Nocharts

1.2K posts

@Saawankumar786 @KKRiders Is it possible that while bowling green , powell , pathirana and narin

And in batting finn impact in place of pathirana?

English

Fifty up for Suryavanshi!

A solid knock 50 off just 39 balls, building the innings with class and composure

#Suryavanshi #HalfCentury #IPL2026 #KKR #CricketTwitter #InningsBuilder #BattingMasterclass

English

@mohak_ailani Well can it take support near 3000? 10% down on Q42025

English

@nid_rockz @yashkarishma Yes when I asked he replied maybe and Q2Q margin matters for any stock price.

English

@yashkarishma Never wrote waaree Energies number was blockbuster bdw

English

Good #Q2FY26-16/10/25 post 8pm

2 solar related names:

Waaree Energies

#WaareeEner

#WaareeEnergies

Blockbuster Q2FY26 🔥

Record quarter with highest ever revenue, EBITDA, PBT and PAT in comps history

Solid QoQ and YoY uptick

Rev at 6065cr vs 3574cr, Q1 at 4425cr

PBT at 1231cr vs 498cr, Q1 at 943cr

32% QoQ growth

More than 2.7x YoY

PAT at 878cr vs 375cr, Q1 at 772cr

Higher tax paid this quarter

OCF at 574cr vs 1493cr

Solid orderbook

Vikram Solar

#VikramSolar

EBITDA ⏫226% with OPM at 21% vs 12%

Big capacity coming up in Q4 and next phase in FY27

Flat QoQ, Q2 is seasonally lean vs other qtrs

Rev at 1110cr vs 572cr, Q1 at 1133cr

PBT at 185cr vs 11.4cr, Q1 at 182cr

PAT at 128cr vs 7.3cr, Q1 at 133cr

H2 should be much better

OCF at 513cr vs -223cr

Orderbook at 11.15 GW

Q2 module sales at 784 MW⏫189%

84% utilization

Monsoon related logistical challenges in Q2FY26

English

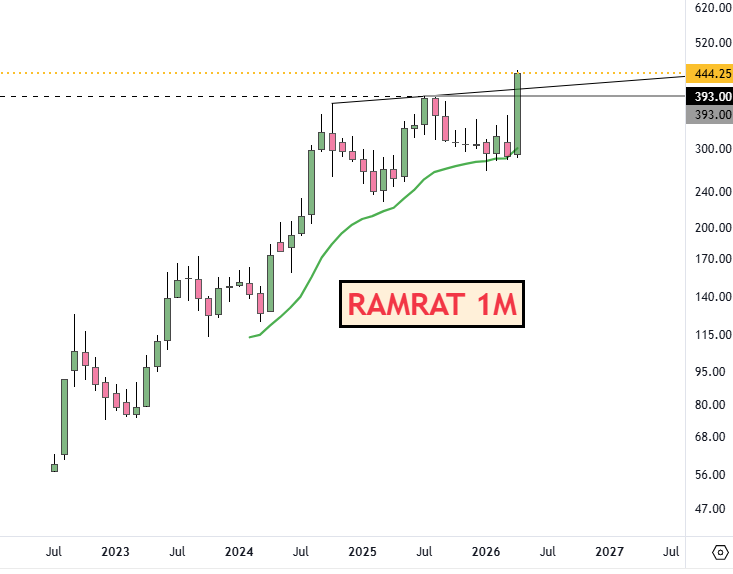

#CNXMETAL Index @ Resistance of TL . Closed good

Rukega Nahin ?

#AEROFLEX

#ALUFLUOR

#BALUFORGE

#BHAGYANGR

#GALLANTT

#GMDCLTD

#HAPPYFORGE

#JAYNECOIND

#PRECWIRE

#RAMRAT

#SAIL

#STEELCAS

#WHEELS

Disc: No Recommendation !! #Trading #StocksInFocus #StockMarket #Swingtrading

English

@swing_blaster Because stock doesn't look back while moving down, but when it's the other way there are resistance, breakout retest , supply zone etc..

