Sabitlenmiş Tweet

IVAYLO

78 posts

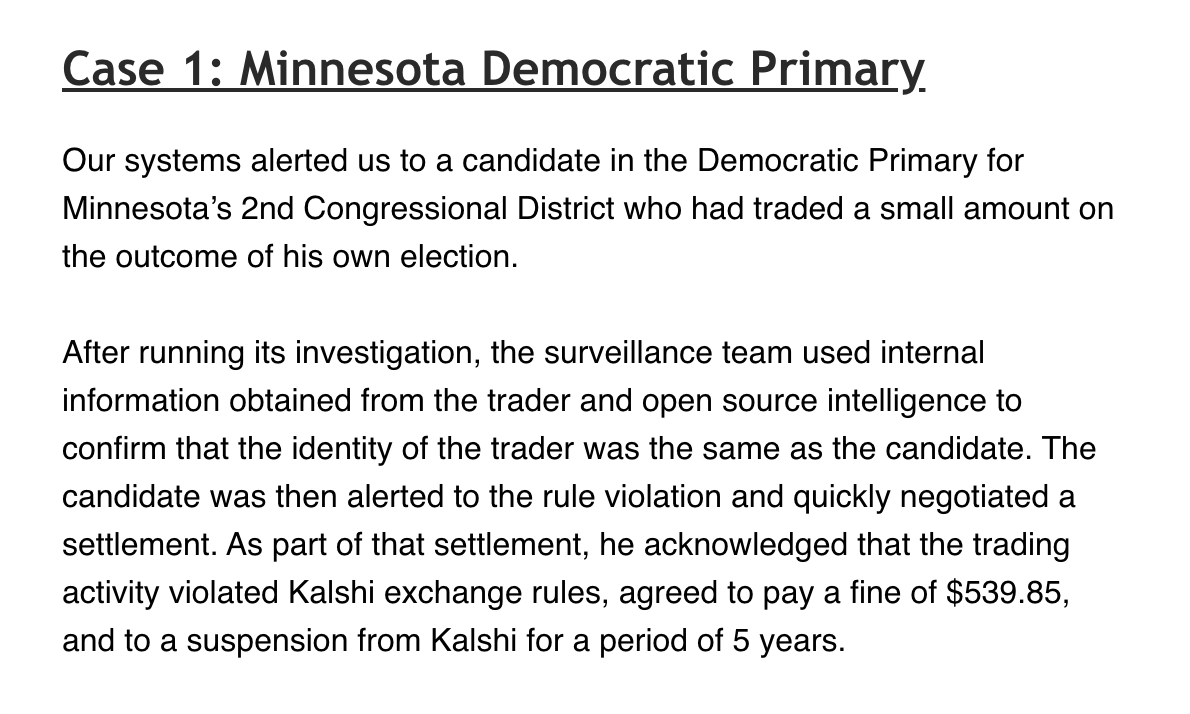

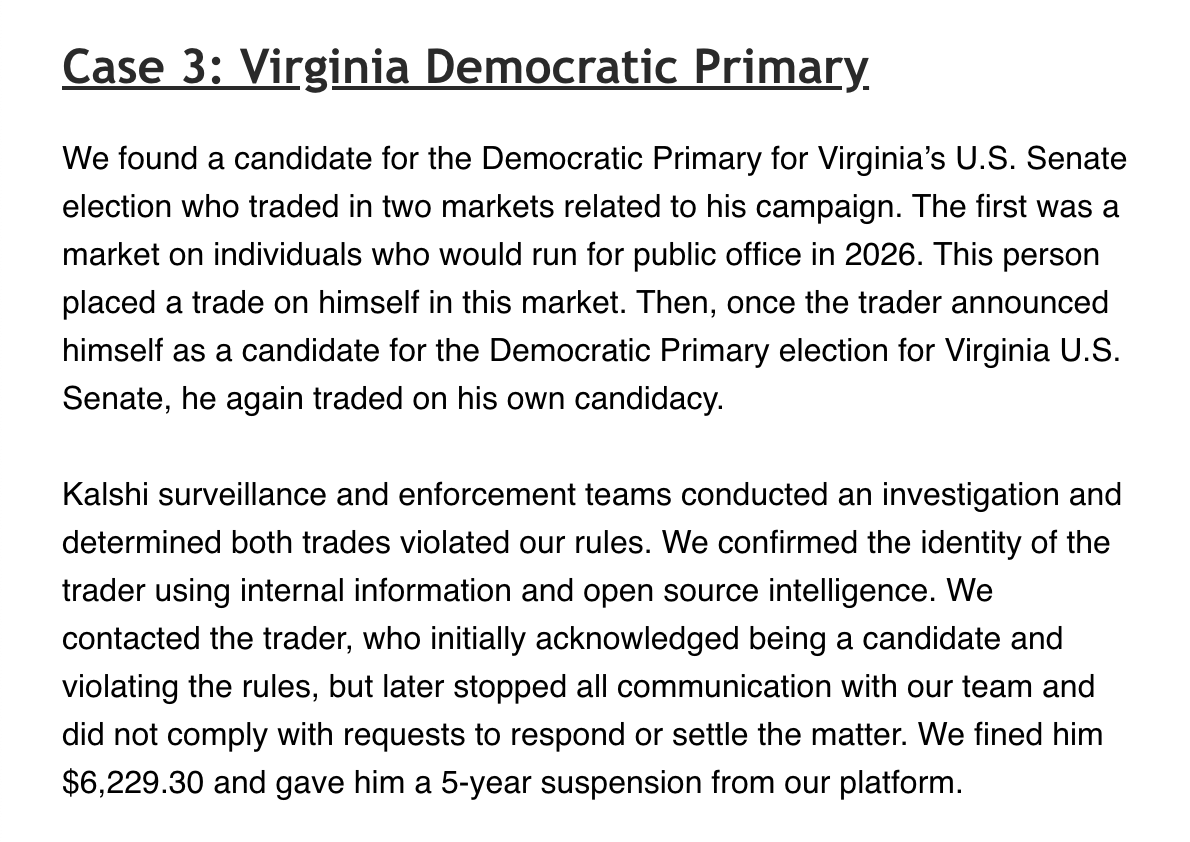

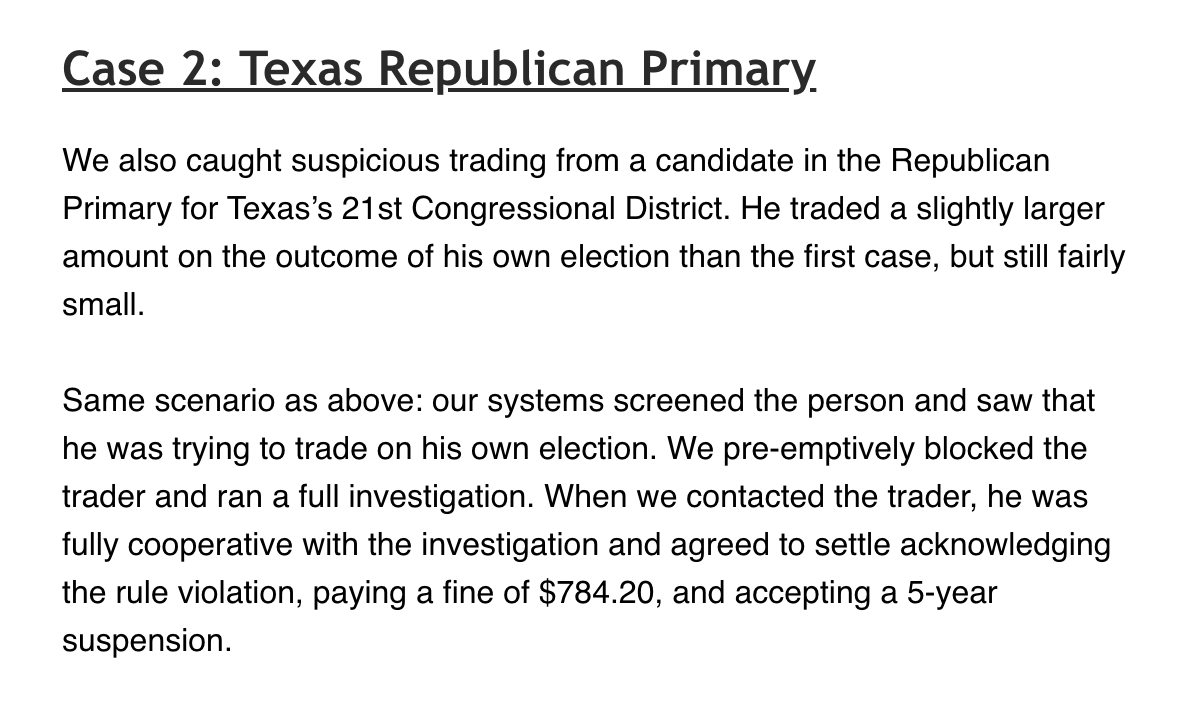

Kalshi says it caught 3 political candidates trading on their elections, including:

- MN-2 Dem primary candidate, fined $539.85

- TX-21 GOP primary candidate, fined $784.20

- VA-SEN Dem primary candidate, fined $6,229.30

They were each suspended from Kalshi for 5 years.

English

IVAYLO retweetledi

🚨 CRITICAL: Active supply chain attack on axios -- one of npm's most depended-on packages.

The latest axios@1.14.1 now pulls in plain-crypto-js@4.2.1, a package that did not exist before today. This is a live compromise.

This is textbook supply chain installer malware. axios has 100M+ weekly downloads. Every npm install pulling the latest version is potentially compromised right now.

Socket AI analysis confirms this is malware. plain-crypto-js is an obfuscated dropper/loader that:

• Deobfuscates embedded payloads and operational strings at runtime

