Jorge

3.1K posts

Jorge retweetledi

San Lorenzo Gold Corp. reported $drill results from the extension of its Arco de Oro target, including 102.3m of 1.33 g/t #gold. 3.9 km step-out continues to highlight the scale potential of the broader ##porphyry #copper-gold system.

Full news - tinyurl.com/nhhzreen

$SLG.V

English

They can't even drill a geotechnicall hole for the adit without hitting a new zone of great mineralization 🙃

Junior Mining Network@JrMiningNetwork

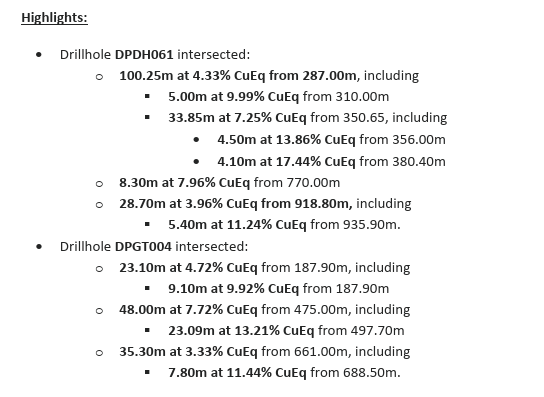

NGEx Drills 34m at 7.25% CuEq plus 48m at 7.72% CuEq, 180m Apart in Mars; Discovers New Zone 300m East of Mars with 23m at 4.72% CuEq $NGEX.TO tinyurl.com/2botc8zd

English

Jorge retweetledi

$KOS $TLW

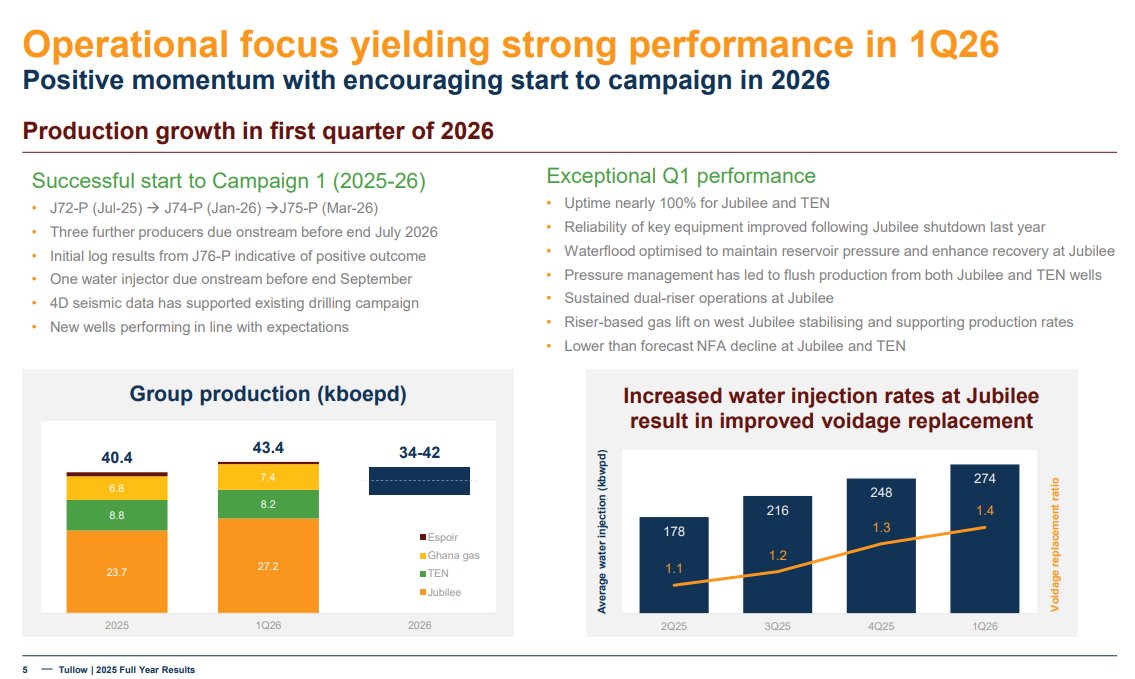

Tullow reported its well-known FY results yesterday, after Kosmos had already announced its annual earnings. Tullow also posted an impressive Q1 performance, which bodes well for Kosmos's Q1 report scheduled for next Tuesday, the 5th.

We do not own bonds or stocks in Tullow, but it is important to monitor them since it operates the Ghana assets in which Kosmos has a significant stake. However, Tullow divested nearly all its assets in 2025 and is now focused only on Jubilee, TEN, and Côte d’Ivoire. But Côte d’Ivoire’s contribution is minimal and will be transferred to Petroci this year, so it’s effectively Kosmos’s Ghana assets.

