Julian Smith

623 posts

Julian Smith

@jsmith_dev

🇦🇺🇨🇳🇺🇸💻 Fund Manager & Software Developer (20+ yrs) Partner @mainstvent. Tech Entrepreneur & Anti-War 🕊️ Libertarian.

Melbourne, Victoria Katılım Temmuz 2020

576 Takip Edilen263 Takipçiler

All tax evasion should be called out.

Following up on yesterday’s post in regard to the taxation of offshore Oil and Gas companies it was pointed out that Oil and Gas companies can shift their profits offshore to avoid tax in Australia.

That’s 100% correct, but it’s not isolated to just Oil and Gas companies.

Offshore profit shifting is rampant amongst all multinationals.

Why don’t the Greens or David Pocock have a 25% export tax on all profits sent offshore?

Why can Pfizer, Meta etc send billions of dollars offshore to avoid paying tax here in Australia?

Why can Australian companies especially banks, offshore jobs to India and the Philippines without paying any withholding tax.

Why don’t renewable companies, 70% owned by foreigners have to pay a royalty on our sunlight and water?

Peoplefirstparty.au is the only party to have a policy on profit shifting and is the only party to have consistently raised these issues in estimates and the Senate.

We will raise the withholding tax rate on profits transferred to treaty countries to 25% and on interest income paid to all countries to 30%. This will prevent capital from leaving Australia and ensure that profits generated domestically contribute to our economy, rather than being funnelled offshore.

Additionally, an operating profit ratio test will be introduced to further strengthen transfer pricing rules and prevent the leakage of profits abroad.

If you’re going to call out one industry for tax evasion then call out all companies.

Otherwise you’re just demonising the industries you’re trying to destroy.

English

@Potstirrer111 It is relevant to the forecast/expectation that prices will or must fall: x.com/jsmith_dev/sta…

Julian Smith@jsmith_dev

On median Australian 🇦🇺 numbers: Removing negative gearing offsets requires roughly +13% aka $88/week rent growth to restore investor after-tax cashflow. The converse is median drop of 33% aka $300k on Australian residential investment property. Which do you see happening?

English

@RobbieBarwick That sounds like an apra.gov.au. Australian banks are structurally optimised to lend against collateral, not productivity. Australian mortgages are treated almost like quasi-sovereign assets inside the banking system.

English

Liberal senator Jane Hume: "We should be encouraging more start-ups."

I'm getting sick of this discussion about "start-ups".

They mean modern "tech" companies that hope to spark a stock market frenzy that makes the founders billionaires.

They don't mean manufacturing enterprises that could help reindustrialise Australia.

We send those offshore.

Here's an example:

In the 1990s a Melbourne engineer invented an oil-free compressor.

He couldn't get any bank or investor in Australia to back him.

A Canadian government development bank offered to invest in him on the condition that he set up production in Montreal. So he did.

Later an American company bought his operation and moved it to Tallahassee, Florida, where a little while later it was bought by giant Danish compressor company Danfoss.

The average salary at the Tallahassee plant is US$90K.

They could have been jobs in Australia, but we don't have a government development bank, or banks with vision, or any inclination to back real industries.

However, we do want young people to believe if only they could create the right app they could become billionaires.

English

On median Australian 🇦🇺 numbers: Removing negative gearing offsets requires roughly +13% aka $88/week rent growth to restore investor after-tax cashflow. The converse is median drop of 33% aka $300k on Australian residential investment property. Which do you see happening?

English

@Potstirrer111 That’s a pragmatic view. Essentially the buyer’s agent is advising not to panic and weather the storm 🌊 why crazy?

English

@Potstirrer111 In fairness, it might mean that.. not wrong, it’s a valid variable. But also, the amount of population demand vs slowing of rates of construction / completion to balance supply and demand coupled with increasing building construction costs is a huge factor too.

