last 10K:

- Mar 31, 2025: 18 employees

- Dec 31, 2025: 81 employees, $4.9M revenue

- Mar 6, 2026: 141 employees, $8.1M revenue

Then on the Q1 shareholder letter and CC we were informed they're at 200 employees, and still hiring.

So, +60 employees in roughly six weeks between the 10k and Q1. 10 employees per week. With about 85 weeks between May 14th the end of '27, 10/week would put us right at the 1000 employees Allan has targeted.

Interesting.

In Q1 they did $230k/employee annualized ($8.1M / 141 * 4), fueled by a jump in B2B revenue from basically 0 to $7.3 million. Don't forget this number includes new hires, trainees, those not yet truly productive. Compare this to Q4 where they did $240k/employee, annualized, at 81 employees.

Headcount increased 75% while rev/employee basically stayed flat. This suggests to me that UMAC is effectively hiring into demand.

What's more, the ratio between 'productive' and 'trainee' only improves from here. I expect we'll see a bit of improvement and then leveling out.

Side note: they're investing in more factory automation equipment, which should eventually boost rev/employee. I don't think $300k/ is out of the question down the road. Not using that number though.

Putting that all together, if we get to 1000 employees by end of '27 and pencil in $250k/employee, we get $250M top line. Right in line with what Allan has targeted.

Interesting.

So the pace of hiring is on track, and Allan's top line is a reasonable target if both hiring keeps pace and Allan can put 1000 people to work at a $250k annualized rate.

Are there structural barriers to hiring? No, not at all. A recent Bizumentary highlighted how the job requirements can all be taught on site. The factory has a notable contingent of former food service workers. Labor pool is effectively infinite.

The bigger question is do they have the facilities to support 1000 people?

They currently have 62k sqft of space across 5 facilities in Orlando. Let's look at the timeline:

- Jun 4 '25: 17K sqft motor center

- Oct 30 '25: 25K sqft fulfillment center

- Dec 10 '25: 9.1K sqft HQ

- Dec 15 '25: 4.5K sqft headset production

As of the Q1 CC, Allan intends to expand to 100k sqft by the end of Q2. More expansion is expected by Q4, which puts that 140k sqft '27 target clearly in view.

So hiring isn't a constraint, nor are facilities.

Equipment doesn't look like it's going to be a constraint, either. Note 6 on the most recent 10Q indicates there's 1.3M of equipment related to motor production to be delivered in Q2. This is against 2.5M of currently deployed equipment. I think we can expect that to continue to scale through the Qs.

So we've got what's essentially a doubling of manufacturing related facilities, a 50% bump in equipment related capacity, and a steady pace of hiring to put it all to use. All in the next 3 months... let alone the next 12.

What about raw materials? Considering this is a factory environment, we can use materials+margins to cross-check our headcount based projections, and measure both against Allan's statements.

As of Q1, UMAC had $12M of raw materials and $13.5M of prepaid deposits. This is an expansion from the $4.2M of raw materials and $9.7M of prepaid deposits held in Q4. That's $12M of net inflow in Q1. Subsequent to Q1, UMAC placed an order for $75M of raw materials, to be delivered in Q3.

Let's carry that forward.

As of Q1, GM was 32.8%, but long term run rate is expected to be 40%. Of this, most, but not all, will be materials.

The 10Q states COGS includes "inventory costs, which includes an allocation for labor and rent for our manufactured products, direct packaging costs, and production related depreciation, if any." in addition to "certain shipping and other direct product costs including tariffs".

For Q1, COGS came out to $5.4M. Recall this was on a raw inventory of $4.2M as of Dec.

Let's hand-wave and say that labor, packaging, shipping, and tariffs eat up 30% of COGS, and that materials are the remaining 70%. This will produce a conservative revenue number vs if we give raw materials a heavier weight.

At 70% attribution, raw material contributed $3.8M, which means there's a materials-to-revenue ratio of 54%.