English

CDSL at ₹1900 = everyone loves it 😍

CDSL at ₹1100 = no one wants it 😴

HDFC Bank at ₹1100 = everyone loves it 💙

HDFC Bank at ₹800 = no one wants it 😶

HAL at ₹5550 = everyone loves it 🚀

HAL at ₹3500 = no one wants it 🥶

Investor psychology is interesting 🧠📉

Price goes up → confidence goes up 📈

Price goes down → fear takes over 📉

Smart money does the opposite 😉

English

@investor_sr33 Average kar le kya , ya phir 2900-3k levels ki watch kare?

Indonesia

Waaree isn’t just expanding… it’s integrating the entire energy stack.

→ Polysilicon (raw material control)

→ ₹3,900 Cr glass capex

→ Entry into transmission infra

→ BESS + storage bets

→ Global capacity expansion

This is a full-stack energy play being built in real time.

Chenthil@jcrajan00

Waaree Energies just announced a 10,000 crore fundraise to enter semiconductor and solar wafer manufacturing. India's largest solar panel maker is going upstream — from assembling panels to making the silicon that goes inside them. This is the exact playbook China used 15 years ago. Start with panel assembly, capture volume, then vertically integrate into wafers, cells, and polysilicon. India's solar manufacturers are now following the same path, just faster. India installed 25 GW of solar in FY26. We make the panels. We install the systems. But we import 90 percent of solar cells and 95 percent of wafers from China. That 10,000 crore from Waaree attacks the most critical gap in the entire clean energy supply chain. Adani Solar already has a 4 GW cell-to-module line in Mundra. Tata Power Solar is expanding. First Solar is building in Tamil Nadu. But wafers — the actual silicon — is where the real value sits. Waaree going after wafers is a strategic move, not just a capacity addition. If India can manufacture solar wafers domestically by 2028, it breaks the last remaining link of Chinese dependency in the energy transition.