English

@jsmith_dev Not must. It means they overpaid and prices have to fall so yields catch up

English

@alisterberkeley @cjoye Australia 🇦🇺 lacks a 1031 exchange equivalent

English

There is an additional dimension to CGT on business @cjoye Governments treat entrepreneurial wealth as static consumption wealth rather than recycled productive capital.

For many serial entrepreneurs, a successful exit is not the end point. It is the funding mechanism for the next company, the next technology, the next jobs, and the next ecosystem. They often reinvest aggressively because they have pattern recognition, networks, operational experience, and a tolerance for risk that most people do not.

When the state heavily taxes those capital returns, it is not merely redistributing wealth. It is reallocating capital away from a proven allocator of risk capital and toward the government itself. Implicitly, the state is saying: “We can deploy this marginal dollar more productively than the entrepreneur who created it.”

christopher joye@cjoye

But they have never worked a day in the private sector; never started a business; built a new product or service; hired a single soul from their hip pocket; or struggled for years, always at risk of going under… What we are seeing is the lid being lifted on those who have always lived completely taxpayer-funded lives trying to take and tax as much as possible to feather the public sector nest. They have never known what it is like to draw a private wage and/or profit. They think it is a zero sum game: any private income, profit or capital gain needs to be redistributed back to government and its dependents. It is the only way they know how to make money: by taxing private citizens and corporations to fund the public oligarchy and its way of life…

English

“Channel all wealth into the family home”

“Done”

“Now tax the principal place of residence”

English

Do you genuinely believe what you write here or just deliberately avoid key context as sophistry for partisan effect ?

Ash@AshPolitik

The "death tax" scare campaign is the laziest dog whistle in the playbook. Here are the facts straight from the Budget papers and ATO: Inheritance isn't taxed. Estates aren't taxed. Farms are exempt. Small business CGT concessions are retained in full. Existing testamentary trusts are grandfathered. Fixed testamentary trusts can still be set up for new wills at zero extra tax. The only change: new discretionary testamentary trusts created after 12 May 2026 will pay a 30% minimum on trust income from 2028. There are about 10,500 testamentary trusts in Australia — 1% of all trusts. And only the discretionary, income-splitting variety set up from now on is caught. 30% is what a nurse on $80k already pays on her top dollar. The Right isn't defending battlers. They're defending the tax planning industry that lets wealth split income across grandkids and bucket companies to pay less than wage earners on the same money. If you want to leave assets to your kids, nothing stops you. What's stopping is the loophole.

