@theficouple So around 33% of their salary goes to housing, do you mind elaborating on why would this be a problem?

English

OhYesJo

412 posts

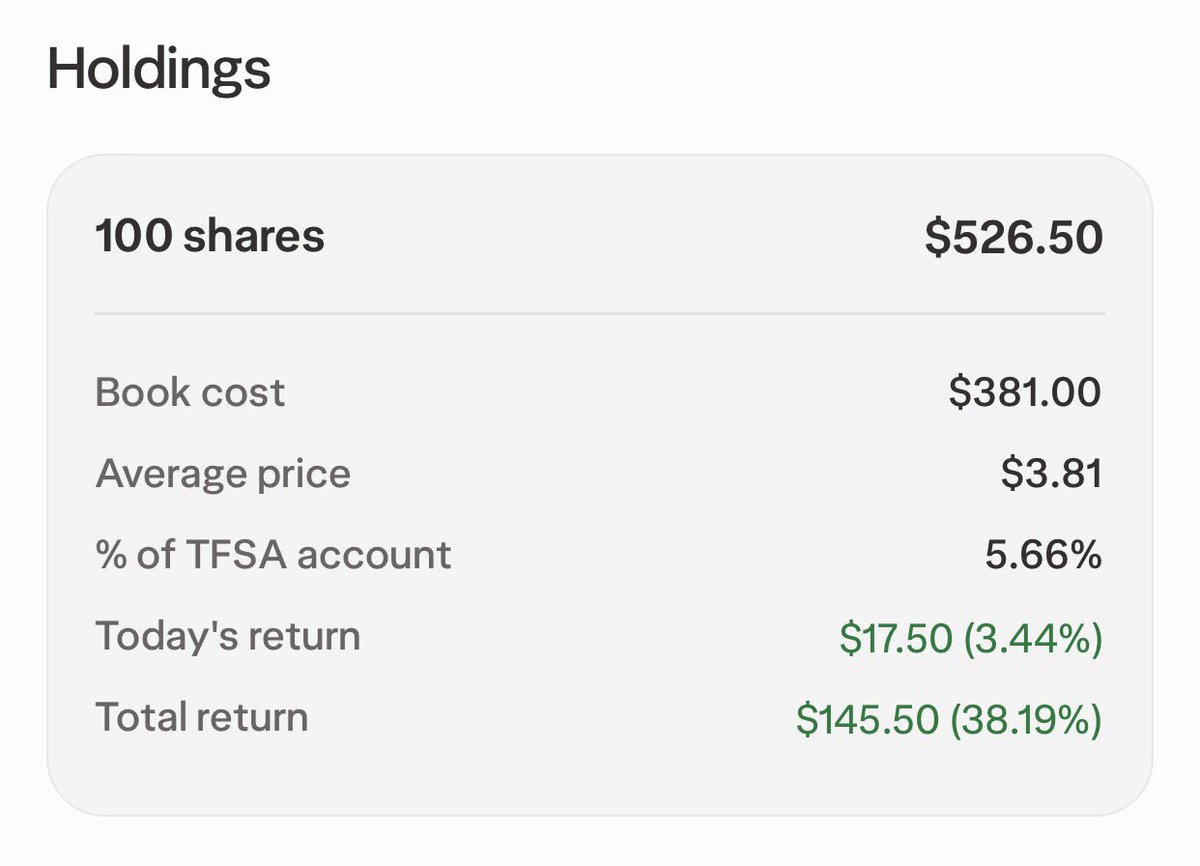

MY BIGGEST, HIGHEST CONVICTION STOCK POSITION! Dye & Durham $DND.TO (Canada) $DYNDF (US) - The Forced Takeover Story Nobody Is Talking About! Dye & Durham - is one of the most explosive special situations in Canada and the endgame is almost certainly a buyout! Here’s the real sequence: 1. Just over 7 months ago, Advent International (a top-tier global PE fund) made an ~$825M offer (~$12/share). - D&D’s board rejected it. - This decision set off the chain reaction. 2. Ex-CEO Matt Proud (Plantro) started trying to take the company private, he made multipe buyout offers: - Feb 2025: Bid #1 - $20/share - Fall 2025: Bid #2 - $10.25/share - Nov 2025 (just last week): Bid #3 - $5.72/share ($3.50 cash + $2.22 notes, ready to sign immediately, no further diligence) His offers dropped as the company deteriorated - filings missed, downgrades hit, strategic review collapsed! 3. Fast-forward to this month: - Stock hits an all-time low of $2.71 - D&D faces OSC scrutiny, delayed filings, lender cure periods - CIBC backs out of the strategic review - Credit downgraded by S&P & Moody’s 4. Then everything blows up: - Three directors resign. - A new Chair + new CEO installed. - Tyler Proud (ex-Chairman) and brother of Matt launches a proxy fight with his own board slate. - Plantro fires in its 3rd offer and says it can “sign immediately.” This is not a normal company. This is a forced resolution. Buyout Probability: ~90% once filings land (within next month) Why? • Board weakened • Two Proud brothers pushing from opposite sides, one to control the board, one to buy the company. • No credible public path • No bank-led strategic review • Lenders want stability • Governance vacuum • Advent previously saw $12/share value in value This ends in a transaction - the only question is at what price. Upside from today’s ~$3.20 share price - $5.72 current offer = +79% - Likely revised bid ($6–$6.50) = +87% to +103% - Advent valuation anchor ($10–$12) = +212% to +275% The key risk window: - D&D must file its Annual + Q1 statements by mid-December and secure lender waivers. - If they do - catastrophic downside disappears and this becomes a pure negotiation! Their latest update on this from 2 days ago is that they will meet that timeline. Bottom line: The Proud brothers aren’t fighting for a $3 stock. They’re fighting because privately, D&D is worth far more than the market is pricing. The buyout probability is extremely high 90%+ The only real debate now is the final price. Dye and Durham is now my biggest highest conviction long!