Josef Vesely

1.1K posts

What stock will be the best performing in 2026?

English

Josef Vesely retweetledi

Josef Vesely retweetledi

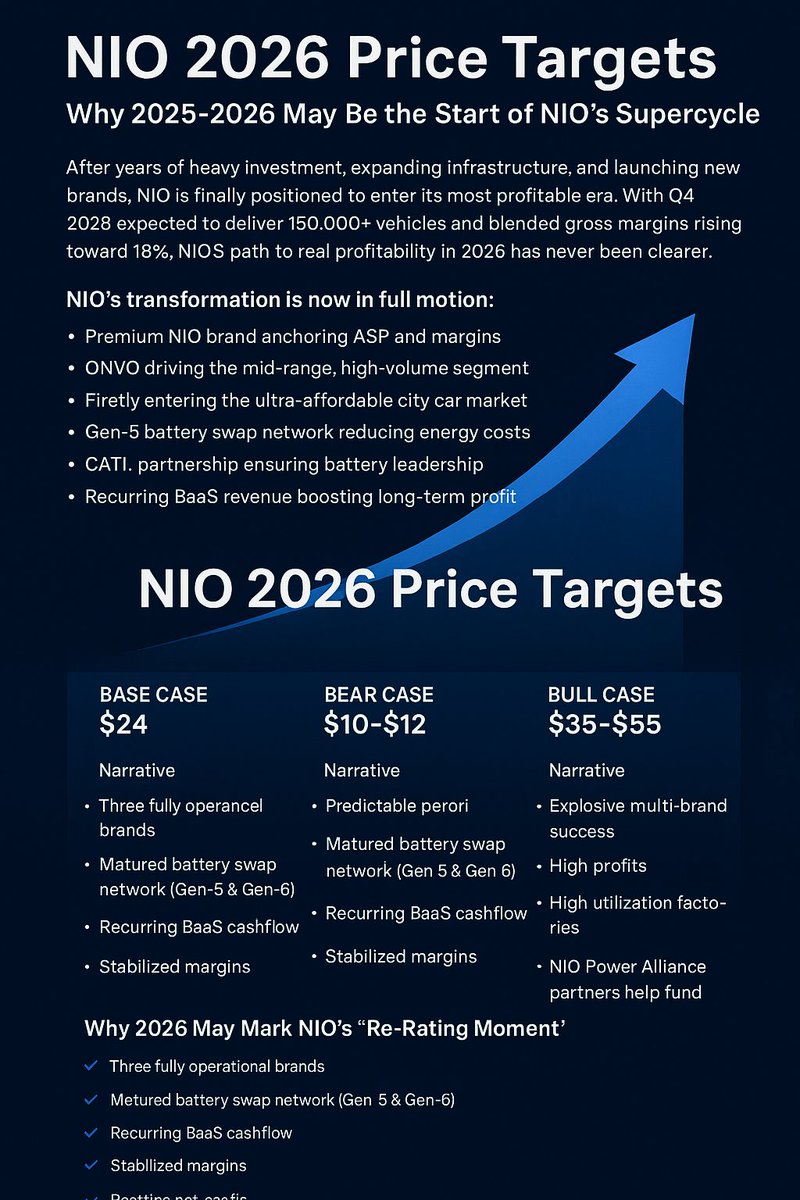

$NIO 2026 Price Targets: Why 2025–2026 May Be the Start of #NIO Supercycle

After years of heavy investment, expanding infrastructure, and launching new brands, NIO is finally positioned to enter its most profitable era. With Q4 2025 expected to deliver 150,000+ vehicles and blended gross margins rising toward 18%, NIO’s path to real profitability in 2026 has never been clearer.

NIO’s transformation is now in full motion:

-Premium NIO brand anchoring ASP and margins

-ONVO driving the mid-range, high-volume segment

-Firefly entering the ultra-affordable city car market

-Gen-5 battery swap network reducing energy costs

-CATL partnership ensuring battery leadership

-Recurring BaaS revenue boosting long-term profitability

-Together, these elements form the foundation for NIO’s 2026 re-rating.

