Sabitlenmiş Tweet

Thought of the day: tech stocks that need to invest in AI now have had capex drag FcF and, in the short run, are more like industrials that, by necessity, have regular and recurring capex spend.🤔

English

Alister Berkeley

2.5K posts

@alisterberkeley

Managing Director at Berkeley Advisory focused on getting companies and founders "fit, funded, big, and out." Founder of DragonAI: Agentic stock analysis rubric

This message exchange is with my ex-wife who is a Partner at a New York law firm working in international financial markets @GeoffWilsonWAM @cjoye 🤯

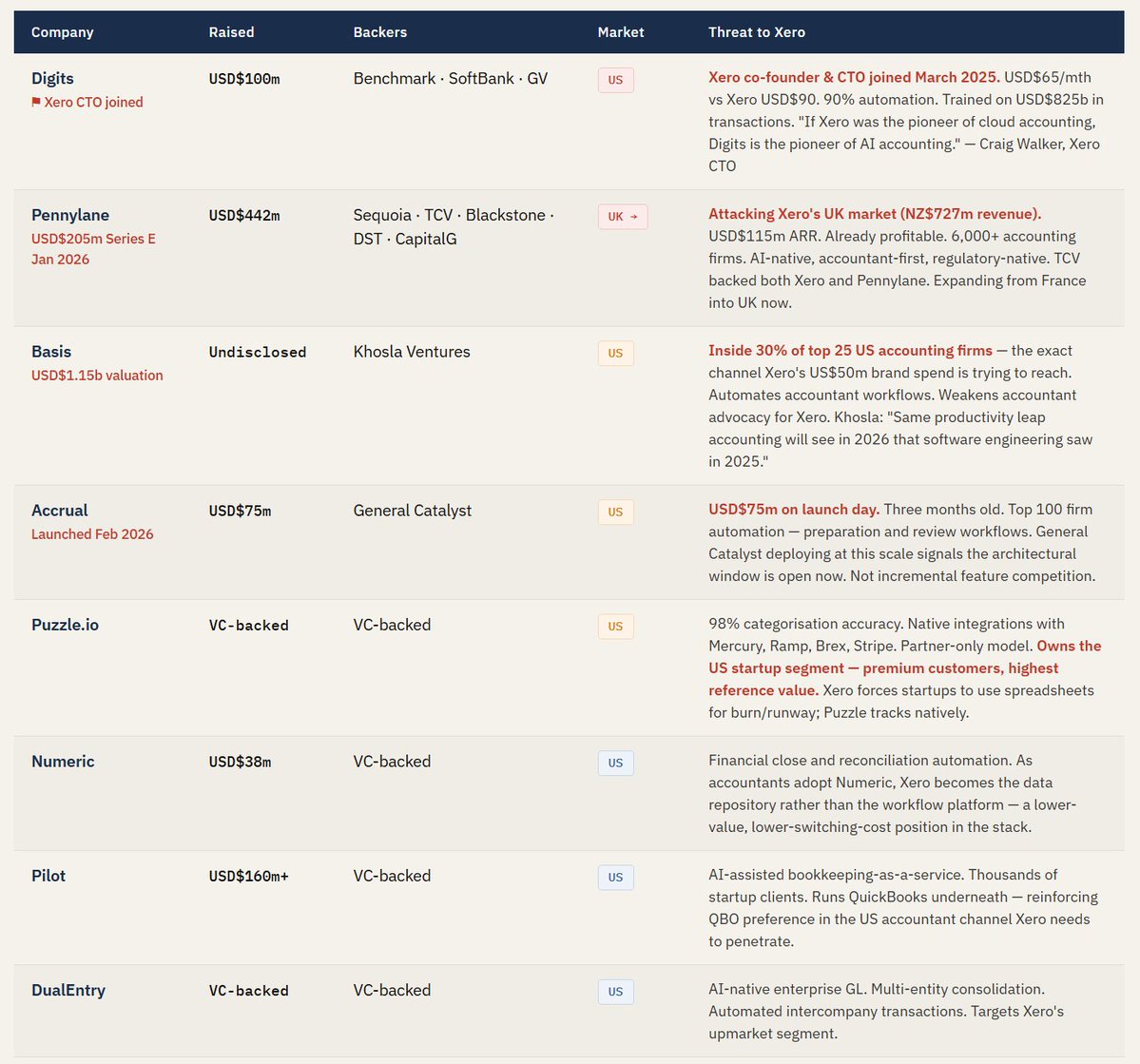

Think about how many companies globally carry capitalised software development costs on their balance sheets. Every #SaaS business that capitalises under IAS 38 or ASC 350. Atlassian. Wisetech. TechnologyOne. ServiceNow. Salesforce. SAP. Thousands of listed technology companies across every exchange in the world. Every one of them has a gross capitalised software balance built at historical labour rates and historical productivity assumptions, costs accumulated over years, of what AI can build in weeks or months. Every one of them has an auditor who is now, or will soon be required to assess whether significant changes in the market constitute an impairment indicator for those assets. Every one of them has a useful life assumption that was set before AI coding tools compressed development timelines by 40-75%. Almost none of them have disclosed what that productivity improvement actually means for the asset sitting on their balance sheet. Now apply the same question to every other software company on every other exchange. What is the gross capitalised software balance? What productivity improvement has the company disclosed from AI tools? What is the implied replacement cost at that productivity improvement? What does the auditor's KAM language say about whether the market change indicator was specifically assessed? Every technology company that has been capitalising development costs at historical rates while AI tools quietly made those historical rates obsolete. Most of the market has not noticed yet. $XRO.AX $WTC.AX $TNE.AX $TEAM $NOW $CRM $SAP $INTU $MSFT $ORCL $ADBE $WDAY $HUBS $ZM $SNOW $MDB $DDOG $GTLB $CFLT $BILL #CapitalisedSoftware #IAS38 #ASC350 #SoftwareImpairment #AIProductivity #UsefulLife #FairValue #ValueInUse #IAS36 #TechAccounting #ForensicAccounting #SaaSAccounting #AIDisruption #BalanceSheet #AuditRisk #KeyAuditMatter #ASU202506 #IFRS #TechInvesting #ASX #XRO #Xero #SaaS #AIAccounting #ReplacementCost #AccountingStandards #CapitalisationRate

