Sabitlenmiş Tweet

Isar

268 posts

English

English

@soamjena @robprogressive I live in the UK and in Dubai on rotation. And the UK is far more expensive. Also education in the uk isn’t free (universities).

English

You probably would be getting free health care and education in UK. But once you move to Dubai, you are going to lose a shit ton of money on both of those!

Basically, if you are thinking from a tax point of view, I don't think you are going to save anything.

You will literally be shelling out a lot of money on those stuff alone. Dubai is extremely expensive to live.

English

Worth sharing some experiments I’m doing with Ai done couple weeks ago. I think with correct prompts long term targets are becoming more and more feasible.

It’s still tricky to get the short term targets spot on but defo the longer term targets at becoming more and more accurate.

For those curious analysis was done couple weeks ago at gold fluctuating around 4200.

English

@andre22x_charts Hey buddy thank you ! And for sure il try to share more on that soon

English

@isarchaudry This looks very interesting bro, when you say long-term targets are improving, what’s the valuation anchor? macro inputs, flow data, or price only context?

I feel like without defined fair value bands, AI forecasts can just become narratives, curious how you’re handling that?

English

Great start to 2026. Bought a second company out and merged into my own ecosystem. Bought one out back in December.

I’m seeing my attention divert more and more into private equity now. I’m on the road to a €100m. But I see it being more feasible via PE. Will explain more on the next YT video.

English

This is the big difference between course selling final boss and actually someone who earned his money the hard way and does financial responsible things

I've made good money over 18 months in the markets and only thing I did purchase thats not an asset is my car, full cash 50k, but ofcourse I didnt go all in trying to flex I cant afford, I stayed in my own lane and bought what I can afford, also thanks to @isarchaudry for always guiding me with financial decisions

alot of these course sellers / influencers go broke trying to look rich, you should go rich trying to look broke at this point.

Jason Applebaum@Jason______A

I really didn’t want to repost this guy because he didn’t even “buy” from Carrio… but he came on here chest-puffing about how “smart” his deal was. Meanwhile he never once looked at his amortization schedule, prob didn’t know what that was until I mentioned it. He thought a “10% rate” meant 10% of his payment was interest. So with a $5,300 /mo payment, he assumed only ~$530 was interest. Reality check: Over $2,500 of that payment is interest. Every. Single. Month. He thought he was paying down 4.7k equity and paying $530 in interest. Nope. It’s basically 50/50 $2,600+ interest, $2,600+ principal. And that’s before the parts he conveniently didn’t mention: 1. There’s a balloon payment at the end. He won’t keep the car that long, but the payment still exists. 2. “First and last payment.” That “last payment” is literally $5,300 set on fire if you don’t run the full term. 3. To exit the lease early? Another $5,300 torched. Those two $5,300 payments alone push his effective rate way above the “10%” he thinks he’s paying. Moral of the story: Don’t flex financing terms if you’ve never opened the amortization table. Twitter will do the math for you. PS: Yes he saved $300k cash and that $300k cash can be used to make more than the interest he is paying. I’m not saying this is an awful deal. I’m saying he didn’t fully understand the deal and went into it with the wrong numbers.

English

@flexxtrades I know you made serious money ! And always open to invest the correct way. Props to you ! Always there for you whenever you need me !

English

Just had this thought while I was waiting for my jet, charting a jet is slowly becoming a norm. It’s not how it used to be, Inaccessible for the normal man. It used be something only for the elites.

Now anyone can do it, if you do okay for yourself. I think charting a yacht is still only for the elites. I’m talking about 20m+ yachts in European sea. Not those Dubai small yachts for 2-3 hours. Not that anything is wrong with that.

