JP

13 posts

Bitcoin is Digital Capital. Strategy transforms it into Digital Credit. $BTC

English

My $DRAM $60 calls I opened yesterday are going to print at market open

GIF

English

JP retweetledi

By 2044,

Those who own an entire Bitcoin have essentially secured 100 years worth of labor,

#Bitcoin operates without...

governing bodies, charismatic figures, institutional funding, management tokens, corporate alliances, lavish headquarters, venture capital support, legal representation, initial mining advantages, or a strategic blueprint.

It functions as a self-sustaining asset.

For instance,

Seeking to confiscate my funds?

- You're unable to do so.

Wish to restrict my purchases?

- I'll proceed regardless.

Aiming to devalue my wealth through inflation?

- Not feasible.

Did you assume that the most significant transfer of wealth in history would occur seamlessly? 🤔

Your time is running out.

English

JP retweetledi

JP retweetledi

#Bitcoin enables focusing on things that truly matter.

It is focus that makes time valuable.

Time without focus is similar to a car without fuel.

Focus serves as the vehicle.

Time acts as the expendable fuel.

One without the other leads to stagnation.

Many of you have time.

You simply lack the mechanism to render it valuable.

"Life" is exceedingly "brief".

Don't waste it, extend it!

English

JP retweetledi

JP retweetledi

"When you print $5 TRILLION dollars that you put into the economy"

"You have diluted the value of the money"

"This is what happens when you have the quantity of something and you add more to it"

"This is dilution"

"The principal is so simple that a child can understand"

🚨🚨🚨

English

JP retweetledi

I am a saver, not an investor.

I’m probably outperforming the top investors, while working.

It’s not hard.

Just save in #Bitcoin.

It will get intense for those who don't see the lines clearly.

This is also the time for DCA into Bitcoin.

It will be life-changing if you manage to keep it in a secure cold storage.

If you’re not bullish now, you need to revisit the drawing board and study Bitcoin again.

Bitcoiners will outperform every hedge fund;

that is a wild thing to comprehend, and many will understand this too late.

English

JP retweetledi

Michael Saylor explains the “magnificent seven” stocks (such as $META, $GOOG, $NVDA) as the current conventional “investments” & how they aren’t the best idea & why #bitcoin is the bigger idea

English

JP retweetledi

Fix the money, fix the world.

Incentives rule the world, and we need better ones.

#Bitcoin literacy offers this.

If every human on Earth studied the zero/first principles of Bitcoin, it would literally change the direction of our species towards a closer type of utopia.

I firmly believe this.

No matter the sector you are in,

incentives run the world, and they are extremely misaligned with human life, extension, and fulfillment.

Bitcoin fixes this.

Change my mind.

English

JP retweetledi

Let's talk $MSTR. There is a lot of information out there right now about their premium so lets dig in deep. Sorry in advance for the long post, but I think this is an important topic.

TLDR

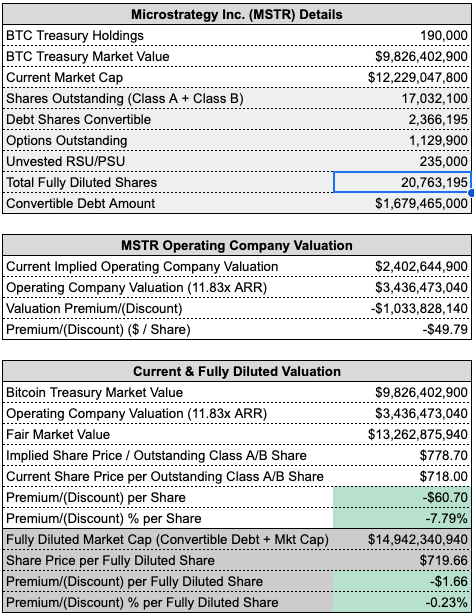

MSTR is undervalued on a fair market basis based on their bitcoin holdings and operating company value. Fair market value as of today is estimated at $778.70 per outstanding Class A/B share. The market is near market value when considering full dilution with a value of $719.66 per fully diluted share vs. today's closing value of $718. Homework an assumptions shown below.

Shares Outstanding

A lot of analysis on X right now is using simply Yahoo Finance or Google Finance data. This often reports only Class A shares (14.904M) leaving large gaps in both shares outstanding and market cap.

In addition to the 14.904M Class A shares, MSTR also has 1.964M Class B shares outstanding.

This gives us a Basic Shares Outstanding of 16.868M shares.