English

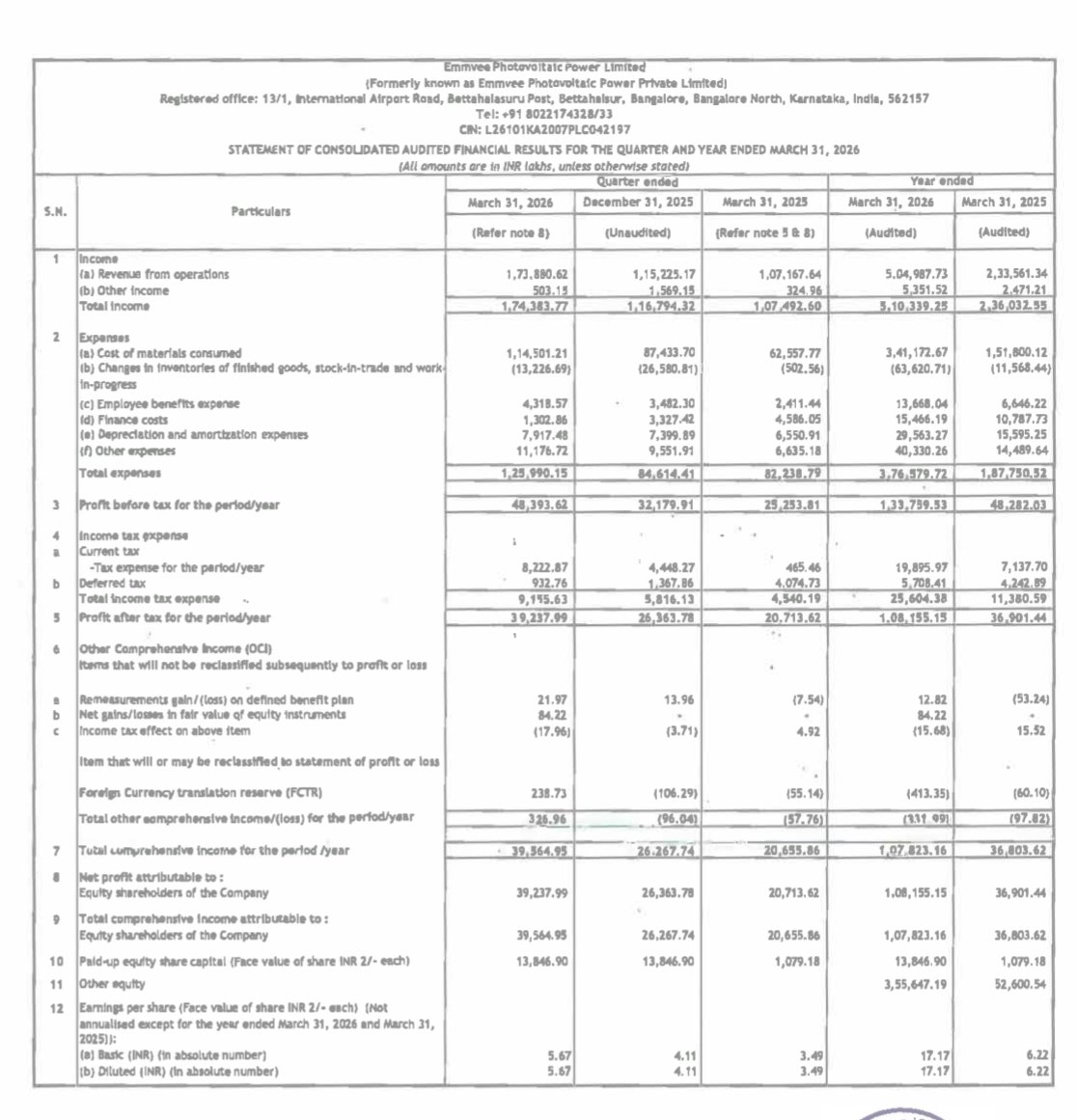

Emmvee Photovoltaic Power

#Emmvee

#EmmveePV

Q4FY26 PAT > FY25 PAT

Crazy execution with timely capacity addition

Blockbuster Q4FY26 👏

Highest ever revenue, EBITDA, PBT and PAT in comps history

Solid QoQ and YoY uptick across all parameters with big growth QoQ and YoY

Rev at 1738cr vs 1071cr⏫62%

Q3 at 1152cr⏫51%

EBITDA at 571cr

⏫58% YoY

⏫38% QoQ

OPM at 33% vs 34%

PBT at 484cr vs 252cr

Q3 at 322cr

PAT at 392cr vs 207cr⏫89%

Q4 at 263cr⏫49%

FY26:

Rev at 5049cr vs 2333cr

PBT at 1337cr vs 482cr

PAT at 1081xlcr vs 369cr

OCF at 200cr vs 625cr

RoCE 38%

RoE 51%

Net cash company

Orderbook increased to 9.4 GW

1.27 GW inflows during Q4FY26

Module capacity enhanced from 6 GW to 10 GW

Installed capacity:

10.3 GW modules

100% TopCON

2.94 GW cells

Cells utilization at 79% during Q4

New capex:

6 GW integrated cell+module capacity

To take Total capacity to 16.3 GW module and 8.94 GW for cells by FY28

English

@shashank_jha_12 Good analysis but Market Also judge quickly as it saw the margin pressure 10% down very next day.

English

Waaree down 10%.

Opportunity or trap?

Comparing Waaree, Vikram, Premier & Emmvee👇

youtu.be/hz1r0AdQ1-0

#StockMarketIndia #Multibagger

YouTube

English

@ThinkWithSaurav @J78Pj Margins (23%) are expected by the Company itself or the analyst?

English

The stock might see a mixed reaction tomorrow. While the 71% profit jump and doubling of revenue are huge wins, the market will notice the EBITDA margins slipping from 23% to 18.6%.

Even with massive growth, cost pressures are starting to hit, with a massive 60k Cr order book and a plan to raise 10k Cr for expansion, it’s a tug of war between high growth and narrowing margins. It’ll be a volatile, watch if the market focuses on the big numbers or the margin dip.

English

Waaree Energies

1. What does the company actually do today?

The company is one of India’s largest solar module manufacturers as you know, it produces and sells solar panels across domestic and international markets, along with EPC and service work.

Revenue (₹14,000+ crore FY25, ₹22,000 crore TTM) and profit (₹1,900+ crore FY25) are largely coming from module sales, exports (especially US), retail distribution, and EPC. So current earnings are fully driven by the solar module ecosystem.

2. How much of the business is BESS today?

BESS contribution today is negligible in revenue and profit terms.

The company has started entering BESS and even won a small order (10 MWh), but there is no meaningful revenue yet. So BESS is still early stage and not contributing to earnings today.

3. Where does the company sit in the BESS value chain?

The plan is to be fully integrated from cell to battery pack to container-level solutions.