English

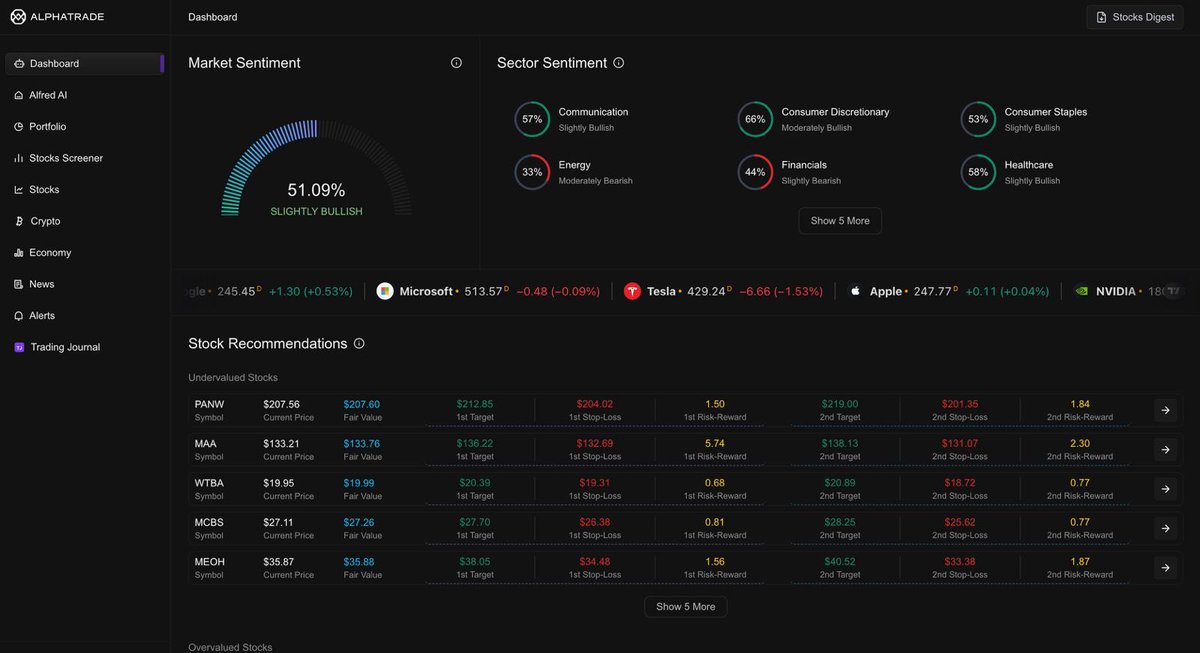

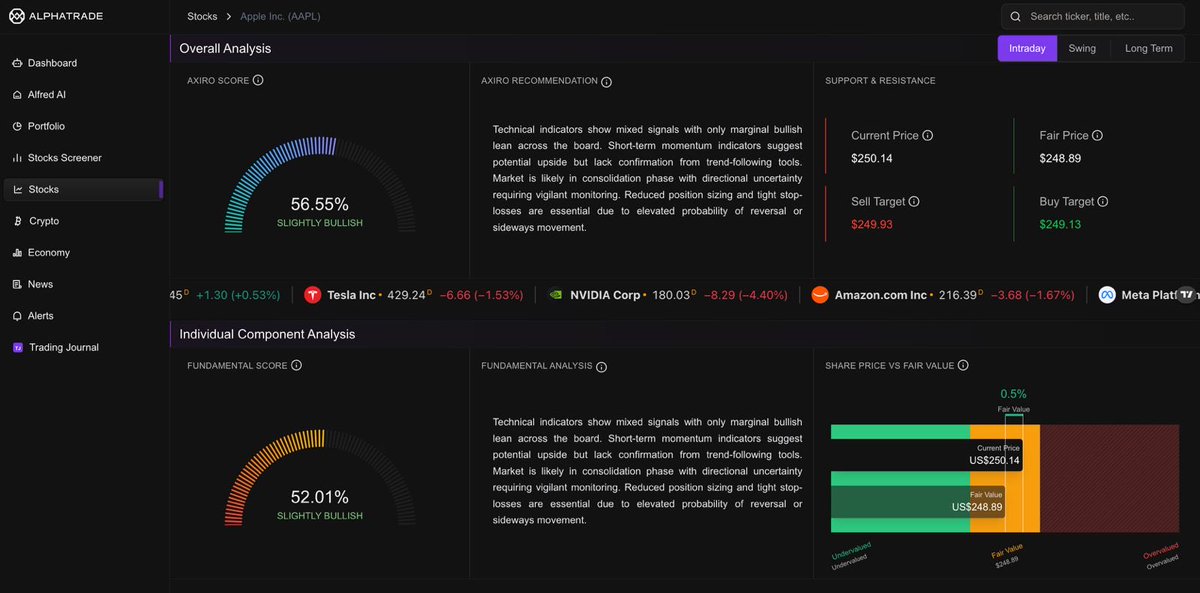

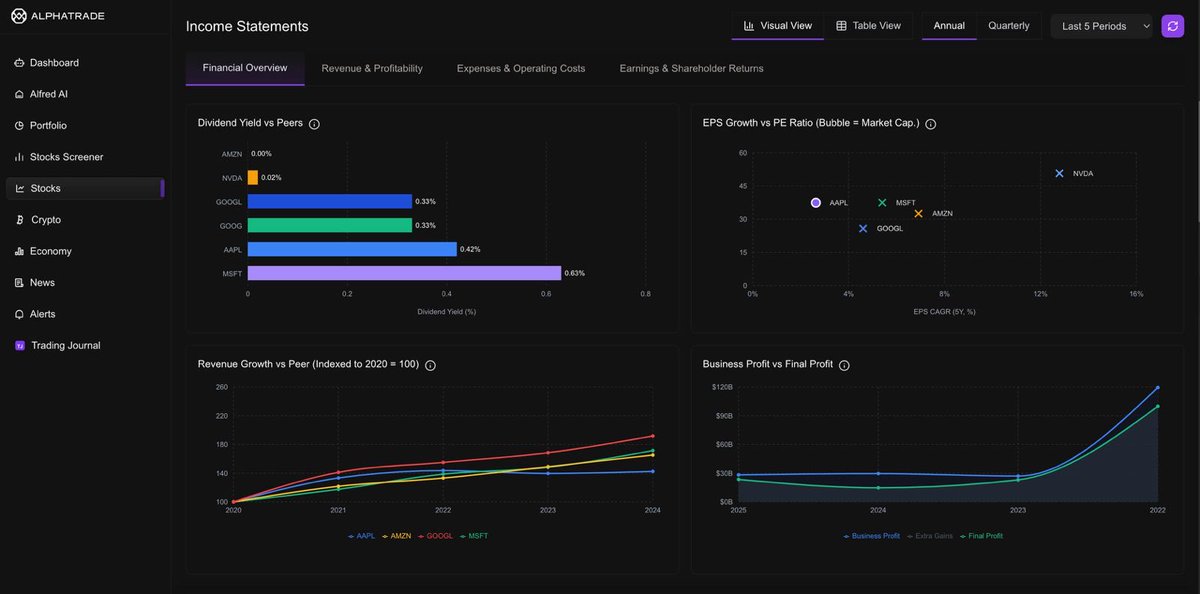

Our biggest update so far is live.

Faster decisions. Smarter signals. Cleaner design.

Here’s what’s new:

Axiro Score

- One number that tells you if an asset’s bullish, bearish, or neutral, built from fundamentals, sentiment, price action, macro data, and live news.

Recommendation Engine

- Your dashboard now delivers ideas that fit you, your portfolio, your risk profile, your trading style.

Rebuilt Stocks Page

- Fully AI-native, stripped of noise, built for clarity.

- No endless data tables, just insights that help you act.

We move fast, but not recklessly.

We're still in V1, but every update gets us closer to what we’re building: the smartest trading assistant in the market that keeps getting better and better over time.

It’s live now @AlphaTradeAi

English