However, even this doesn't give the full story. So far in 2024 164,100 options have been exercised with 150,000 of those coming from @saylor. These shares increase the Class A shares outstanding and thus results in a new Basic Shares Outstanding of 17,032M (Used for Fair Market Calculations).

There are additionally 1.13M options outstanding which given the performance of the stock are almost certainly in or near the money and likely to exercise. This would provide 18.162M diluted shares. Saylor is exercising 5,000 options every trading day through the end of April with 250,000 remaining to exercise.

We then must look at the convertible debt shares. There are 2 notes with convertible debt.

The 2025 Note is convertible at $398/Share and would provide 1.633M shares to the debt issuer. Given how deep in profit these shares are, we can almost certainly assume the intent to convert these to shares.

The 2027 0% interest Note is convertible at $1,432/Share (a 99% increase from current price). This conversion would add another 733K shares. Given the 0% structure of this note, it is almost certainly a direct play to #Bitcoin and $MSTR's leveraged strategy to create value. While it seems far off from being profitable, it still has 3 years to maturity. At the moment I would consider these as intended to convert.

With the inclusion of these, we now have a diluted Shares count of 20.528M.

The last category is RSU/PSU. This is a smaller category with 235,000 shares.

With these categories considered, we have a fully diluted share count of 20.763M Shares (used for fully diluted calculations).

Trading Premium

The premium is not as straight forward as most would like it to be. Most are simply taking the premium as Market Cap / BTC treasury value.

While this is a simplistic approach, It ignores the fair market value of the operating company which generates $500M annually in revenue profitably.

Lets take a MSTR competitor as a comparable using $GWRE.

GWRE generates ~$830M in revenue based on their last quarter run rate, and are on track to lose $108M annually. However, for SaaS companies the market hardly cares about profitability as much as they do about ARR growth.

What is the market cap of this unprofitable software company? $9.89B. Of this amount, I would attribute $781M to their treasury or Cash/short/long term investments (being conservative and including all). So operating business only (for comparison purposes), let's call it $9.10B in operating company value.

But how do these companies get valued? Typically, they use a multiple of ARR (Annual Recurring Revenue) to determine the value of a SaaS company.

With an ARR of $770M, GWRE currently has a multiple of 11.83x ARR. Note that this multiple has lowered drastically from the 18-22x ARR valuation of a couple years ago in the SaaS space.

So what about MSTR? As they are in transition to their subscription/cloud model, I'm going to assume their Product Licensing and Subscription Services Revenue convert directly to ARR. Additionally, I will assume they will be able to convert at least 50% of the product support revenue into their subscription model as deals renew (conservative) to boost their ARR. This is conservative as they will certainly try to convert 100% to increase enterprise value.

This amounts to $72.622M per quarter, or ARR of $290.488M. Using our multiplier of 11.83x ARR we get an operating company value of $3,436,473,040.

So what does this tell us? Basically, that even with the run up in the price, $MSTR is still undervalued from a fair market perspective. As of market close today, the market was giving MSTR an implied operating company valuation of $2.4B.

This indicates the market still is trading at a discount of $60.70 per current outstanding Class A/B share. So as of close today, the fair market value of $MSTR should be $778.70 considering the price of their BTC holdings and our estimated operating company value.

Fully Diluted Valuation

We get a different story when looking at fully diluted valuation. The fully diluted valuation which includes current market cap plus the full convertible debt about divided by fully diluted shares indicates the market is nearly trading at fair value. The discount with these considerations puts the discount at a paulty 0.23% or $1.66 per fully diluted share.

Conclusion

The market has yet to determine the fair market value for $MSTR, and we are not currently in the throws of a short squeeze. At the moment, at worst we are simply looking at an undervalued company which has been pegged as a "Bitcoin Value Only" approach by most investors. There is still lots of room to move and we will continue to monitor as this progresses. At best, the market is trading near fair value when considering full dilution.

Would love feedback or other approaches/opinions from anyone who has a view on valuing this unique organization. @adam3us @BitPaine @IIICapital @lylepratt @saylor

English

JP retweetledi

Anyone who is waiting for a 20k #Bitcoin will end up buying BTC above 100k...

Bears are in disbelief. 🐻

They were calling for not only 10k but also 3k.

Many of the major bears were literally staking their life's bet on the failure of this asset.

It's unbelievable that they called for 3k = insanity.

BTC will continue to dematerialize every asset in the world.

Bitcoin changes everything because it protects the most precious, scarce thing in this world: your time. ⏳

The Last Safe Haven,

Opt out, Buy #Bitcoin, put it in cold storage 🧊

There will soon come a time when people will no longer be willing to exchange their ₿ for $.

Gradually, then suddenly!

English