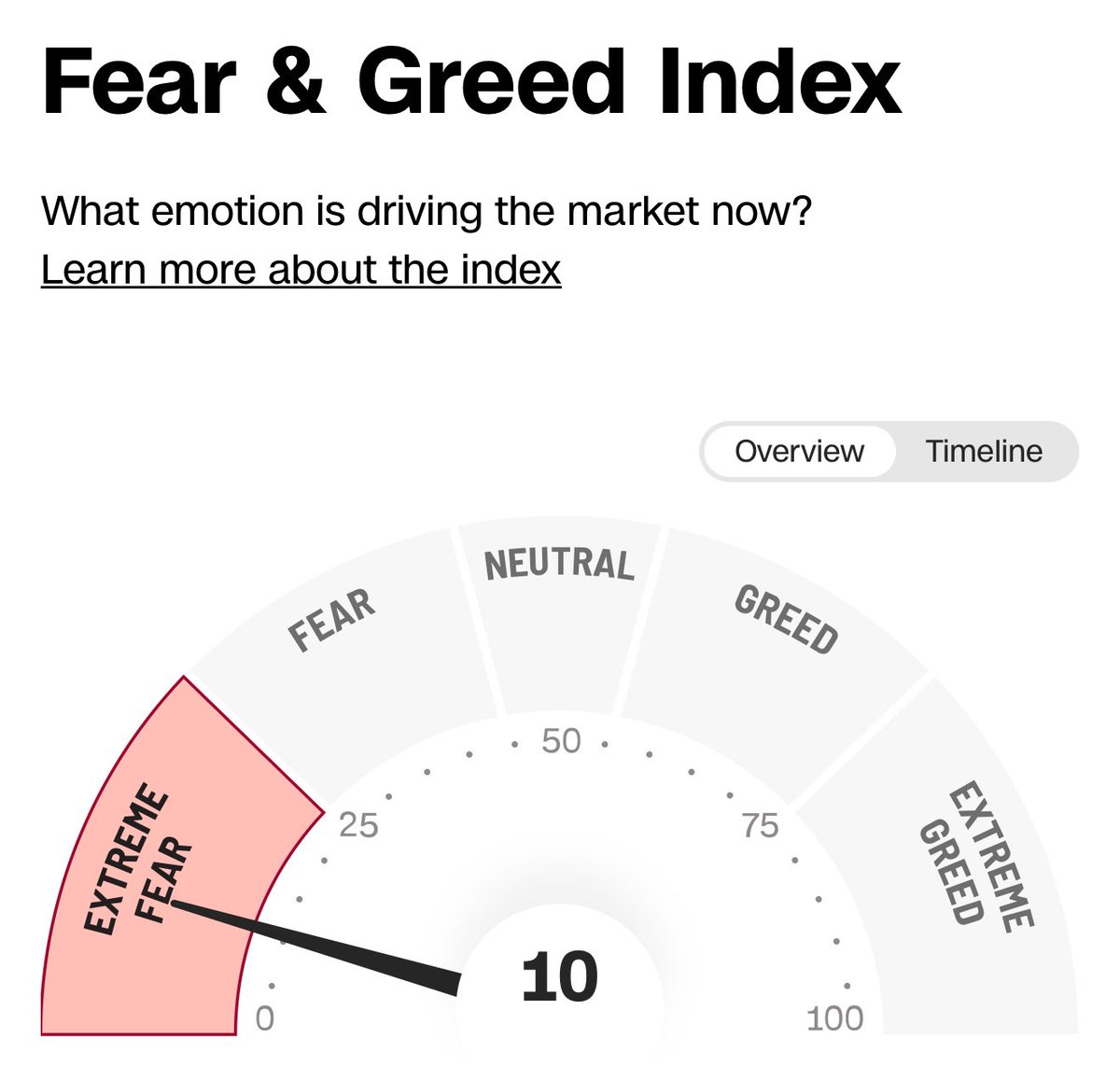

Sabitlenmiş Tweet

Jay aka @JADED_BULL aspiring CPA

12.3K posts

BREAKINIG: E*Trade is in lead to handle SpaceX IPO sales for small retail investors, per sources. SpaceX considering cutting Robinhood $HOOD and SoFi $SOFI out of IPO as brokerages negotiate for a piece.