• Dynamically loads fs, os, and execSync to evade static analysis

• Executes decoded shell commands

• Stages and copies payload files into OS temp and Windows ProgramData directories

• Deletes and renames artifacts post-execution to destroy forensic evidence

If you use axios, pin your version immediately and audit your lockfiles. Do not upgrade.

English

In this new world, auditors who have had a lot of experience identifying issues and their root causes would have a huge leg up. Not to mention all the experience from chatting with AI agents on a daily basis.

vitrupo@vitrupo

Eric Schmidt says the 10x advantage is no longer execution. It is defining what counts as success. A programmer writes a spec and an evaluation function, runs it at 7pm, and wakes up to what was invented overnight. The advantage now belongs to whoever can specify the problem precisely. The rest will be automated.

English

IVAYLO retweetledi

Resolv was audited 18 times. The exploited contract was reviewed. The vulnerability was never flagged.

In December 2024, auditors reviewed this exact contract and found 5 issues, including a High severity bug in the fee function. One finding was literally called "Missing upper limit validation." But it was about price bounds in a different contract. The function that lets a single key mint unlimited tokens with no ceiling? Not mentioned.

That's how audits work: a function restricted to a trusted role is "privileged, out of scope." Auditors verify code correctness, not whether trusting one key with unlimited power is a good idea.

18 audits couldn't prevent this. The flaw wasn't in the code - it was in the architecture.

English

@0xAnteater circumventing kyc is one of the easiest things for bad actors.

pretending it prevents crime is laughable

English

@StaniKulechov won’t private credit see even more pressure now with the war in the ME?

gulf states are major players there and by how things are going they’ll probably be needing their cash back

English

Private credit is in a strange place today.

