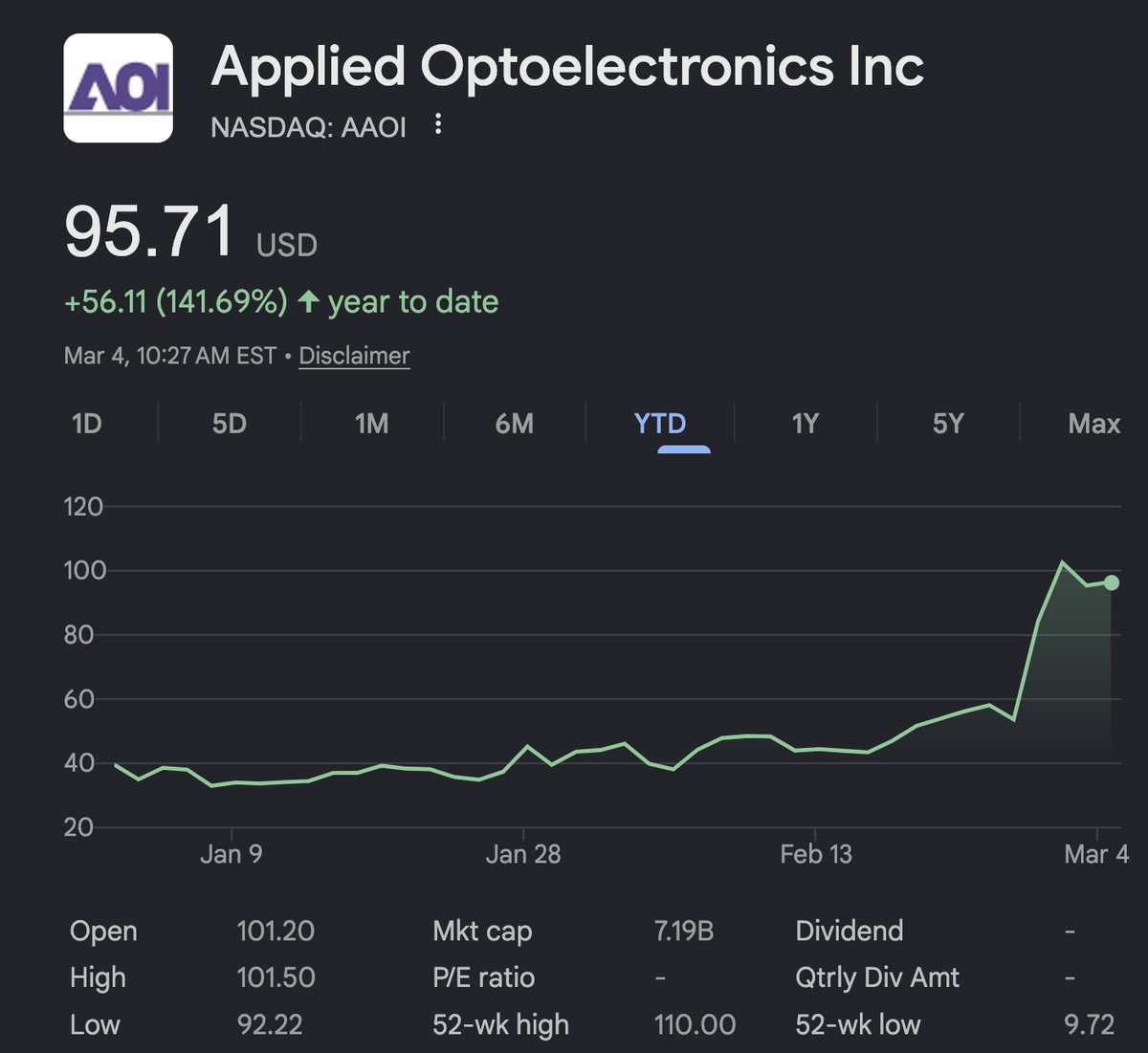

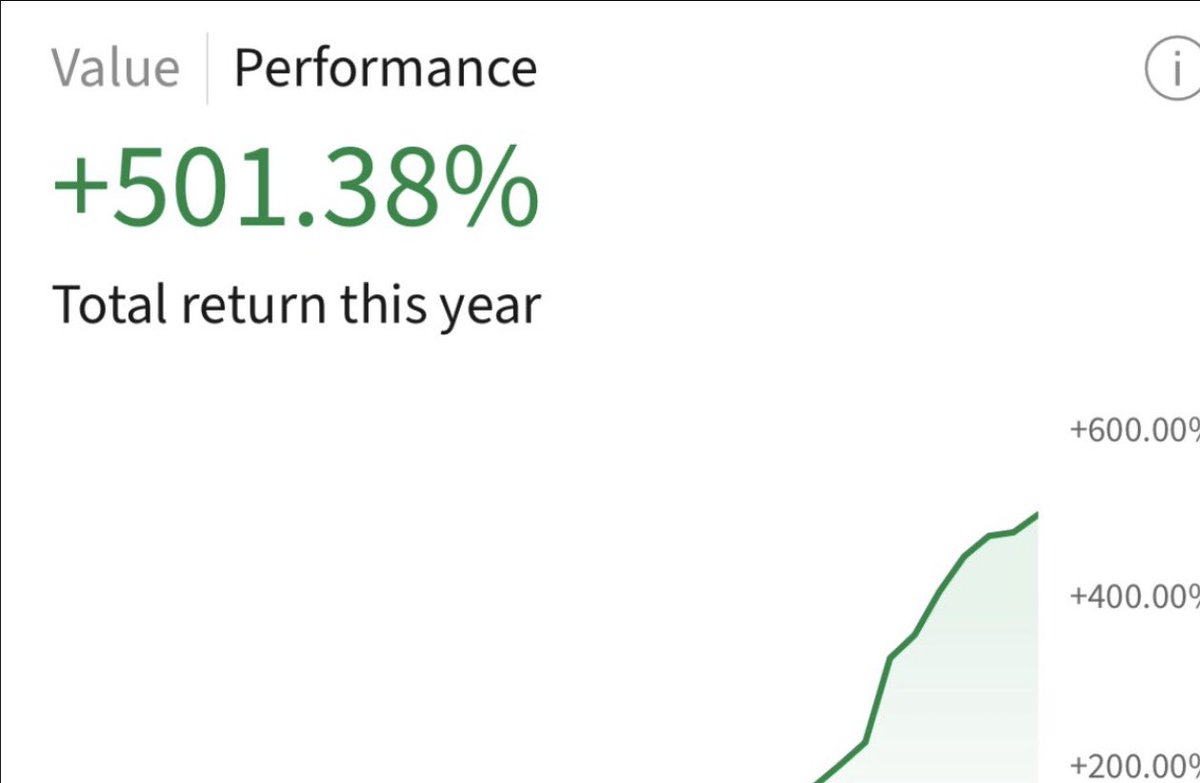

@MikeFritzell Have noticed the same thing. @skhetpal what are you doing to us?

English

JackCap

1.4K posts

@jackefeller

Trying to learn from past mistakes and keep on learning

After the interview, Iliana Bouzali puts Stan Druckenmiller in the hot seat with a multiple-choice game—covering macro, asset bubbles, and the risks he’s watching.

Tom Gayner on how he thinks about $MKL public equity portfolio We also discuss Markel Ventures, reinsurance, and capital structure Interview available for free on all podcast players and our platform