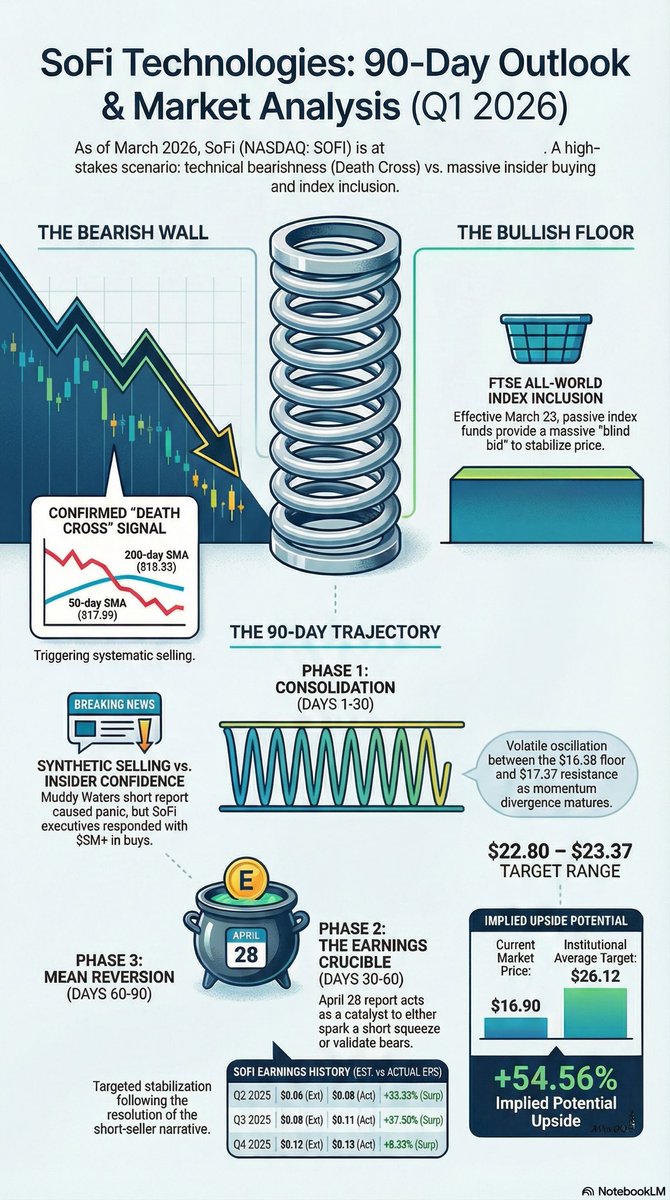

$AFRM private credit FUD $KLAR The narrative suggesting that Affirm Holdings is facing an existential funding crisis due to the ongoing volatility in the private credit markets represents a profound mispricing of risk by the public equity markets. The gating of redemption requests by interval funds such as Stone Ridge's LENDX, Cliffwater, and BlackRock's HPS highlights a structural failure in the architecture of semi-liquid asset management products, rather than a systemic collapse in the creditworthiness of the American consumer. The public equity market's reaction to the LENDX markdown failed to account for the mechanical realities of interval fund accounting, mistakenly conflating a fund's liquidity-driven mark-to-market distress with the actual fundamental default rates of Affirm's consumer loan book. Affirm’s fundamental architecture is deliberately constructed to isolate the firm from precisely these types of capital market dislocations. The company's execution in the first quarter of 2026 provides empirical, irrefutable proof of this resilience. By upizing its Asset-Backed Securitizations to $750 million at yields below 4.6% in a wildly oversubscribed offering, expanding its forward flow agreements with multi-billion-dollar life insurance conglomerates like New York Life, and simultaneously delivering 36% GMV growth with 30% adjusted operating margins, Affirm has comprehensively demonstrated that institutional demand for its originated assets remains intensely robust. While the macroeconomic environment—defined by sticky 2.7% PCE inflation, geopolitical instability, and $110 oil—warrants vigilant monitoring, Affirm's short-duration assets allow for real-time underwriting recalibrations that insulate its balance sheet from sudden economic shocks. The ability to simply turn off break-even origination cohorts provides a shock absorber that legacy credit card issuers lack. Furthermore, the strategic pursuit of a Nevada industrial bank charter, despite fierce opposition from legacy banking consortiums fearing competitive displacement, illustrates a proactive management team seeking to permanently secure a low-cost, insulated deposit funding base. Ultimately, the early 2026 intersection of private credit fears and financial technology has created a market environment driven by headline contagion rather than fundamental credit analysis. For Affirm, the private credit market's structural evolution is less a localized threat and more a catalyst that validates the durability, transparency, and superiority of its diversified funding model in a highly restrictive macroeconomic era. The contrast between Affirm's tightening ABS spreads and the explosive credit losses of peers like Klarna confirms that in a high-rate, high-anxiety market, institutional capital will relentlessly seek out structural quality, leaving public equity sentiment to eventually reconcile with fundamental reality.

