The Insider

5.3K posts

You are correct Tim. You always pull it off to explain these insanely complex topics in such an easy to understand way.

Indeed, as I said for the economics part, it's more of an alert than a real issue. It's just part of the business. Reputable sources also told me this wasn't the first time a CNL trigger was breached.

English

I tried writing a deep dive on the $SoFi ABS situation but I have decided not to publish it.

It became far too technical and would likely only spread confusion.

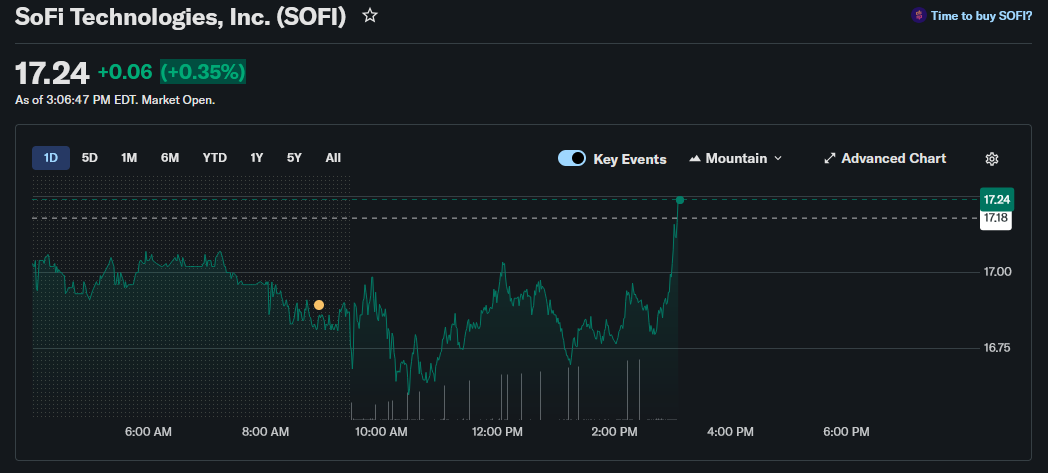

I'm pretty sure this correlated to SoFi heavily underperforming every other financial in the past few weeks.

Institutional investors got access to this information way before we did. I bet 99% of you didn't even know what I'm about to share.

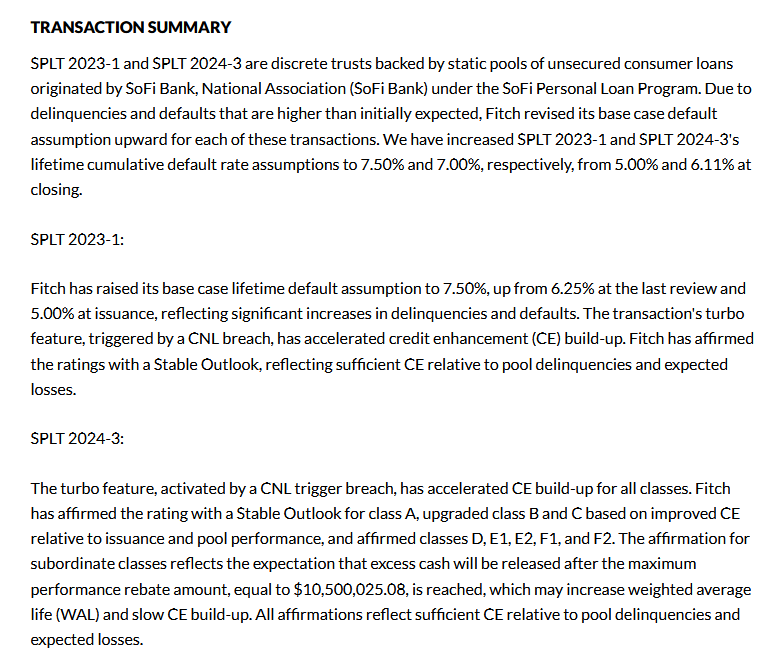

The short version is that SoFi Consumer Loan Program 2025-1 has breached its cumulative net loss trigger of 2.60 percent. I'm pretty sure that this is the first time this has ever happened to SoFi.