That would project our already-placed materials PO of $75M into $139M of top line alone.

This material should arrive

That's *far* closer to Allan's $250M target than to the consensus $50M.

Here's where it gets interesting: Allan has indicated that the $75M raw materials order is just the first of two waves. Per the April 6th AlphaWolf interview:

"And you know, in a in a week or two, we're going to have to order another 60 to 80 million dollars worth of raw material. Okay, right? And then 6 months after that, we're going to have to order 100 to 150 million dollars of raw material."

Then, on May 5th, 4 weeks later (a little delayed), the $75M order came through. The timeline places the next big order some time around December.

So for FY '26, we've got $25M of current inventory and prepaids, and $75M of new orders. That's $100M of raw inventory bought and paid for. A cold hard fact. With our assumed margins that gives us $185M top line.

Even if you totally ignore Allan's statements about another big order, that blows the consensus '26 and '27 numbers out of the water.

What would the next $100M to $150M of raw materials add? Well, at 54% revenue contribution that'd be another $185M to $277M, putting combined '26 and '27 revenue at $370M to $460M.

👏 Against 👏 $50M 👏 full 👏 year 👏 '27 👏 top 👏 line 👏 estimates👏 (did I emoji right?)

Reminder that Needham targeted $40M for FY '26, and a 'run rate $100M' end of '27. Litchfield projects $35.5M top line '26 and $50M '27.

Neither of these are even in the ballpark of what we can project based on already placed materials orders.

What's UMAC trading at today?

$685M MCAP, with $220M of cash and $60M of short term investments gives us an EV of $400M.

On our already-committed materials, and assumed $180M top line that creates, that's just beyond 2xNTM EV/Sales.

That's cheap, especially considering the defense tailwinds and supply chain mandates, let alone the DJI ban and thus domestic commercial market vacuum.

I call that optionality.

So I'm left scratching my head, wondering what these analysts are thinking, but content to keep buying.

English

One of the bullish facts for $NVDA is the dividend jumping from $0.01 to $0.25. I believe we’ll see $230+ tomorrow.

Yegor@imyegor

$NVDA to 230 after earnings.

English

I don’t see real conviction in your plays. You’re trading pennies and making pennies on these positions while pulling in tens of thousands of dollars every month from subscriptions. + You have a big portfolio somewhere else, yet you only show these tiny trades. To me, it screams that you’re scared of your own trades.

English

If the market were to face a severe top, it would be the most obvious thing ever.

The president literally pumping markets

Gambling services on “investment” apps

Insane parabolic moves ever here

I think that’s why people are so compelled to just be bearish

It’s why I just trust the volume. Only thing that keeps me sane

English

I’m not a Trump fan, and I’m not a hater either. I’m just a realist who looks at both the numbers and how people actually behave.

I’m staying long in this market as long as Trump’s in office. The guy clearly wants the market to do well, it’s good for his image, his legacy, and his friends in business (and his port ofc). He’ll do everything he can to keep it pumping. Sure, there’ll be dips along the way, but big picture, I think it trends higher.

That said, I’m not stupid about it. As a risk manager, I still play both sides and keep some hedges ready.

$SPY $QQQ $IWM $NVDA $AAPL

English

@SevenParr And yes, of course we can go lower, and the odds are fairly high. But it doesn’t really matter to me atp. I’m focused on the long term (and I assume you are too).