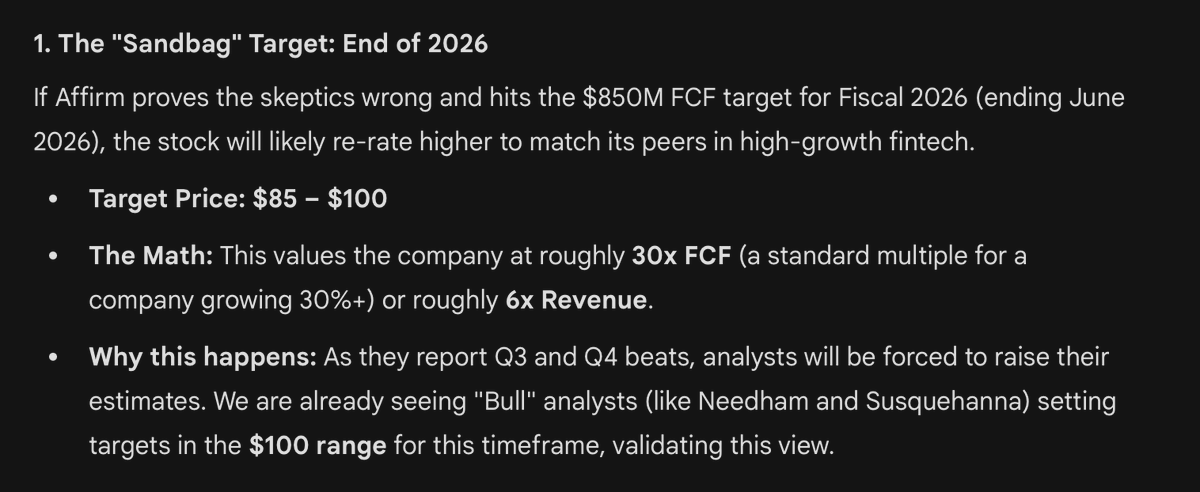

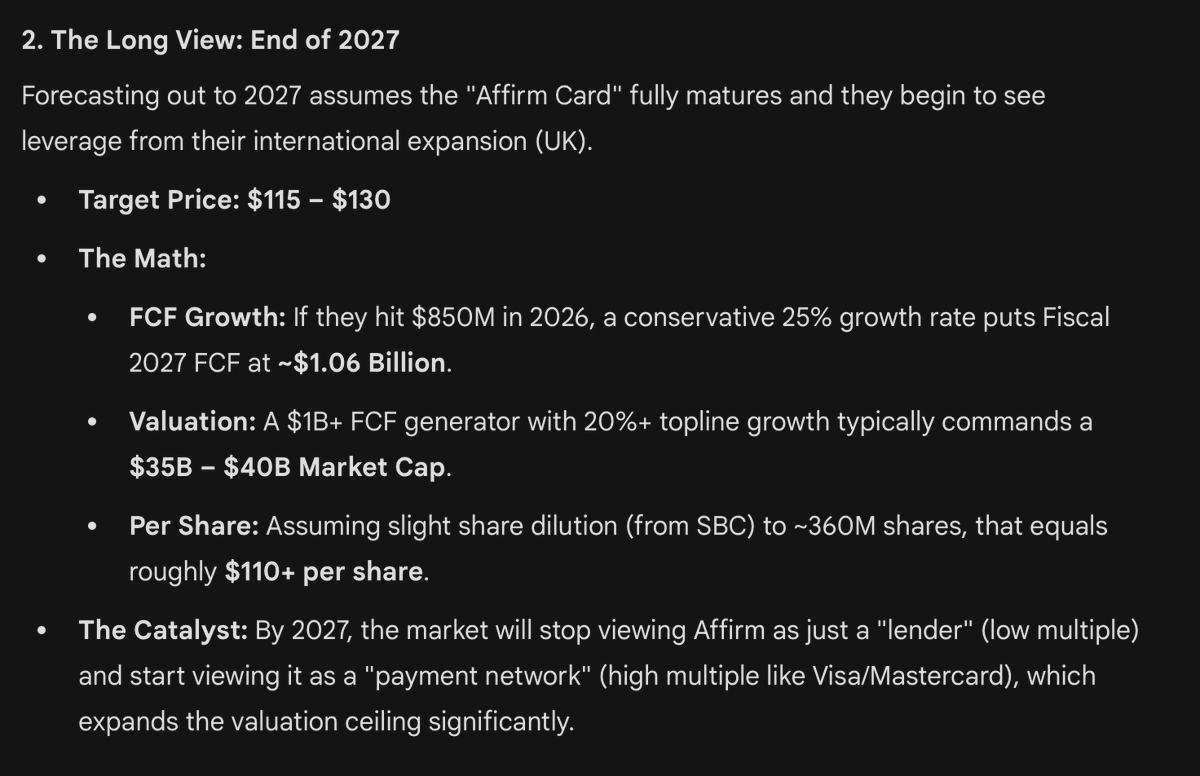