The December 2025 distribution report already showed cumulative net charge offs at 2.15 percent on a pool amortized down to 60.11 percent of original balance. Subsequent performance has now crossed the line.

No matter your perspective, this is not a good sign.

However, it does not mean this is devastating for $SoFi's Loan Platform Business or even the personal loans they keep on their own balance sheet.

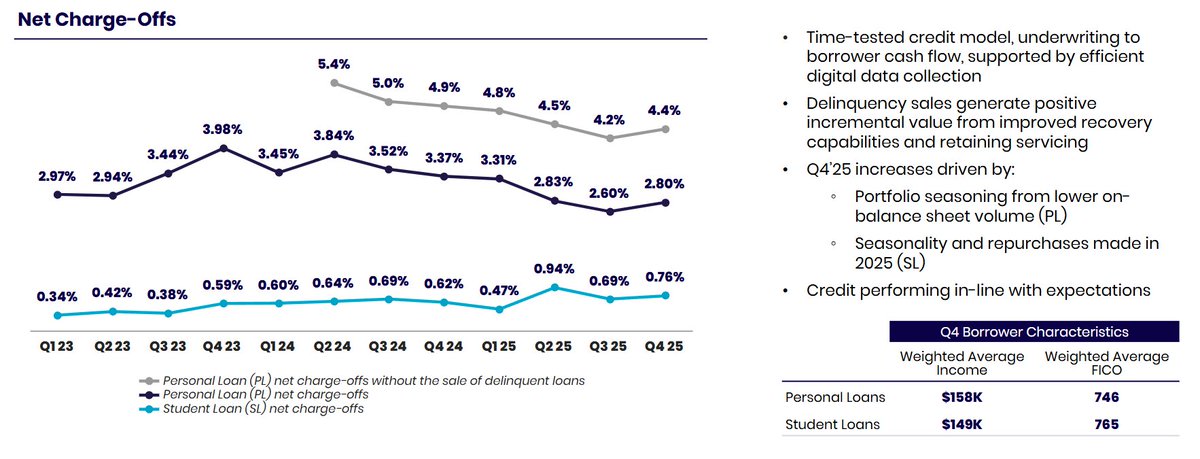

SoFi’s corporate level personal loan net charge off ratio actually improved to 2.86 percent in 2025 from 3.54 percent the prior year.

The 2025 1 trust is one specific vintage under pressure, not a proxy for the entire book. What this means is more technical but still important.

When a trigger like this is breached, the securitization structure shifts into a more defensive mode. Excess spread is diverted away from subordinate tranches and residual holders. Senior note amortization accelerates through turbo principal paydown. Overcollateralization steps up further and cash is trapped to protect the bond stack.

Current senior credit enhancement stands at approximately 14.04 percent, meaning the senior AAA notes now have significantly more protection than they did at issuance.

Importantly, rating agencies have not changed their ratings. Morningstar DBRS continues to rate the senior Class A notes AAA(sf), confirming that the structure still provides strong protection to bondholders even after the trigger breach.

In other words, the structure is doing exactly what it was designed to do when credit performance weakens.

Economically, the impact for SoFi would likely be real but indirect. It touching servicing valuations, future gain-on-sale economics, repurchase liabilities, and new LPB pricing.

In a market this fragile, I do not want to throw highly technical credit analysis into the timeline and watch it get turned into panic and FUD.

Once people see phrases like trigger breach, deteriorating credit, nuance dies immediately.

My draft was not a bearish article. It was about the technical explanation and the broader warning on capital markets dependence, while highlighting that SoFi’s on-balance-sheet personal loans continue to perform well and distribution to private credit buyers remains robust.

But I know how this platform works. So rather than contribute to confusion, panic, or oversimplification, I would rather hold it back.