English

@imyegor Does that mean we can’t go lower? No not necessarily

But the dip is being bought at scale and we know this

English

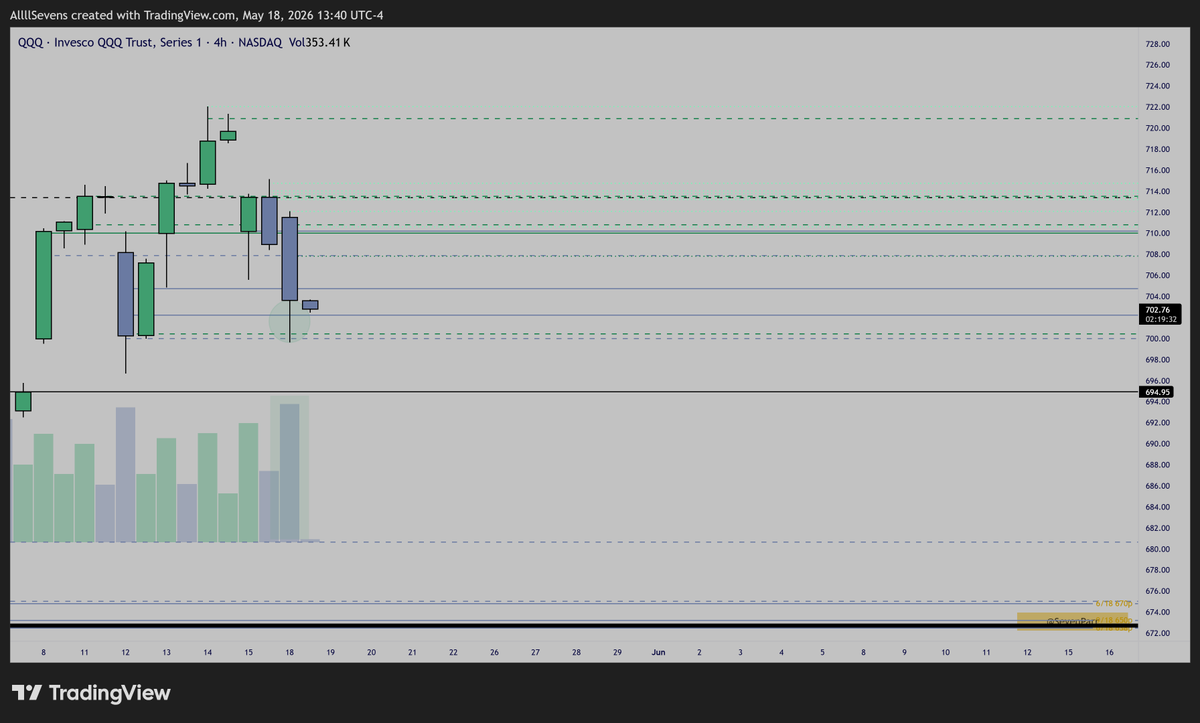

All this talk of puts on semiconductors sure has short-term speculators in a panic, that is forsure- because this mornings long-term accumulation into $QQQ is even larger than Friday's.

Understand what game you're playing.

AllllSevens@SevenParr

$QQQ and another nlod on completely inefficient volume. Don't be fooled.

English

One of the main reasons I followed you is that I saw you focus on the same things I do, volume and accumulation. I don’t trade off historical patterns. For example, this is the 3rd or 4th time we’ve seen the market rip up 20%+ in a month, and according to history it “should” correct. But after watching this market for just over a year, I believe we’re in an environment that can make new history.

English

Yegor retweetledi

$QQQ and another nlod on completely inefficient volume.

Don't be fooled.