Some points I would like to highlight:

1. Production in Q1 2026 has been robust, surpassing the upper range of guidance. Jubilee's gross oil output exceeded 70k, and TEN nearly reached 15k. Management now admits that previous guidance was quite conservative, leaving room for substantial upgrades in the future. As a point of reference, Kosmos' share price declined sharply in November after Tullow unexpectedly announced its guidance.

2. New wells are performing better than expected, and the decline from existing wells has decreased significantly. Management noted that three wells have been brought online since mid-last year, producing in line with pre-drill expectations. One was brought on stream in late March, with three more expected before the end of July, followed by a water injection well in September. Tullow highlighted that preliminary results for the next well (J76) suggest another positive outcome. Importantly, the decline rate from existing wells is improving due to enhanced voidage replacement from more reliable, consistent water injection. The adoption of dual-riser operations and riser-based gas lift in Jubilee was key to achieving this success. Everyone was very bearish on Jubilee not long ago, so it's encouraging to see real data indicating that this field remains in good shape.

3. Since the start of the war, West African crude trades at a material premium to Brent due to lower geopolitical risk compared to the Middle East. Jubilee priced a cargo at $130 per barrel, the highest realized price Tullow has ever achieved on a cargo. It's worth noting that hedges are priced against Dated Brent. Therefore, Tullow/Kosmos have 100% access to this premium, which peaked at around $12 but remains very significant and volatile nowadays.

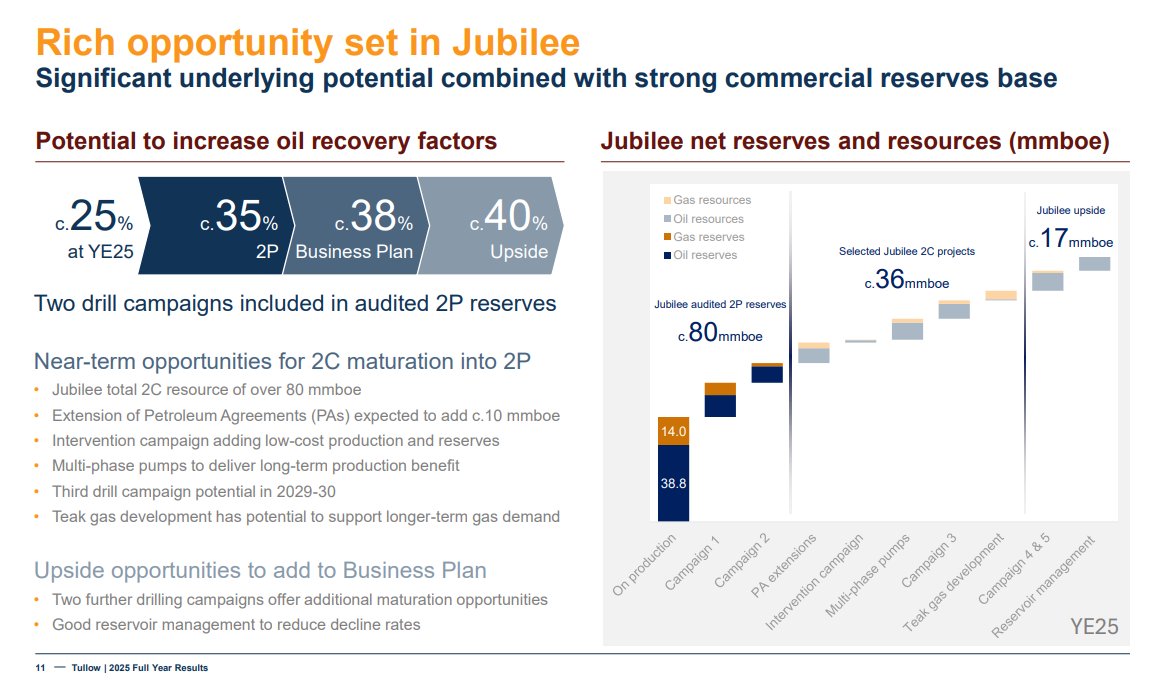

4. Tullow presented a compelling plan to significantly increase its 2P reserves by transferring value from the 2C category into 2P. New data from the 4D and OBN surveys reveal a strong opportunity for short-term, high-return drilling efforts that can sustain high production levels at Jubilee. Additionally, with the FPSO acquisition, they see potential to begin drilling in the TEN field and considerably boost performance. They confidently shared the NPV with Tullow, estimating Tullow's value at over $2 billion. Since Tullow owns nearly the same stake in Jubilee as Kosmos, this has significant implications for Kosmos.

