John Doe

350 posts

The level of risk for @US_FDA is unreal. Arm ‘s Length replaced by hand’s up my ass. $QURE

English

@aleabitoreddit @aleabitoreddit Company has 2032 target of 100B JPY Revenue and 25% Operating margins. Do you think they can achieve this by 2028-29 given large capex from memory companies?

English

@aleabitoreddit Very informational report for anyone interested: towajapan.co.jp/en/wp-content/…

English

Yeah... the more I look into things, $TOWA / $TOWCF (6315) at ~$1.34b looks like a sleeper beneficiary for HBM4 spend from SK Hynix, Samsung, $MU.

It’s hyper cyclical with spending cycles.

But we’re seeing hikes in capex spend across the board from memory makers.

Not exactly a 4x type play...

But my guess is that it should get materially re-rated from a spike in unavoidable inflows for the start of the new HBM4 memory cycle anyway.

And they appear to be a largely forgotten beneficiary for this new cycle despite their monopoly in compression modeling processes.

Hybrid bonding just removes one step in the process but requires Towa anyway (monopolies tend to get higher premiums)

I also don't think this cycle is like the last due to how much memory companies have been printing recently?

Just my thoughts, but if my guess is right... it should show up in earnings on the Monday 11th (Tokyo Time) as everyone’s building out HBM4 lines?

Serenity@aleabitoreddit

Monitoring the situation for you (testing/yields edition): $VIAV and $FORM earnings: Extremely Bullish So what does this mean? Names like $ONTO / $CAMT go brr. Throw in $TOWA (6315), since there's indication of aggressive memory production ramp. Names like Msscorps / $KEYS should go brrr. Broader upstream yields, test, validation, and inspection for both memory + optical ecosystem go heavily BRRR. And it's a leading indicator for $COHR, $FN, $LITE, and others if they're ramping up production. For $VIAV: -> $406.8M vs. $393M (beat) 42.8% Y/Y growth. -> $.27 EPS vs $0.2-$0.24 Guidance was $427m-$437m, indicating acceleration. For $FORM: -> $226M, 32% Y/Y, $.56 EPS vs. $.45 -> margins increased a TON to 49% (which indicates pricing power). -> Guidance was $.61 EPS, midpoint ~$240m revenue. "Record demand for High Bandwidth Memory (HBM) and stronger "Foundry & Logic networking applications" Basically the smaller yields/test ecosystem in general. BRRR.

English

@aleabitoreddit Any concerns with HBM5 expected to use hybrid bonding instead of $TOWA compression?

English

I’m personally a fan of the functional monopolies.

Here’s 6 of them that I own.

1. $TOWA (6315) - HBM4 Compression

2. MSSCorp (6830) - CPO Inspection

3. $LPK - Glass Core Substrates

4. $SOI - Silicon Photonics Substrates

5. $AXTI - End-to-End (mineral, refinery, production) InP substrates.

6. $ALRIB - Quantum / MBE (hybrid level systems).

I can’t give recommendations. But for me personally, I wouldn’t buy all of them today eg. AXT until there’s clarity over share authorization + it ran like 1000% already within a small timeframe.

But just thematically as you’ve seen, they tend to outperform so I’m holding all regardless.

There’s a lot more of these out there that you should definitely research yourself.

Always better to teach the thought process so people can do this themselves.

English

Just bought the dip on Dye and Durham

DND.TO / $DYNDF

I’ll keep accumulating at these prices far below insider buys in recent weeks.

Buy out incoming!

Common Sense Investor (CSI)@commonsenseplay

Dye and Durham $DND.TO (CAD) / $DYNDF (US) INSIDERS ARE BUYING ABOVE TODAY’S PRICE! Plantro Investment Company owned by the former CEO, just dropped OVER C$11 MILLION in open-market buys Feb-Mar 2026. - Latest tranche at $4.79 (March 4). - Director Alan Roy Hibben piled in too (50k @ $3.45 + 11k @ $3.66). Current price? Only $4.10 - trading below their most recent buys. Meanwhile the Board is running a full strategic sale (whole company OR Canadian FS division): - First-round bids ALREADY IN ($5.75 to $7) - Second-round bids due mid-April - and they can go even higher ($8 to $12). Takeover premium loading… I BOUGHT BIG.