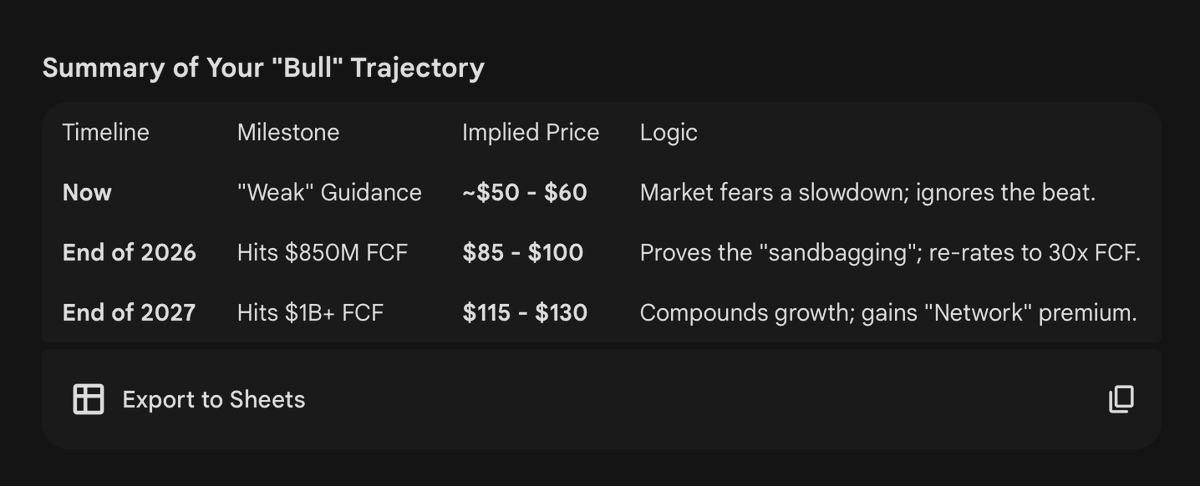

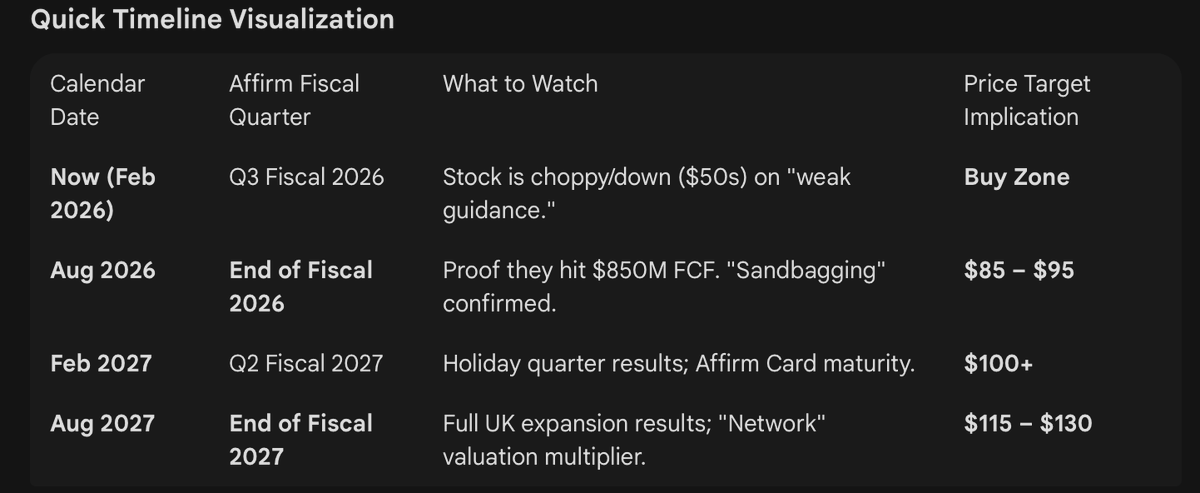

$AFRM Management is sandbagging. Buy.