In summary, Tullow made a compelling case to Kosmos yesterday. Additionally, our GTA tracking shows strong performance in Q1. I anticipate Kosmos will generate free cash flow this quarter for the first time since 2022, despite GTA prices lagging (with a 6-month Brent average) and Ghana being largely hedged. To see the impact of Brent prices on Kosmos's P&L, we will need to wait until Q2.

With the balance sheet significantly de-risked through divestments and a capital raise, I believe Kosmos's shares and bonds are still undervalued. Keep in mind that I am very selective in the oil sector now, as many companies are assuming a $80 long-term Brent price, but that’s not the case here.

As always, note that I hold substantial positions in both the stock and bonds, so my perspective may be biased or incorrect. Conduct your own due diligence!

English

Jorge retweetledi

Freeport cuts 2026 #copper sales estimates to 3.1 billion lbs vs January 2026 estimates of 3.4 billion lbs, primarily reflecting a projected delay in achieving full ramp-up of the Grasberg Block Cave underground mine pending modifications to ore loading infrastructure

English

@Edark94 People read too much on the daily small shit. For a person managing a pf with a 2-3 year timeframe (me), today's news are nothing. They can reverse on Tuesday. The US clearly doesn't accept multipolarity, and they will go down breaking things. Hence I keep my oil bets, GLTA.

English

Guess the doomers (me) lost yet again

Can't believe I fell for it again

Javier Blas@JavierBlas

BREAKING: Iran says passage "for all commercial vessels" via the Strait of Hormuz (and via the new Iranian shipping lanes) is now "completely open" after the ceasefire in Lebanon.

English

@creandocartera Y a 20 años+ que tal el resultado? No sería yo tan osado de decirle a uno de los pocos gestores que bate a los índices a l/p si hace bien o mal su trabajo.

Español

El gestor se aferra a una estrategia que no acaba de funcionar. ¿Es lo mejor para los partícipes?