Sometimes the responsible move is not posting.

And btw, that short report was ridiculous. Always funny when people discover fair value accounting. Must've been an intern writing that short thesis. But yeah, I'm just buying the dip and not selling a single share.

I'm still spending time on the Private Credit article I promised you guys, it's way more work than I expected, but a deal is a deal! It actually reminds me of my Master's thesis lol. Anyway, have a great day everyone.

English

QME

@insiderinvests @AverageDipBuyer Interesting...where is this chart from?

English

@ChrisK3861 Normally it's published on here. I've got this information from reputable sources, couldn't find any links myself either. Check my reply on Vadim, that gives some more context. fitchratings.com/research/struc…

English

$sofi

People here need to stop giving any credit or time to the Muddy Waters report

There's virtually nothing that they concluded that has any basis in fact and is pure conjecture and emotional provocation.

By reasserting their claims for content clicks, you actually assist their false narrative

English

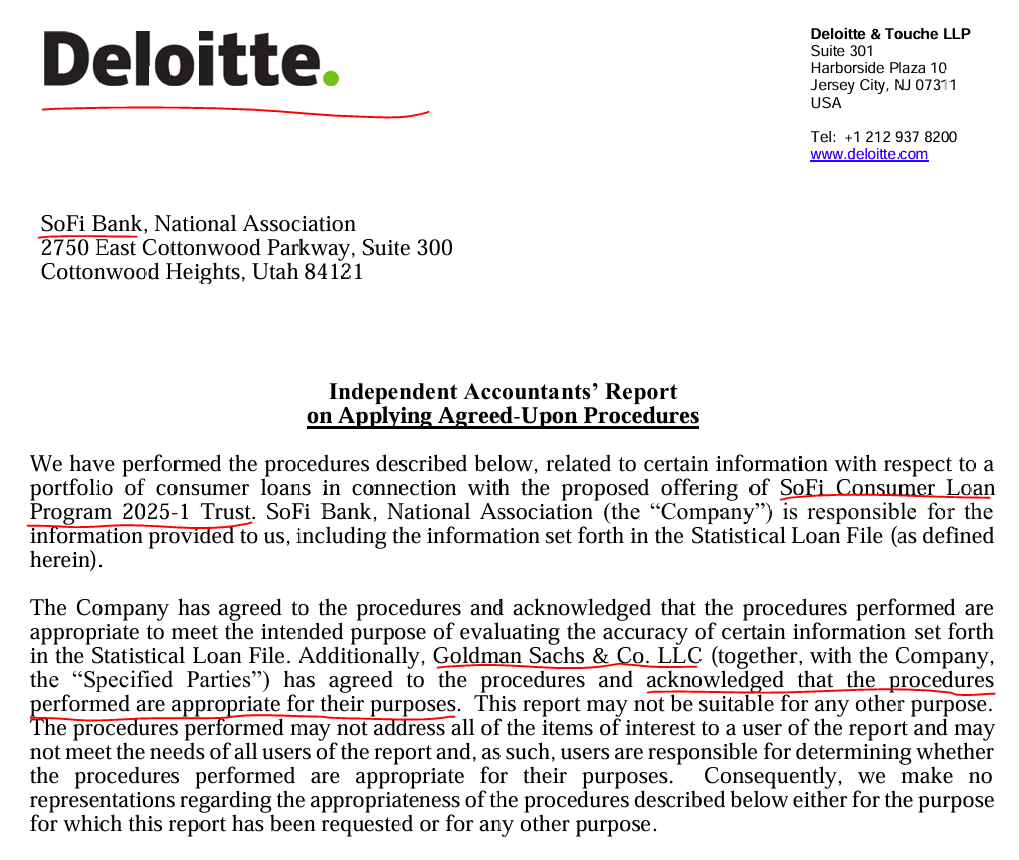

It's true, Deloitte audits $SoFi's loans

Goldman Sachs acknowledged that the procedures performed by Deloitte are appropriate for their purposes