Xero $XRO.AX has NZ$720.9m of software sitting on its balance sheet. Built at historical labour rates. Historical productivity. Their own annual report says AI tools let them rebuild a product that took 6 months in 10 weeks. That is a 75% productivity improvement. Apply that to the NZ$720.9m and the replacement cost of the same software today is NZ$180m. Implied writedown: NZ$541m. But here is the thing. That writedown does not happen. Not today. Not under the accounting standards. NZ IAS 36 uses the higher of replacement cost and value in use. Value in use is the discounted cash flows from 4.92 million customers paying NZ$51 a month. That DCF is approximately NZ$4.4 billion. Against a book value of NZ$720.9m. The cash flows bury the replacement cost argument completely. For the asset to actually be impaired on a value in use basis, Xero would need to lose 1.2 to 1.5 million customers. That does not happen overnight. So there is no writedown today. The accounting is technically correct. The risk is not a writedown. It is useful life compression. Xero amortises capitalised software over 3 to 7.5 years. That assumption was made when the relevant question was how long before a competitor could build something better. Digits built a competing general ledger in less time than Xero spends capitalising development costs in a single year. Pennylane built a profitable USD$115m ARR business from scratch in five years. If AI-native architecture makes existing software architecturally obsolete faster than the amortisation schedule assumes and the evidence suggests it does the useful life needs shortening. Not impairment. Just faster amortisation. Shorten the useful life to 3 years across the portfolio. The incremental annual P&L charge is NZ$103m. Against true distributable FCF of NZ$277m. That is 37% of distributable earnings consumed by accelerated amortisation. The key is whether the useful life assumptions still hold at the next audit.

How do we make Australia more prosperous? How do we encourage people to build businesses, take risks and compete with the rest of the world? Our politicians and government are spending the money that comes from our work, our risk and our effort. So we should demand more from them. More innovation. More ambition. More bold decisions. As Australians, we should expect to have one of the highest standards of living in the world. Let’s demand this from the people who lead us.