¿Resultado? En 3 años: -12,44%

Global Allocation@GlobalAllocatio

1.- Informe Mensual Marzo 2026

Español

Jorge retweetledi

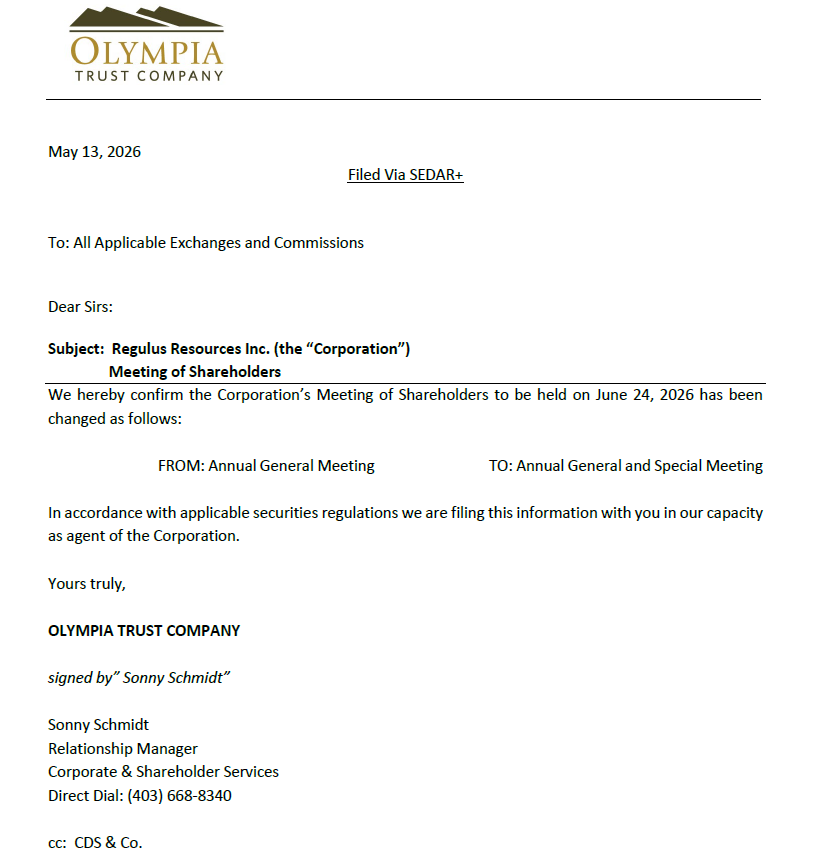

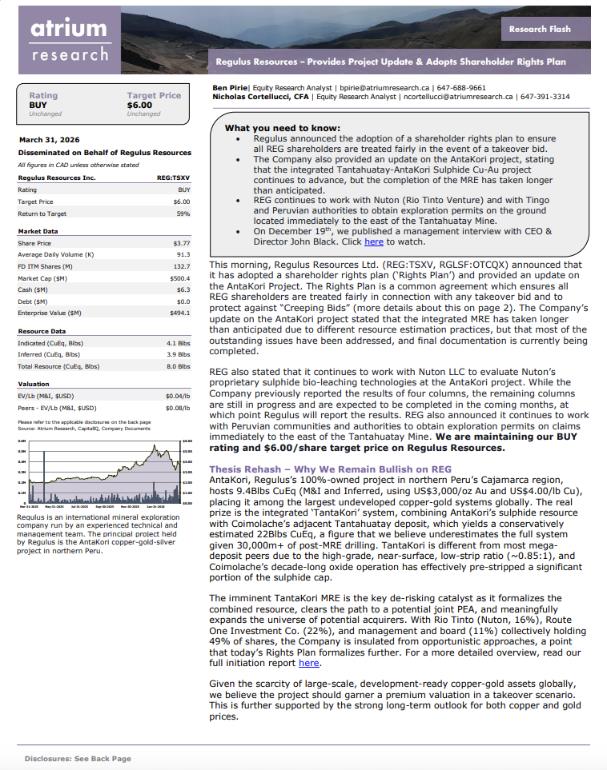

Our team has published a research flash on Regulus Resources Inc. Regulus announced the adoption of a shareholder rights plan ensuring all REG shareholders are fairly treated in the event of a take-over bid. $REG.V

🔍 Read the full report below

📰 Disclosure: Disseminated on Behalf of Regulus Resources Inc.

English

👀$REG.V @GlobeNewswire/regulus-adopts-shareholder-rights-plan-and-provides" target="_blank" rel="nofollow noopener">ceo.ca/@GlobeNewswire…

Norsk

Jorge retweetledi

Welcome, @IncRegulus!

AntaKori is shaping up to be one of the most compelling copper-gold-silver stories in South America, and we're proud to visualize it on our interactive 3D platform.

What our platform makes strikingly clear is the strategic positioning: several surrounding operators in the Cajamarca district are approaching the end of their mine life, creating a powerful convergence of demand, infrastructure, and M&A opportunity right on AntaKori's doorstep. These synergies aren't always obvious on paper, but mapped out spatially, the picture speaks for itself.

With district-scale ambition and a resource advancing toward production, Regulus is one to watch through 2026.

Learn more at → terrahutton.io

English

Jorge retweetledi

$KOS update:

Kosmos reports insider participation in the capital raise. In the end, management purchased 3.7 million shares, totaling $7 million, marking the largest insider buy ever.

investors.kosmosenergy.com/news-releases/…

This suggests a strong outlook for the company. Although the capital raise process wasn’t ideally executed—mainly because the discount was too high with many hedge funds involved—I believe the opportunistic flippers are out after the last two days' volume. Once the greenshoe option ends, the stock is likely to trade significantly higher than the day before the capital raise.

Operational performance has been very strong, and the balance sheet is now in a much healthier position, making the investment case more resilient. Additionally, it seems the war is far from over, and the Brent curve is beginning to reflect this. All 2026 maturities now trade above $80, and notably, even 2029 is above $70. The market should start pricing in at least $70 for long-term Brent, indicating that this company is highly free cash flow generative and will deleverage faster than many expect. However, consensus and agency ratings overlook these major developments — including operational improvements driven by GTA and Ghana updates, balance sheet strengthening from the capital raise and divestments, and significant free cash flow from the Brent price spike and operational cost reductions.

barchart.com/futures/quotes…

Finally, I want to address this news to prevent any potential confusion:

reuters.com/business/energ…

Senegal's Prime Minister is challenging the BP gas deal and seeking to renegotiate it. This does not negatively affect Kosmos; in fact, if Senegal succeeds, it would be a significant win for Kosmos. The core issue concerns the GTA pricing, where the partners produce the gas and sell it to BP's trading entity at 9.5% of Brent. Currently, this contract might be close to 13% if linked to Brent or TTF, which would make a notable difference. At present, BP's trading division profits substantially by buying cheap gas—linked to a low Brent ratio—and selling it in Europe at high margins. Kosmos attempted to switch to TTF pricing or sell to other buyers, but in late 2024, the International Chamber of Commerce (ICC) in Paris ruled in BP's favor. This ruling prevents Kosmos from selling cargoes to third parties until 2033, maintaining the original sales agreement. It is important to note that this project spans over 20/30 years, and by 2033, Kosmos may choose to renew under the same terms or seek better ones.