Get f*cked bears

English

Holy sh*t

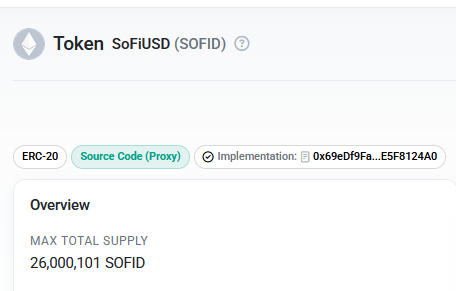

The $SoFi stablecoin just went from $16 million to $26 million

English

@LxntedF74275 The market anticipates bad news, that is why stocks are down

English

@ste16390 Yeah, that is a non-issue, everything will be okay related to the macro

English

Everyday we here how SoFi is doing this and that incorrectly and even fraudulently - a complete joke. Yet, the company continues to gain respecability. Is Mastercard going to partner with a loser? Has JD Power been hoodwinked - and put their reputation at risk? These things just happened in the last 2-3 weeks. Think about it.

English

The Insider retweetledi

$SOFI

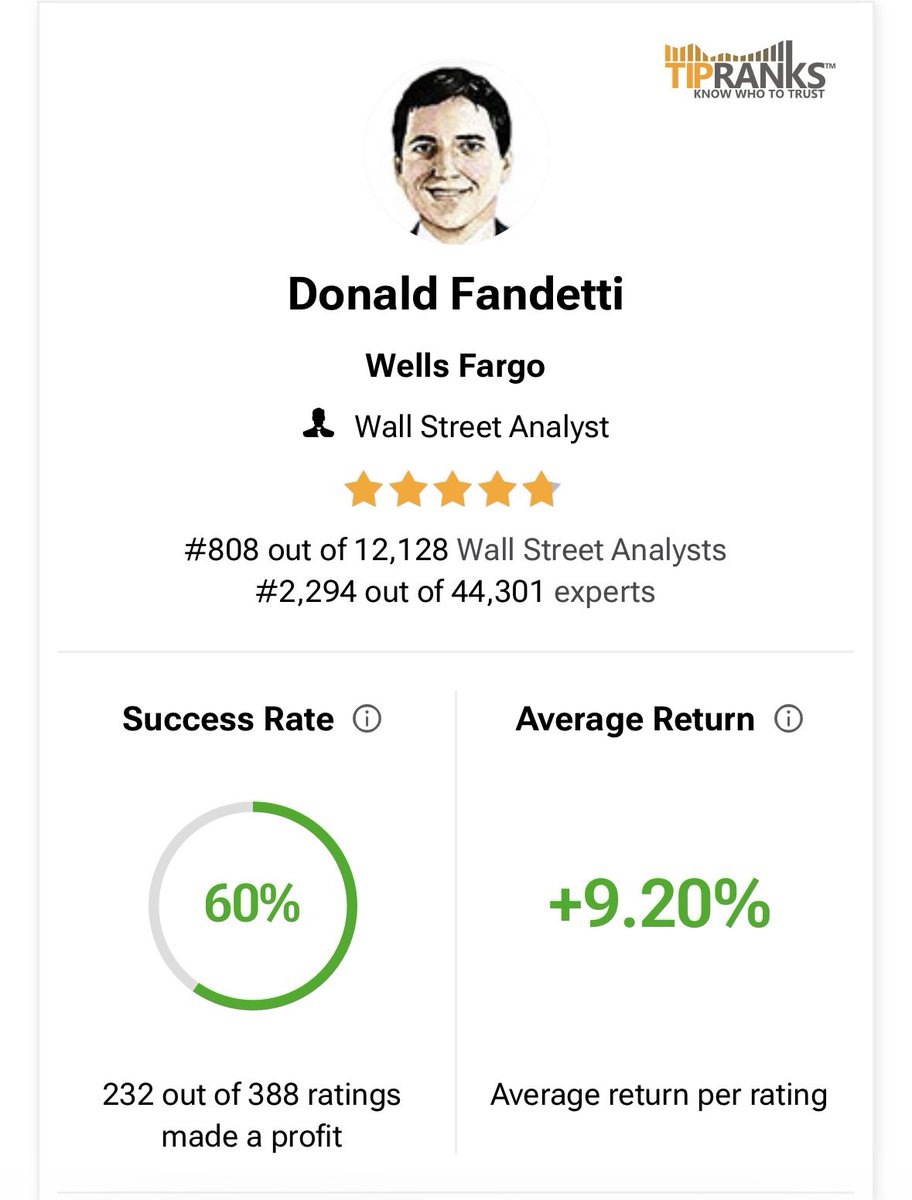

Donald Fandetti @ Wells Fargo today initiated a hold rating on SoFi Technologies, and set a PT of $19.

He says “the company is a digital leader sitting at the nexus of technology and financial services”.