AllllSevens@SevenParr

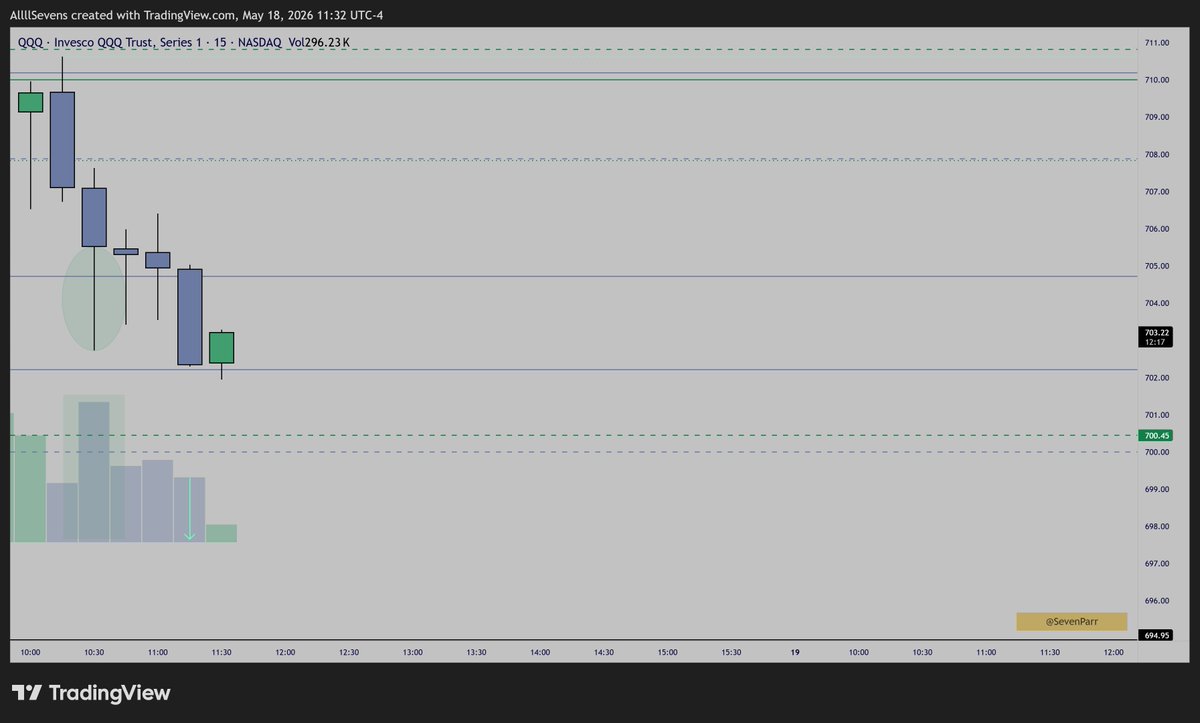

A lot of participants did indeed do exactly that just now. Look at the last 15m candle's volume relative to the inefficient selling prior. All absorbed by Patient Money. $QQQ

English

I’m not defending this guy, but even if you’re a millionaire, it still makes sense to charge people, especially when they’re ready to buy. Take Michael Burry, for example. He’s got millions and still charges for his content. The reason? Recurring income is safer and easier than just risking your own capital. Your name and reputation can print money for you, so why not use it? Even $20 a month from tens of thousands of people can easily make you a million a year with zero risk.

And on the prices — I believe no matter who you are, you get to decide what your knowledge or information is worth. Don’t get mad if someone charges 10x more than others. That’s their choice. You can either pay it, find someone cheaper, or just not buy at all. There’s always a choice.

English

Why on earth do you need to charge 199$ a month if you have 10 million usd in stocks? Like literally just make some profitable trades and you'll make 20x that. Weird ass way to go about it. Id never stoop as low as selling subscriptions for 199$ even if I had 0 dollars in the bank.

If you read this Kevin Xi I think the transparency is cool, but come on 199$? Thats just retarded, especially considering your entire premise is getting people to trade stocks to change their lives, charging people 199$ directly counters that goal.

English

Kevin Xu

- $HIMS was a loss ❌

- $QS was a loss ❌

- Gave up on $IREN ❌

- Multiple pumping post to buy while only risking .5% of his own port

Who is paying $199 a month for this clowns sub? Shameless

Kevin Xu@kevinxu

Call me crazy, but I just made a new trade and its an even bigger banger.

English

Just opened a small position in $ABAT today — 2,000 shares at $3.32 average.

Checked the filings and saw BlackRock and Vanguard doubled down and bought even more, but that’s not really the reason why I’m back in.