English

@aleabitoreddit Thanks. Any concerns on HBM5 possibly moving to a hybrid bonding?

English

So just putting it out there: Towa (6315), at $1.35B...

Is a rare, living definition of monopoly over HBM4 (compression molding).

It's been kinda flat YTD, but every memory company like $MU, Sk Hynix, Samsung are their customers. And each of the memory company earnings signaled massive capex increases.

Even as seen with $TSM earnings, every major semi is going through a massive capex cycle to meet AI demand.

And all three memory makers have printed from hbm3e and nand... so the next capex cycle is probably not like the last (meaning a lot more spend).

Like $ASML, this is hyper-cyclical but I wanted exposure to the upcoming HBM4 capex ramp over these next few months.

Thought I'd put this name on people's radar alongside $LPK (glass core substrates) as a functional monopoly.

But I do feel like this timing is about right while every machine supplier is having a massive re-rating yet this was relatively flat.

Not exactly a new find, since a few other analysts + random followers had this name but hope I get the timing right.

(Disclaimer: I do hold positions, this just TLDR of my own thoughts, please don’t copy trade)

English

@KairosPraxis What do you think of $LPK/$LPKF? From what I understand valuation is important to you, so very interested to know what you think in a 1 yr and 3-4 yr time horizon :)

English

Planoptik $P4O touching the €11s again ahead of annual report on Apr 29. This is a superb business and I'm very bullish on the stock in a 2-3 year horizon, but IMO, this is a good time to take *some* profits off the table.

Reminder:

- As per preliminary guidance, Planoptik growing revenue at ~10% in FY26. Margins at best 10%.

- This is a tier-3 supplier two steps removed from $GOOG and one step from $LITE

- They are still ramping up capacity.

- They get at most 1-2% of $LITE's OCS backlog revenue. Glass substrates not there yet.

Kairos@KairosPraxis

Why I think Planoptik $P4O stock is attractive here at 5.8€. - If you assume 10% margin, stock is trading at 21x 2026 earnings - If you assume revenue grows at 15% in 2027 + 12.5% margin, stock is at 14.8x 2027 earnings, which seems cheap

English

@KairosPraxis Yr 1 and 2 based on analyst estimates, also the simplified valuation just for sanity check

English

@KairosPraxis For Credo specifically, Analysts have been revising the estimates up every month, so don't really know how to even value it at this point - also impossible to know how long is this cycle going to be. Did a very simplified discounted earnings valuation earlier today. Wdy think?

English

I've been pitching $CRDO all year so going to disclose that I trimmed my position today.

Credo has a long runway of growth ahead and the new acquisition is exciting... but the story today is no different than yesterday. Optics revenue takes a while to catch up to AECs

Kairos@KairosPraxis

$CRDO is now a photonics stock & cool again. $900M is pricey but 3 things this acquisition achieves: 1. Vertical integration: In-house serdes, DSP, & SiPho PIC inside transceiver 2. Accelerates timeline for 1.6T, 3.2T 3. Differentiation: Dustphotonics known for low power optics

English

@FinnStockinger @MarkosAAIG Thanks guys - the exchange is very valuable to the followers.

English

Sorry man, I've just noticed it after your comment - you’re partially right.

Vera Rubin (R100) no, but Vera Rubin Ultra (R200) partially yes (hybrid).

I’ll try to write something deep, because your quote from yesterday pushed me to dig deeper and look at this from a different angle. I was probably viewing this a bit too “utopian” before, but after focusing on the here and now - surprisingly, I found some “glass” in the story.