English

Oooof… this makes a compelling point. What is the AG Office’s view? @agdgovau

christopher joye@cjoye

From a reader... Dear Sir Under current legislation, all trusts (not just discretionary trusts) are taxed on accumulated income to which no beneficiary is presently entitled. Such income tax is assessed to the trustee under section 99A of the Income Tax Assessment Act, 1936 (“the Act”). The tax rate assessed to the trustee is at the highest marginal rate, plus Medicare. That imposition amounts to 47% of the accumulated income. The Commissioner retains a discretion to assess such income under section 99 of the Act, (which applies personal rates of taxation) but that discretion is exercised sparingly and only in limited cases, such as deceased estates and bankruptcies. Again, under current legislation, a share of trust income – to which a minor or a non-resident beneficiary is presently entitled to – is assessed to the trustee under section 98 of the Act and assessed again to the beneficiary with a full credit given to the beneficiary for the tax assessed to the trustee. The 2026 Federal Budget proposals change the concept of the taxation of beneficiaries of trust estates that has applied since the Federal Government introduced income tax. That is done by treating the trustee as a separate taxpayer on income to which beneficiaries of a discretionary trust are presently entitled to. Now, a beneficiary is said to be presently entitled only on the after-tax net income of a discretionary trust estate. Any credit for tax paid by the trustee, under these new proposals: is not fully credited to the beneficiary if it produces a cash tax refund to the beneficiary, and in the case of a corporate beneficiary the tax paid by the trustee is not credited at all. With all due respect to Treasury officials and the Treasurer, who devised this new arrangement, there is a complete misconception on who is being assessed on income to which a beneficiary is presently entitled to. Unlike companies, where the taxable income of a company is legally and beneficially derived by the company, in the case of trusts, including discretionary trusts, any net income of a trust estate to which a beneficiary is presently entitled to is income of the beneficiary, not the trustee. By taxing the trustee on income to which the trustee is not beneficially entitled to, and not passing the tax paid by the trustee to the beneficiary who is entitled to that income from the trust estate is not a tax, but – in my opinion – an illegal penal confiscation. Allow me to explain: The Core Problem: When a trustee is assessed on income to which a beneficiary is already beneficially entitled, without any credit (or a full credit) being passed to the beneficiary, two (2) serious legal problems arise with regard to the Constitutional validity of the legislation purporting to assess: 1. Section 51(ii) — Is it a Valid "Tax" or a Penalty/Forfeiture? The High Court in Matthews v Chicory Marketing Board (Vic) (1938) 60 CLR 263 confirmed that a tax is "a compulsory exaction of money by a public authority for public purposes, enforceable by law, and... not a payment for services rendered." A "tax" – in the constitutional sense – requires it to be imposed for revenue-raising purposes, not as a punishment or confiscation. See Woodhams v Deputy Commissioner of Taxation of the Commonwealth of Australia (1997) VSC 59 on what constitutes a penalty (and not a tax). The key issue is whether imposing the full tax burden on a trustee — without any (full) credit mechanism for the beneficial owner — crosses the line from taxation into something more like a forfeiture or a penalty. In these circumstances, I submit the trustee’s right to exoneration and indemnity are in jeopardy and a beneficiary would be entitled to restrain the trustee from using trust funds to discharge a personal obligation, that is not a fiduciary obligation, even if the obligation was imposed by flawed legislation. 2. Section 51(xxxi) — Acquisition on Just Terms If the Commonwealth imposes a liability on a trustee with respect to property or income beneficially owned by another, and the trustee cannot recover that tax from the trust estate or beneficiary through the tax legislation itself or under the terms of the relevant trust deed, this could constitute an acquisition of property (money) from the trustee without just terms, contrary to s 51(xxxi) of the Commonwealth Constitution. The High Court has ruled in Minister of State for the Army v Dalziel (1944) 68 CLR 261 and most recently in Government of the Russian Federation v Commonwealth of Australia [2025] HCA 44 that section 51(xxxi) of the Constitution will protect a party whose property is assumed by the Commonwealth without compensation. The term “property” is widely characterised to give the affected party full constitutional protection. In my view, the proposed arrangements don’t fall into the unintended consequences camp, as is often claimed when some controversy is later discovered after a proper and considered analysis. In this case, the proposed arrangements are fundamental misconceptions, that fail to recognise basic constitutional protections.

English

Oh… the State’s hand is always out. It’s just sheer number of pockets they are putting it in is disturbing.

chairman Beans, IQ 277@justbeans4

Rich people want government handouts for everything you'd think its socialism

English

"The Capital Gains Tax…if I had known they were going to do that, I wouldn’t have voted for them. I voted for Albo and Chalmers. They didn’t have a mandate for changing Capital Gains Tax. It’s now the highest in the world. No-one is going to want to invest in Australia. What the fuck are you doing?"

@DHughesy

Valerie 🤌🏻@AussieVal10

Welcome to the “right” side Hughesy! And keep going 👏🏻👏🏻👏🏻👏🏻👏🏻 The more the merrier speaking out about the morons in power in Aus!

English

@AbdulKhalid25 @RBASHAGGER I realise it’s hard to understand from first glance, but Jim Chalmers isn’t actually Ed Harris in “The Truman Show” directing the economy. This is parody. Moron.