The economy is tied to the cost of money. Low interest rates mean cheap borrowing, which in theory should lead to higher utilization of credit facilities. Conversely, high interest rates mean less affordable borrowing and, in theory, reduced demand for credit.

We've been living through a high-interest-rate environment since the Federal Reserve began its aggressive tightening cycle in March 2022, raising rates from near zero to over 5% by mid-2023, the fastest hiking cycle in four decades. Rates have remained elevated through early 2026, with only modest cuts. For many consumers and businesses that initiated borrowing during the low- or mid-rate era, and whose obligations remain outstanding, this translates into a significantly higher cost of capital, a burden that compounds over time.

This all sounds normal. Finance is part of almost every phase of a company's lifecycle, from growth to maturity. The problem arises when the cost of capital stays elevated for too long, creating unmanageable expenses for borrowers.

Businesses typically borrow from financial institutions like banks, or from asset managers in the form of private credit.

How do private credit funds work?

Private credit funds are typically either closed-end or semi-liquid vehicles managed by asset managers. This structure makes sense: the funds need to deploy capital into lending opportunities to generate returns. Investors in private credit range from pension funds, insurance companies, and family offices to, increasingly, retail investors.

Closed-end funds don't allow redemptions until maturity, usually 7 to 10 years. Semi-liquid funds offer quarterly redemption windows with limits. BDCs (Business Development Companies), which are publicly traded, provide liquidity via daily trading on exchanges.

In essence, private credit funds function as private banks: they lend capital to businesses and collect interest.

What does private credit fund?

Typically, private credit finances leveraged buyouts for private equity, middle-market corporate loans for companies that lack access to public bond markets, certain asset-backed lending (such as aircraft, shipping, and consumer loans), and real estate credit.

Private credit funds generally fill the funding gap that banks have vacated. This shift has been driven primarily by post-2008 regulation, particularly Basel III, which pushed banks out of riskier corporate lending. Today, private credit finances an estimated 80 to 90% of leveraged buyouts in the U.S. middle market.

Who are the players?

Apollo ~$460B AUM

Blackstone ~$330B AUM

Ares ~$280B AUM

KKR ~$220B AUM

Carlyle ~$190B AUM

Blue Owl ~$170B AUM

What's going on?

Recently, distress has emerged across private credit. The persistent cost of capital driven by high interest rates remains a reality, and AI is reshaping perceptions of many software companies that private credit has funded, creating uncertainty about these borrowers' futures.

The market has already begun repricing private credit:

VanEck BDC Income ETF: ~15% decline over the past year

Blue Owl Capital: ~50% decline over the past year, with ~30% of that during 2026

Apollo, Blackstone, Ares, KKR: shares down ~20% on private credit concerns

The average BDC now trades at roughly a 20% discount to NAV while offering 10 to 11% yields, signaling that loan portfolios may be overvalued, defaults could rise, or liquidity risk is building. What makes this even more concerning is that historically, these funds traded at a premium.

Some funds' monitored loan default metrics have risen to as high as 9%. Blackstone's flagship private credit fund, BCRED, is a notable example.

BCRED recently limited its redemptions. The fund manages roughly $82B, and during Q1 2026, redemption requests reached $3.7B, approximately 8% of NAV. Blackstone injected $400M of its own capital to support liquidity. Technically, the fund was not gated, but it came very close.

Meanwhile, BlackRock's HPS Corporate Lending Fund (HLEND), a $26B fund, received $1.2B in redemption requests, reaching the point where gating was necessary. Roughly $580M in requests could not be honored.

Blue Owl's retail private credit vehicle experienced $2.9B in redemptions during Q4 2025, with redemption requests reaching 15% of NAV, largely driven by exposure to software lending.

Can the market handle a private credit fund default?