Wells says that while SoFi has “strong” earnings growth its neutral rating reflects the stocks valuation and the company’s loan sale risk.

English

The Insider retweetledi

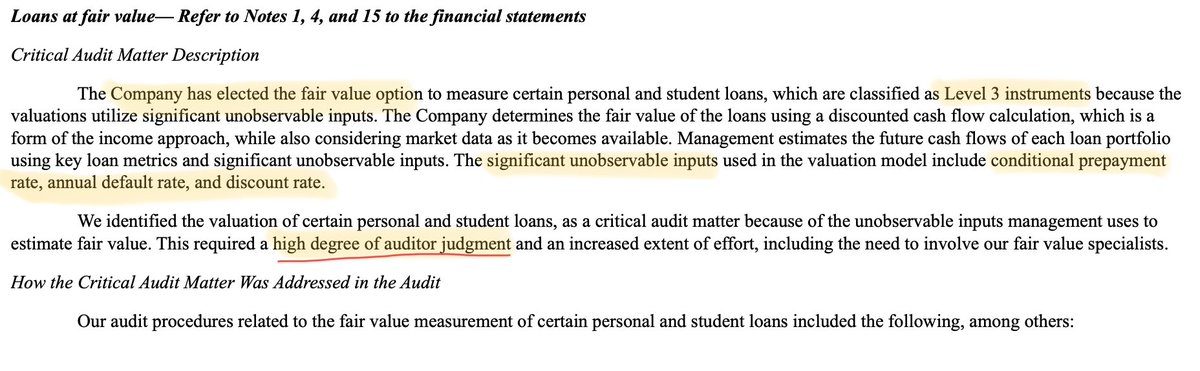

Shorts keep yelling “Level 3 = fake” but the 10k literally spells out the opposite.

$SOFI values loans using DCF with explicit assumptions for defaults, prepayments and discount rates and those inputs aren’t soft. Default assumptions run as high as 18% and discount rates approach 19%.

That’s not aggressive accounting that’s building in downside.

More importantly, Deloitte didn’t just “review” this. They flagged it as a critical audit matter, brought in valuation specialists and ran independent fair value estimates against management’s models.

And the sensitivity tables make it even clearer: if defaults rise or discount rates move up FV drop mechanically.

So the entire “inflated asset” narrative hinges on ignoring disclosed assumptions, ignoring audit work, and pretending Level 3 = manipulation.

I see model risk. I don’t see deception.