NIO 2026 Price Targets (Base / Bear / Bull)

Below are realistic, data-driven scenarios for 2026 based on volume, revenue, margins, and profitability projections.

🟦 BASE CASE - $24 Price Target (Most Likely Scenario)

Assumptions:

2026 deliveries: 600,000 vehicles

Blended ASP: $43,000 (premium + ONVO + Firefly mix)

Revenue: ≈ $25–27B

Gross margin: 17–19%

Net profit: $1.4B – $1.8B

Forward P/E (high-growth EV sector): ~15×

Result: A $1.6B profit at a 15× multiple adds roughly $24B to market cap, implying a stock price between $22 and $24.

Narrative: 2026 becomes NIO’s first predictably profitable year. Margins stabilize, ONVO scales smoothly, Firefly performs strongly in Europe/Asia, and swap stations drive down energy costs. Wall Street shifts NIO into the “profitable growth” category rather than speculative EV.

🟥 BEAR CASE - $10–$12 Price Target (Low Probability Scenario)

Assumptions:

-2026 deliveries: 350,000–400,000

-Margin pressure from aggressive competition

-Slower-than-expected ONVO / Firefly ramp

-Weaker BaaS adoption

-Net profit: breakeven or slightly negative

Result: The market applies a depressed valuation due to limited profitability, producing a $10–$12 share price.

Narrative: Supply issues, macro headwinds, or geopolitical turbulence slow momentum. Even then, NIO’s brand strength and swap infrastructure still prevent a collapse—but a re-rating gets delayed.

🟩 BULL CASE — $38–$45 Price Target (High Potential Scenario)

Assumptions:

-2026 deliveries: 800,000+

-ONVO becomes a breakout volume winner

-Firefly dominates the European A-segment

-Premium NIO lineup maintains 20%+ margins

-BaaS delivers high-margin recurring revenue

-Net profit: $3.2B+

Forward P/E: 15–18× (Tesla + BYD blended multiples)

Result: $3.2B profit at 16× yields a ~$51B market cap, implying $38–$45 per share.

Narrative: All brands fire on all cylinders. Swap stations expand across China and Europe, CATL tech cuts battery costs further, and profitability surges. Institutions re-enter aggressively as NIO becomes the only Chinese EV maker with a full ecosystem moat.

Why 2026 May Mark NIO’s “Re-Rating Moment”

By 2026, NIO will have:

* Three fully operational brands

* Gen-5 & Gen-6 swap networks deployed

* Recurring BaaS subscription cashflow

* Stabilized, mature margins

* Profitable operations

* High factory utilization

* NIO Power Alliance partners funding many stations

* Global expansion (China, Europe, Middle East, Australia)

This is the moment NIO transitions from “promising EV startup” to “multi-brand global automaker.”

Final 2026 Price Targets Summary

In the Bear Scenario, NIO lands between $10 and $12 per share, driven by slower deliveries, margin pressure, and weak profitability—essentially a breakeven year.

In the Base Scenario, NIO reaches $22–$24, supported by strong deliveries, stable margins, and clear, consistent profitability throughout 2026.

In the Bull Scenario, NIO accelerates into $38–$55, powered by multi-brand success, strong global performance, high-volume ONVO adoption, and multi-billion-dollar net profit.

Bottom Line

With Q4 2025 about to become NIO’s first profitable quarter—and 2026 shaping up to be its first fully profitable year—NIO is entering a structural growth phase that the market has not priced in.

The combination of:

Vertical integration

Multi-brand strategy

Energy ecosystem

BaaS recurring revenue

CATL battery partnership

Swap infrastructure moat

…positions NIO as the only EV company with this level of synergy.

2026 could be the year the market finally re-rates NIO as a global leader, not just another electric automaker.

Disclaimer

This content is for informational and educational purposes only and does not constitute financial advice, investment guidance, or a recommendation to buy or sell any security. All price targets, forecasts, and scenarios are speculative in nature and based on publicly available information, assumptions, and forward-looking estimates that may change without notice. Actual results may differ significantly due to market conditions, geopolitical factors, competition, regulatory changes, and company performance.