While total redemptions have been around $7B+ (5 to 10% of NAV) and public alternative managers are down 20 to 30%, the overall private credit market is still $1.8 to 2T in size. Even the largest funds top out at $20 to 80B, compared to the global bond market at $130T or banking assets at $180T. A single fund default would most likely not collapse the broader market or trigger the kind of contagion that amplifies crises. Large funds also hold diversified portfolios of hundreds of loans, and the semi-liquid or closed-end structure naturally forces investor lock-up, acting as a buffer against bank-run dynamics.

I've mapped out three scenarios of increasing severity:

Scenario A: One large fund defaults (~$50B)Investors lose capital, some companies lose financing, and credit spreads widen. The system likely absorbs the shock.

Scenario B: Several funds fail simultaneouslyCredit markets freeze, leveraged companies cannot refinance, and defaults cascade. This could trigger a credit-cycle downturn.

Scenario C: Private credit + leveraged loans collapseA broader corporate credit crisis unfolds: private equity deals fail and banks become exposed. This would be genuinely systemic.

Fortunately, private credit funds remain relatively small in the broader picture and are unlikely on their own to pose systemic risk. However, the most worrisome scenario is one where loss of confidence begins in private credit markets, particularly around lending to businesses vulnerable to AI disruption, and then bleeds into public bond markets. This contagion path is plausible because the larger corporates in bond markets are arguably more exposed to automation and AI disruption than the leaner, high-growth businesses that private credit typically funds.

How does this affect RWAs and DeFi?

The most immediate impact of private credit distress falls on capital allocators. Many private credit funds have been distributed to retail investors via publicly traded BDCs, private credit ETFs, or semi-liquid funds like Blackstone's BCRED, Apollo's Debt Solutions BDC, and BlackRock's HPS Corporate Lending Fund.

These funds share common characteristics: quarterly (or monthly) redemption windows, redemption limits typically capped at 5% of NAV per quarter, and target returns of 8 to 11%. Recently, some funds have also begun gating redemptions.

From a DeFi capital allocator's perspective, the biggest risk I see is structural: private credit is packaged in DeFi in ways that many retail-oriented users don't fully understand before committing capital. We've seen countless examples of DeFi users eagerly supplying funds into high-yielding RWA strategies, only to discover later that the underlying exposure carries significant duration risk.

I believe RWAs represent the biggest opportunity for DeFi in the near term. However, my greatest fear is that institutional opportunists could view DeFi as a channel to offload illiquid and distressed products that Wall Street has already soured on, effectively using DeFi participants as exit liquidity. This risk is amplified by the fact that assessing RWA allocation opportunities is inherently harder: they don't carry the same transparency or onchain verifiability that native DeFi opportunities provide.

That said, private credit done well onchain offers something traditional finance fundamentally cannot: smart contract-enforced guarantees. Redemption windows, withdrawal limits, collateral ratios, and distribution rules can be encoded immutably, meaning fund managers cannot arbitrarily change the terms after capital has been committed. In traditional private credit, investors discovered the hard way with BCRED and HLEND that redemption policies can be tightened or gated at the discretion of the manager when conditions deteriorate. Onchain, those rules are transparent from day one and enforced by code, not by a fund administrator under pressure. This is precisely where RWAs and DeFi can outperform the traditional model for this asset category.

For RWAs to succeed in DeFi, and for DeFi to scale meaningfully through real-world assets, the industry needs deliberate and careful structuring of opportunities that bridge TradFi and onchain markets. That means robust transparency standards, proper risk disclosure, independent verification of underlying collateral, and governance frameworks that protect onchain participants from asymmetric information disadvantages. Without these safeguards, the convergence of TradFi and DeFi risks becoming extractive rather than additive.

DeFi should not become Wall Street's exit liquidity.

English

@ZachhC @AlanRMacLeod @Polymarket didn’t similar incentives exist even before Polymarket? you could still profit from such decisions, just through different financial instruments

English

@AlanRMacLeod Yea, honestly @Polymarket please shutdown nuclear attack related markets. Not worth having such incentives even exist...