Therefore, this news is mostly neutral or slightly positive for Kosmos.

English

Jorge retweetledi

THE UNITED STATES, JAPAN AND THE EUROPEAN UNION ARE ADVANCING TALKS ON A CRITICAL MINERALS TRADE AGREEMENT THAT MAY INCLUDE A PRICE FLOOR AND TARIFFS TO COUNTER MARKET DISTORTIONS FROM CHINA.

English

Jorge retweetledi

$KOS Kosmos raised $182 million yesterday at a price of $1.90, which is a 21% discount to the closing price. The offering has generated strong demand, and the management team participated by purchasing approximately 3 million shares (the first insider purchase in a long, long time). For full transparency, I also participated in this capital raise.

I believe this offering was forced by the RBL banks to extend the 1.35bn facility. During the earnings call, the company stated they plan to seek an extension over the summer, ahead of the September 2026 deadline, when the liquidity test could trigger early repayment.

I don’t believe this raise was necessary, but banks forced them to act. Banks that have been very supportive of Kosmos—extending the RBL facility and granting numerous waivers in recent months—are now trying to reduce risks through this move. I wonder whether they are facing issues with many other companies, given reports of turbulence in the US private credit market.

Some people argue that $182m is insignificant compared to the around $3bn net debt reported in Q4, but they overlook key details. As of December 31, the RBL total was $1.35bn, with $1.20bn drawn and $150m undrawn. In January, they issued a $350m Nordic bond and repaid $100m of the RBL. Then, in February, they announced the sale of assets in Equatorial Guinea to Panoro, expected to close by mid-year, which should lead to an additional $200m repayment, as those assets were collateral for the facility. As a result, the existing bank debt is now approximately $900m, making this capital raise quite significant to this number. It’s fair to say that banks lost EG collateral, and GTA and GoA are now secured against different loans, leaving them with little safety margin outside Ghana. Nevertheless, Jubilee's performance remains robust, and its asset value should exceed $1 billion, even if oil prices stay low.

This is why companies often prefer bond financing to bank loans, even though bonds are generally more expensive. Bondholders were not asking the company to raise funds today, unlike banks, which often do. This has occurred several times; for instance, Golar raised $100 million in December 2020 (∼10% dilution) after banks pressured it, even though the company was already under control. Be aware that Golar's stock price tripled over the next two years, clearly indicating that the capital raise was unnecessary. Similarly, Kosmos has achieved control over its operations through GTA and Ghana, which are performing above expectations. The company also hedged effectively for the second half of 2026 and 2027, securing high free cash flow that will significantly reduce its leverage.

Although I believe the raise was unnecessary, the dilution isn't significant and doesn’t harm the investment case. Even with the greenshoe option (standard in all brokered equity issuances), the dilution remains minor and it only slightly lowers the long-term target price. However, it helps mitigate downside risk if oil prices fall back to $60 or below. This move reduces the company's risk and could attract institutional investors who previously stayed away due to the weak balance sheet. Starting with nearly $3 billion in net debt, I believe that through the EG sale, this equity raise, and free cash flow, they could reduce net debt by almost one-third by the end of the year — potentially driving the stock's valuation higher rather than trading like a distressed company.

Understanding that they couldn't control the equity issuance movement was not something they could control (better now than when it was trading at very depressed levels), perhaps my only surprise is the large discount. I would have expected a smaller discount compared to the last price, given the current outlook. They could have put in more effort to show that the company's 2025 numbers are significantly different from today's numbers, making it more convincing to investors involved in this capital raise.

Overall, as in other cases, I think the stock might take time to absorb this equity raise, particularly with the greenshoe active, but then, it will definitely trade higher due to an improved balance sheet and better FCF generation outlook. All else equal, I'd be surprised if the stock trades below the price issuance level.

English

Jorge retweetledi

Centauri will offer a portfolio comprised of several high-potential projects, an aligned management team with experience in the region and a proven track record, and an unbeatable macroeconomic and national environment. Happy to be on this team, long $REG.V and $ALDE.V too

Aldebaran Resources Inc@AldebaranInc

Press release: Aldebaran and Centauri Announce Significant Increase in Mineral Resources for the Rio Grande Gold-Copper Project in Salta, Argentina Read the full release: aldebaranresources.com/aldebaran-and-… $ALDE.V $ADBRF #Centauri #gold #copper #silver ⛏️🇦🇷📈

English