I like how the business is actually growing and executing. Yes, there are risks (there’s risks in everything), but I really believe in this company. They do the work.

$ENVX $QS $SLDP $CBAT $ALB

English

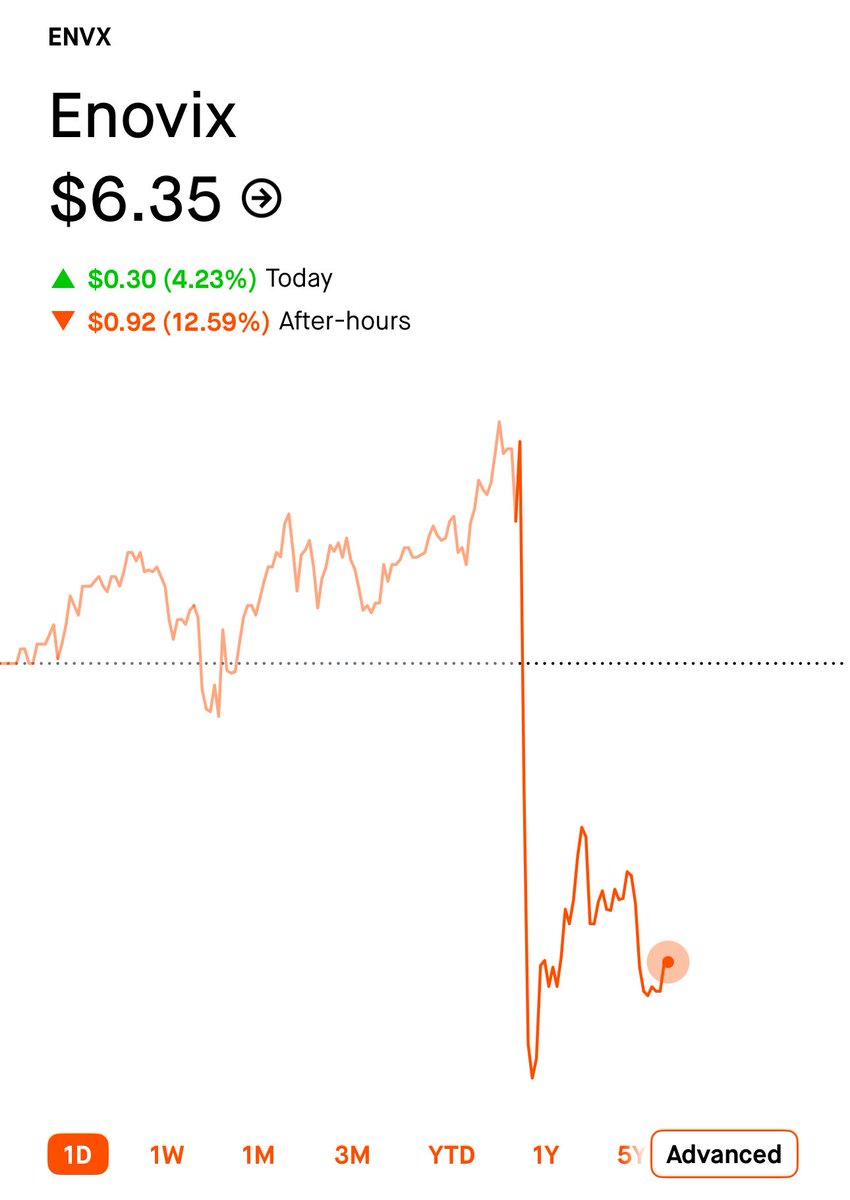

$ENVX looking like a decent buy right now. I traded it last year, they always do that pump & dump thing.

Earnings today weren’t bad at all (still dumped like always). I even think it might dip to around $5.90 first, then they’ll start pumping it.

Let’s wait for tomorrow.

$QS $SLDP $ALB $SQM $TSLA

English