English

At this poin, Polymarket is literally a threat to the survival of the planet.

It needs to be shut down.

David Sirota@davidsirota

Polymarket has created a market that would monetize a nuclear attack amid increasing concerns that bets are happening among government insiders who can make military decisions.

English

@izebel_eth yes that’s the point but all these retards have no idea what prediction markets are or how they work

insiders are the most informed thus influence markets towards the most accurate outcomes. if there are people willingly giving up their money for the cause let them

English

insider trading is illegal because you defraud investors, and investors should be protected

who is mr beasts editor defrauding by trading on kalshi? retards who bet on kalshi? why do we care about protecting them? isnt the point to financially incentivize accurate information?

More Perfect Union@MorePerfectUS

The first insider trader punished by Kalshi is an editor who works for MrBeast. The editor has been suspended from the platform and reported to federal regulators for insider trading. He bet about $4,000 on markets related to MrBeast.

English

@JoshC0301 completely agree. what makes it even worse is that it is possible to do age verification without uploading all personal info with zk tech but the fact they arent doing that should make their goal clear

English

Once again, I am reminding people to stop calling it "age verification" and instead call it **Identity Verification** because it's not possible to verify everyone's age without providing ID information that will probably be hacked and leaked soon after

alpha@omarsbigsister

And this is why age verification laws passing anywhere is a danger for everyone everywhere

English

imo what makes this time different is the domain, where past revolutions automated muscle by building tools for us to direct and manage, this time the focus is on automating reasoning. if successful there’s really no economic reason for the majority of humans to be part of the labor force with white collar going first and eventually blue collar work too

also I’m not really sure where exactly you stand, if you think even if AI gets good enough people will still find something to do or if you think AI will never get good enough in the first place and remain in the current tool-like state

just to clarify my position: right now it’s a great lever for competent people to use as a productivity multiplier but will still be a while before actual structural, society-wide displacement

English

@ivxylo I dont see it at all. Ive used LLMs enough to know they arent even close to being a generic replacement for human cognition.

Exactly what leads you to believe this time is different?

English

people have been saying this for 70+ years since the initial success of the "electric brain" and "thinking machines".

the feeling and general mood among the tech bubble has appeared a number of times, and each time everyone thinks "this time is different".

it never is.

it never has any rigorous justification. people just want to believe it.

the story is really several thousands years old in its religious and mythical variations. the "scientific/industrial" version is about 200 years old, and the computational version about 100 years old.

𝕆𝕝𝕚𝕧𝕖𝕣 𝔹𝕖𝕚𝕘𝕖@oliverbeige

Norbert Wiener, merchant of doom.

English

I can't even express my feelings rn...

3rd place on Mento's contest, life is good.

Congrats to @vinicaboy, he once again proved that he is one of the best in our space!

@0xSimao I guess the 5 figs challenge goal isn't that far now, is it?

English

There should perhaps be a psychological study on the people that pick out random words from your tweets and make coins from them like quick guys he said toothpaste quick raid raid raid, but then they get annoyed and say how come you aren’t supporting toothpaste token when you previously used the word toothpaste in a sentence

English

IVAYLO retweetledi

@0xapple_ @Cryptor256 @flyingtulip_ @aave I think it’s exactly the AI reports that are mostly the ones confusing design with bugs.

Usually they miss the higher context

English

@Cryptor256 @flyingtulip_ True, but @aave V4 contest had ~2× the nSLOC and 4× the rewards, yet still <1,000 submissions.

I participated in FlyingTulip and reviewed the findings. From what I saw, a large share of the invalid reports came from people confusing design choices with bugs, rather than AI spam.

English

Days 24-30:

Spent the week focused on Flying Tulip. Had some submissions that were immediately invalidated after a change to the conest rules but still have a few I'm hopeful of.

Will probably spend some time today catching up on the Mentorship Series videos that just released

@0xSimao Contest Academy

English