UNTOLD: JAIL BLAZERS premieres April 14. In the early 2000s, the Portland Trail Blazers were stacked with talent—and surrounded by controversy. Through firsthand stories from Rasheed Wallace, Damon Stoudamire, and Bonzi Wells, this is an unfiltered look at a team caught between brilliance and notoriety—and the media storm that followed.

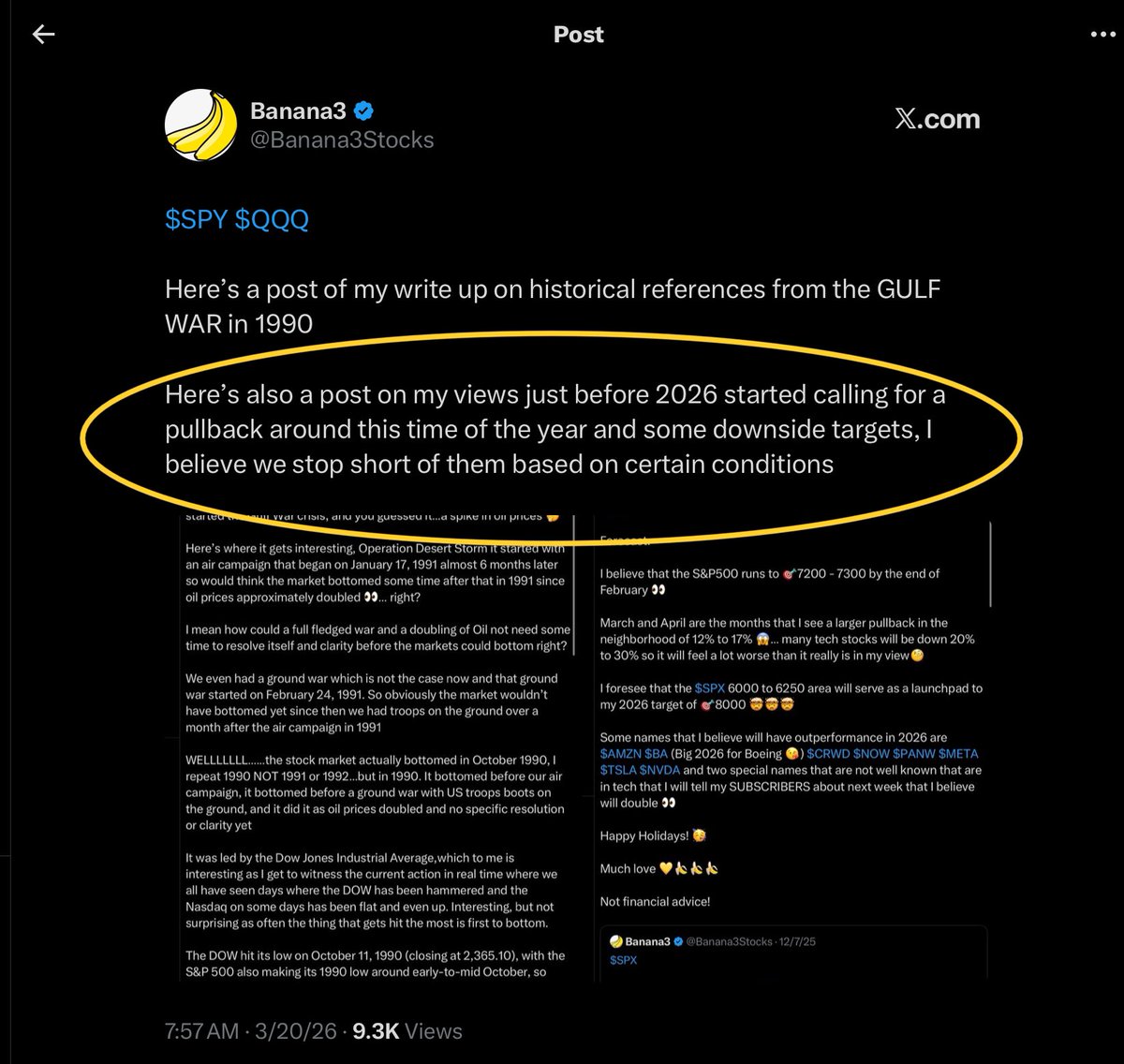

$SPY $QQQ Here’s a post of my write up on historical references from the GULF WAR in 1990 Here’s also a post on my views just before 2026 started calling for a pullback around this time of the year and some downside targets, I believe we stop short of them based on certain conditions