But currently, it has no operational scale in BESS. It does not yet control large-scale manufacturing or execution in this segment. So positioning is future integrated player, but current presence is minimal.

4. What is the core business model?

The business is product based manufacturing supported by EPC and distribution. Revenue comes from selling modules, executing projects, and retail network sales.

This creates repeat demand, but still depends on continuous order inflow. It is not annuity-based, and a large part of revenue is project or order driven.

5. What is the quality of revenue and visibility?

The company has a very strong order book (₹60,000 crore) and large pipeline (100+ GW), which gives strong near to medium-term visibility .

However, revenue is still execution-based. Orders need to be delivered and depend on project timelines. So visibility is strong but not fully predictable like annuity income.

6. What is the execution status?

Core module business is fully operational with large capacity (20+ GW) and strong execution track record.

New segments like cells, wafers, BESS, inverters, and transformers are under execution with clear timelines (FY27–FY28). BESS specifically is still in early build-out stage.

7. What will drive margins in this business?

Margins are currently driven by scale, export markets (especially US), and premium segments like retail and EPC.

Future margin improvement depends on backward integration (cells, wafers) and moving into higher-value segments. But base module business still remains competitive and price-sensitive.

8. What is the financial strength of the company?

The company has strong profitability and operating cash flow generation (₹3,000+ crore CFO in FY25).

At the same time, debt has increased (₹2,900+ crore) due to expansion. So financial position is strong, but capital deployment is increasing alongside growth.

9. How capital intensive is the business model?

This is a highly capital-intensive business, especially with full backward integration and new areas like BESS.

The company has announced very large capex (₹25,000+ crore overall plans including BESS ₹10,000 crore) . So growth depends heavily on continuous capital investment.

10. What are the key risks in this business?

Pricing pressure in modules is a key risk since it is a competitive global market.

Execution risk is high due to multiple large projects running together (cells, wafers, BESS, US expansion). Policy changes and global trade dynamics (like US tariffs) also remain important risks.

11. What are the key triggers and timelines?

Near-term triggers include execution of large order book and continued export growth, especially in the US.

Medium-term triggers are commissioning of cell, wafer, and BESS capacities (FY27–FY28). These will decide whether the company successfully moves up the value chain.

12. What is management saying vs what is visible?

Management is positioning the company as a fully integrated energy platform — covering modules, cells, wafers, BESS, hydrogen, and power infrastructure. The narrative is of becoming an end-to-end energy transition player .

What is visible today is still largely a solar module-driven business. Revenue and profit are coming from modules, EPC, and exports, while new segments like BESS and hydrogen are still under development and not contributing meaningfully.

13. What is the real variable to track here?

The company is currently generating strong earnings from modules, supported by scale and export demand.

At the same time, it is deploying large capital into integration and new segments. So the key variable is whether this capital allocation actually converts into future profits, or if returns remain dependent on the core module business.

English

#waareener requested chart*

CMP 3438

Made a big base and trying for Bo so keep an eye . As of now trading above 50/200 ma so looks good on chart. What do you think will it give strong Bo on chart this time or fall like before ? 🤔 expected level 4557 based on current base and only applicable after confirmed Bo. Retrace levels 3307, 2869, will it touch these levels or not ? What ur views?

Disclaimer no buy sell recommendation

#stockstowatch

English

#premierene requested chart*

CMP 1003

After listing its in downtrend, struggling to break TL but this time it’s trying hard, let see weekly candle will sustain above this TL or not? As of now trading above 50/200 ma so looks good on chart. Congestion at 1098, what do you think will it cross this level or get electric shock ⚡️? 🤔 retrace levels 973, 945. Disclaimer no buy sell recommendation

#stockstowatch

Ratan Roy@RatanRoy836579

@ranu5 Premier energy mam chart plz

English

#SAKAR 629 & #ASTERDM 705

Hv been My Fav in Hospital space to #trading

Disc: No Recommendation !! #Trading #StocksInFocus #StockMarket #Swingtrading

English

@WasimJaffer14 If he wouldn't have played 84(49) against the USA in the world cup 2026

match was long gone, india would have stranded with 6 left handed batsmen.

English

Nocharts retweetledi

I am accumulating this Gem. Can any one gauge this? Image is Ratio Chart.

English