English

The Insider retweetledi

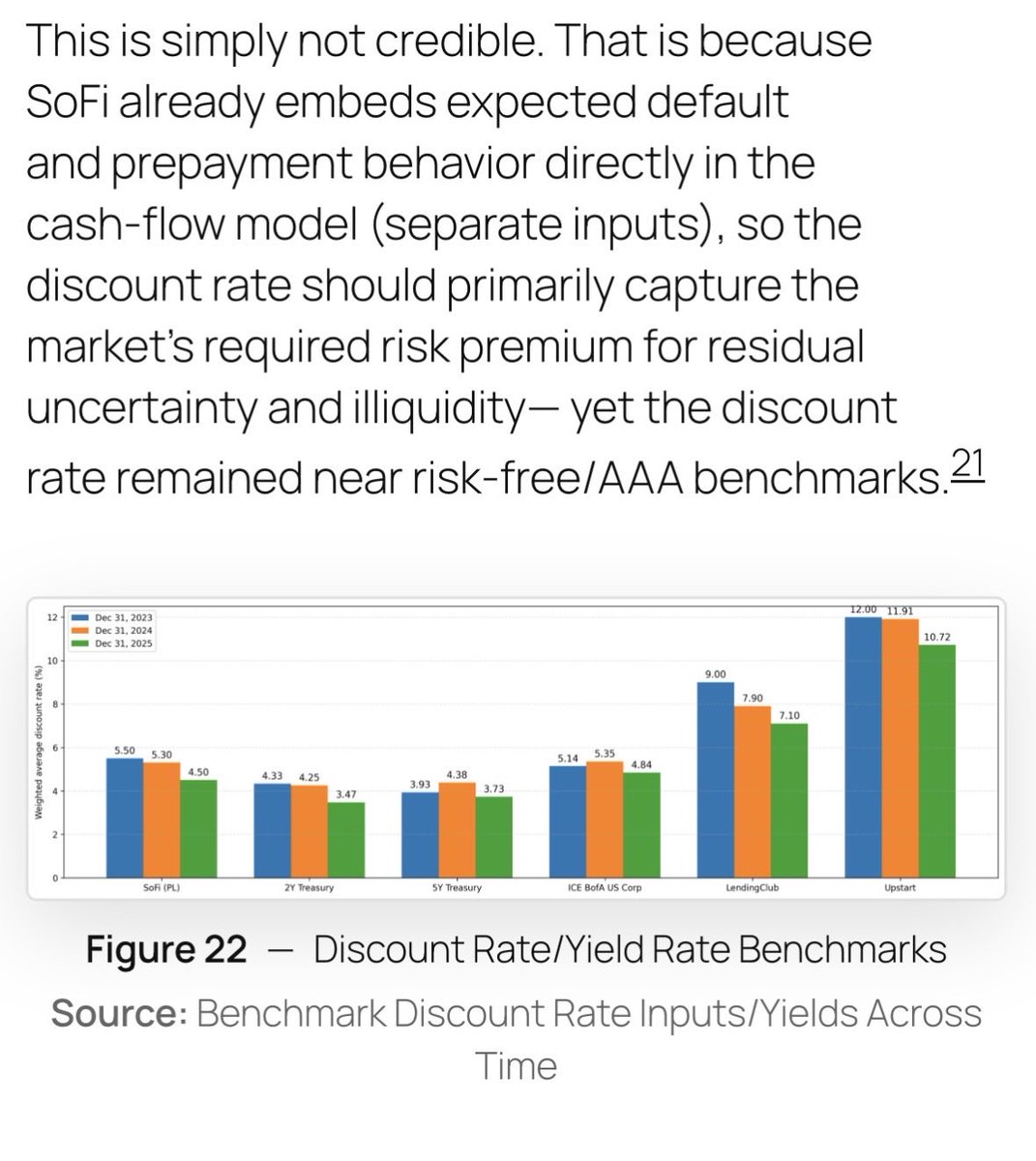

$SOFI… It was a lot for the shorts to put together such a long piece. Some of the issues look like they accidentally compiled some documents out of context. Example, net of hedges on a structured product is not always added to and end market value of loans directly. Particularly true if it was taken over a period where the underlying has been sold.

I’m exhausted and may not have time to check this and demonstrate. However, the below illustration gives you a sense for what I mean by the need to double check apples to apples.

This bit compares loans across treasuries of different durations and companies. I don’t know $LC and what their mix of loans was. But $UPST? That’s straight garbage (junk loans). $upst management tells you they mostly kept the lower buckets of credit risk to improve their model.

English