English

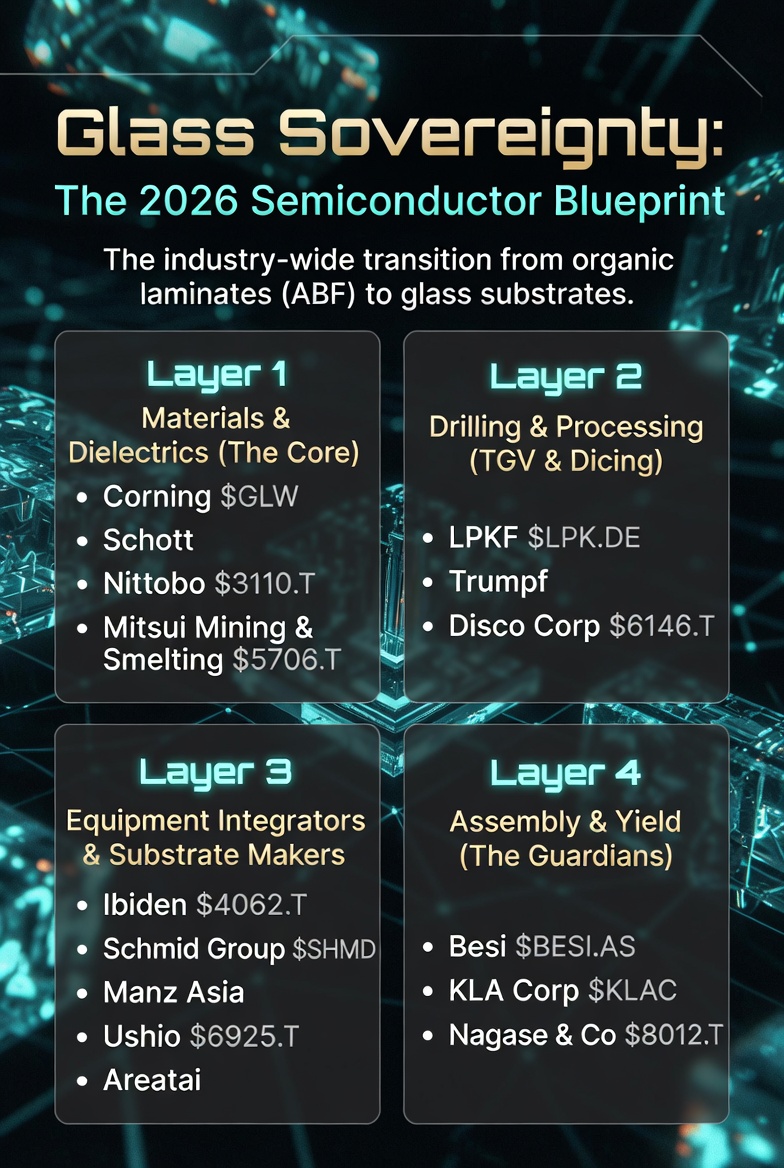

Glass Sovereignty: The 2026 Semiconductor Blueprint

The industry-wide transition from organic laminates (ABF) to glass substrates is now a physical mandate.

Driven by the architectural demands of NVIDIA Vera Rubin (2026) and Feynman (2028), glass is the only material capable of eliminating the "warpage wall" in massive 100mm+ packages while enabling the ultra-dense interconnects required for HBM4.

The 2026 Supply Chain Map

1️⃣Layer: Materials & Dielectrics (The Core)

➡️Corning $GLW & Schott: The primary glass panel providers. Schott has secured a dominant position in the EU and Asia by providing specialized glass for Co-Packaged Optics (CPO).

➡️Nittobo $3110.T: The Strategic Choke Point. They hold a near-monopoly on T-Glass (low-CTE) fiber. The market is currently facing a critical supply shortage, driving up margins.

➡️Mitsui Mining & Smelting $5706.T: Provider of MicroThin™ copper foil, the essential conductor for creating sub-micron Redistribution Layers (RDL) on glass.

2️⃣ Layer: Drilling & Processing (TGV & Dicing)

➡️LPKF $LPK.DE: Owner of the LIDE patent. Their machines are the global standard for high-speed Through Glass Via (TGV) drilling without micro-fractures.

➡️Trumpf (Private): The "engine room" providing the high-power femtosecond lasers that drive TGV arrays.