English

Julian Smith retweetledi

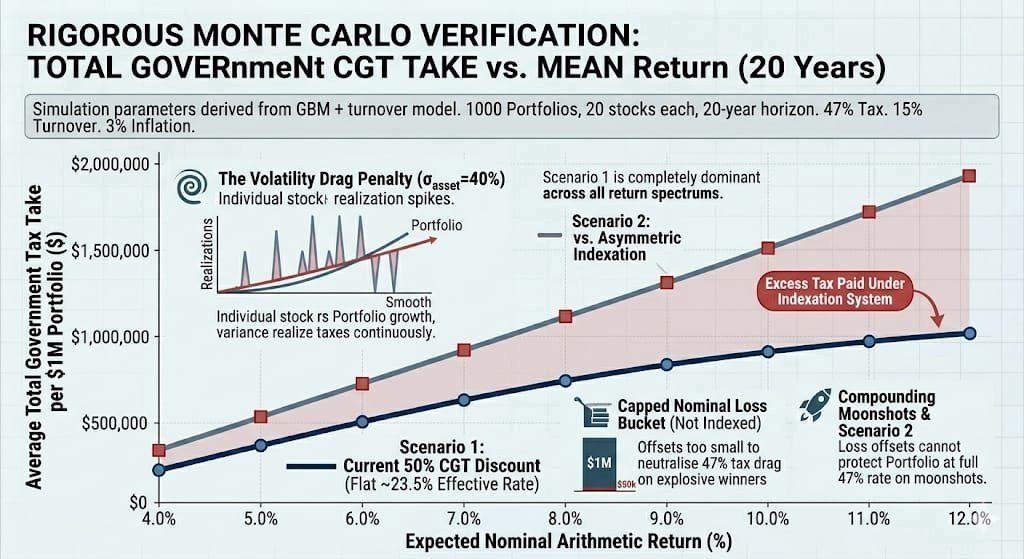

Small Cap Investing is Dead with a 77% spike in Tax Collection

I have run 1,000 Monte Carlo simulations of portfolios of 20 Small Cap Stocks with the New Inflation Corrected CGT model versus the existing 50% CGT discount model.

The results are devastating.

The bottom line is that small caps are highly asymmetric bets where your small number of winners are meant to compensate you for your many losers. Mining companies are a good example of this situation and are a fundamental pillar of our national wealth. However if you tax those few winners at 47% with the trivial relative inflation correction you effectively wipe out the ability to offset your losses. This is because the tax drag on your few multi baggers is so high that it changes the entire logic of the investment process.

It's become a loser's game.

1. The Moonshot Tax Penalty:

Because Australian small caps rely heavily on a right-skewed distribution (a few massive winners offsetting many losers), the Indexation framework introduces a devastating tax penalty. For a stock that goes from $50,000 to $400,000, a 3% inflation adjustment on the original $50,000 cost basis is completely negligible. Under Indexation, you forfeit the 50% discount and pay a flat 47% on nearly the entire gain.

2. The Turnover Trap:

With a 15% annual turnover, small-cap portfolios realize taxes continuously. Under the current system, every partial sale triggers a flat 23.5% effective tax rate, leaving more money inside the portfolio to compound. Under indexation, those early wins are hit at a full 47% clip, severely dampening the portfolio's forward compounding engine.

3. The Asymmetric Loss Failure: in small-cap investing, a stock can only ever lose 100% of its value, but explosive winners have unlimited compounding upside. The government’s asymmetric tax system completely devastates this dynamic: by replacing the flat 50% CGT discount with inflation-indexing for winners only, it leaves your nominal losses capped and completely unable to counteract the massive tax hike on your multi-baggers. Because a 3% inflation buffer barely dents a 400% moonshot gain, you end up paying a brutal, un-discounted 47% tax rate on the very winners that drive a small-cap portfolio's success, causing a 77% spike in total government tax take overall.

Even in investing we see the socialist government wants us all to be the same. Communists.

(Technical notes: Model executed using Gemini Pro with 1,000 portfolios of 20 stocks each with the volatility and median return typical of this class of small cap stocks over the last 10 years, using a geometric mean process to step forward each portfolio each year).

English