➡️Disco Corp $6146.T: A mandatory player. Their Stealth Dicing technology is the only reliable method for singulating brittle 700mm glass panels without edge-chipping.

3⃣Layer: Equipment Integrators & Substrate Makers

➡️Ibiden $4062.T: The Japanese heavyweight and Intel’s premier partner. Ibiden is merging its ABF legacy with new glass lines, positioning as the primary volume manufacturer of Glass Core substrates.

➡️Schmid Group $SHMD: Leading the Western push with Vertical Inline Systems. Their tech prevents 700mm panels from sagging a major edge in the US-based Intel ecosystem.

➡️Manz Asia (Private): The dominant integrator in the Taiwanese corridor. Scaling horizontal 700x700mm lines for mass CoPoS production for TSMC.

➡️Ushio $6925.T: Provides large-area Digital Lithography (DLT) for massive 700mm glass tafli.

➡️Areatai (Private): Specialist in molecular-level glass surface engineering, solving the industry’s #1 headache: copper-to-glass adhesion.

4⃣Layer: Assembly & Yield (The Guardians)

➡️Besi $BESI.AS: The leader in Hybrid Bonding. Their machines place chiplets onto glass substrates with sub-micron precision for 16-high HBM4 stacks.

➡️KLA Corp $KLAC: Their Lumina™ series is the only metrology platform capable of 3D-inspecting transparent glass for sub-surface cracks at HVM speeds.

➡️Nagase & Co $8012.T: Supplies specialized chemical etching and cleaning agents for TGV holes.

⬇️Strategic Consensus: Glass Core vs. FOPLP

FOPLP: NVIDIA and TSMC’s primary path for Vera Rubin. Glass acts as a temporary carrier to scale production volume and lower packaging costs.

Glass Core: Intel’s path and the strategic endgame for Feynman (2028). Glass remains inside the final package as a permanent, rigid structural and electrical communication hub.

👇2026 Investor Verdict

1.Safety Play: Nittobo $3110.T. A raw material monopoly in a time of supply crisis.

2. Growth Play: $SHMD & $LPK.DE. Primary beneficiaries of the US and EU push for "Sovereign AI" infrastructure.

3. Blue Chip Play: Ibiden $4062.T. The most stable bridge between legacy packaging and the new glass-centric era.

Bottom Line: 2026 is the "Year of Installation."

Profitability will be dictated by Yield.

The company that first stabilizes 95%+ yields on the fragile 700x700mm format wins.

What's your take on Glass Substrates?

If you liked this post, feel free to share it - it means a lot to me. 👊

#Semiconductors #GlassSubstrates #Nvidia #Intel #TSMC

English

I called my dad today.

He’s 72 and has spent his whole life taking engines apart.

Cars aren’t just a hobby for him - they’re his passion.

My car was in the shop with a couple issues that needed fixing.

Normally I’d call him immediately.

Instead, I caught myself opening ChatGPT first - asking if I was getting ripped off, what questions to ask, all of it.

I stopped.

Closed the app.

Called Dad.

We talked for over an hour.

AI is an incredible tool.

But never let it replace the people who actually love you.

Call your family. ❤️

English

I don’t do stocks or trade full time actually! I have a full time job and I have kids. I also have a part time job. So I do my DD mostly on weekends. I’m currently not interested trading full time. I tend to do long duration thesis growth portfolio, and I don’t trade super often to be honest. If I need to trade it certainly doesn’t require me to be a full time trader. After hours and weekends is my prime time for researching and monitoring. I probably won’t quit my full time job anytime soon, even if I get to my magic number bc of health benefits and retirement benefits. I love this as a hobby and a passion, but more isn’t necessarily better! FWIW

English

For those who do investing full time:

- how long did you need to swap your 9-5 with investing biz?

- what made a difference for you? what advice you'd give to the rest of us who are pursuing this goal?

- is this even possible for 99% of us?

Having a full time job, family, errands, life outside - it all takes time. Is it even possible to make your hobby your primary occupation? Not talking just about buying and selling, it can be any type of work - people who do podcasts, write article, do research, create youtube videos, or anything else.

If you have any experiece trying to achieve this goal, regardless if you achieved it, or currently working on it, or switched to pursue other goals, please share your story.

I hope this brings value not only to me, but to anyone else working towards the same goal.

English

English

Activist-targeted Dye & Durham Ltd. has received preliminary first-round bids for the whole Canadian legal software company and for its financial services division, sources told

@TheDealNewsroom

. The auction is progressing. pipeline.thedeal.com/article/000001…

$DND.TO DND.TO

English

@rorol @TheDealNewsroom Enjoyed the article on Dye and Durham - been following them for a while.

Any updates? You think the sale goes through?

English

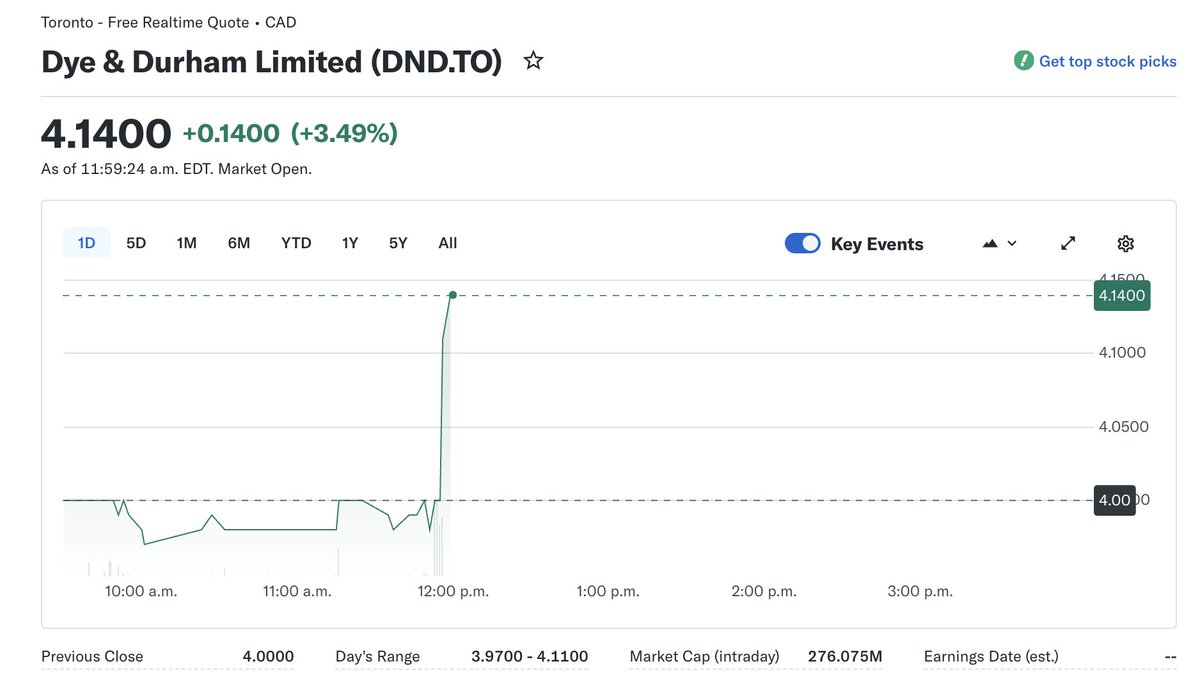

I'm expecting a 20 to 30% rally in Dye and Durham any day now.

Second round bids are due mid April (i.e. this week).

Initial bids were at $5.75 to $7.

Current share price fro DND.TO is $3.99. I think we land around $8 - a double from here!

Trades on US OTC as $DYNDF and the TSX as $DND.TO.

Common Sense Investor (CSI)@commonsenseplay

Trade Alert: I just bought $60k worth of Dye and Durham. $DND.TO $DYNDF Multiple bids received - of $1.7 to $1.8 billion. The company is currently valued at $240 million!!!!! Don't get shaken out. Multibagger!!

English