Readers should conduct their own research or consult with a licensed financial advisor before making any investment decisions. The author and AI assistant assume no responsibility or liability for any actions taken based on this analysis.

English

Josef Vesely retweetledi

These 4 stocks are trading at a ridiculously low valuation.

These are absolutely no brainers IMO.

Solid growth, extremely profitable, absolutely disrespected by the market.

1. $NVO

14x forward P/E

2. $JD

10x P/E

3. $META

20x forward P/E

4. $PYPL

11.89x forward P/E

English

Josef Vesely retweetledi

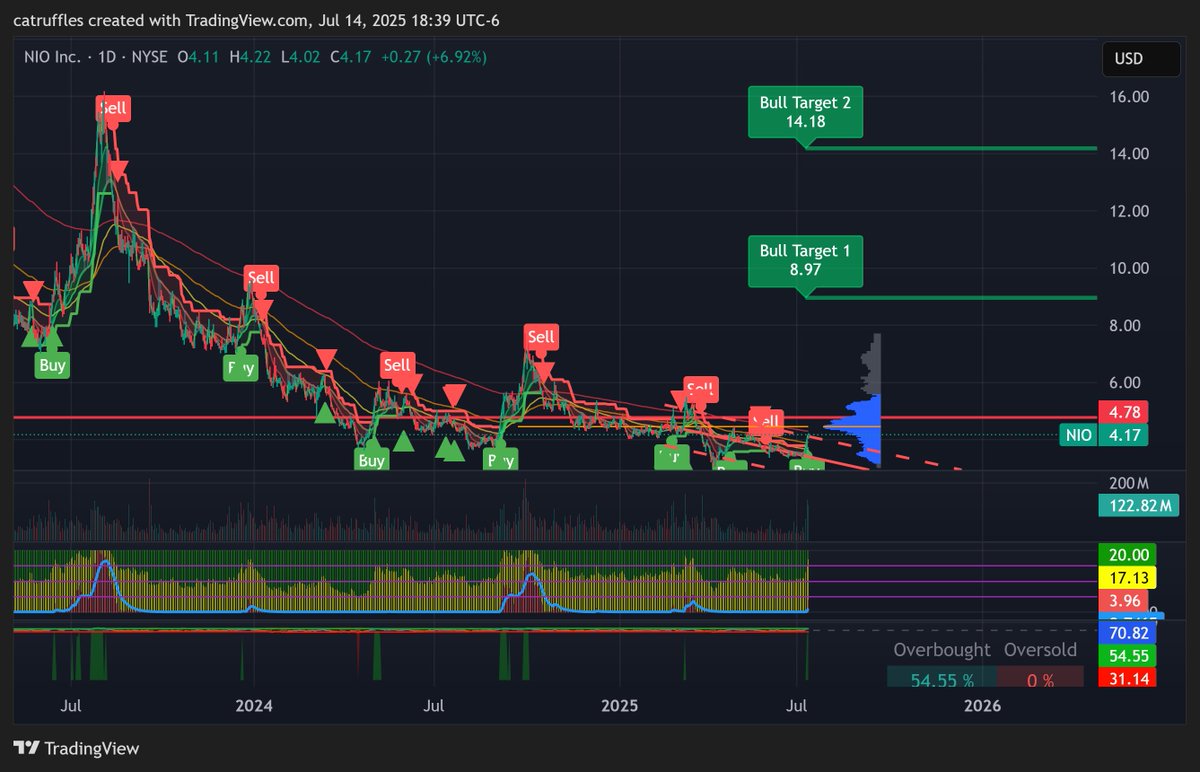

$NIO NIO

Daily Chart - Bullish Potential

PT 1 - $8.97

PT 2 - $14.18

Needs to break the weekly supertrend resistance at $4.78

English

Josef Vesely retweetledi

Josef Vesely retweetledi

@NIONenad Power swap stations are an important part of China's infrastructure plan for the next 10 years. NIO Power will be a goldmine. That is all.

English

Josef Vesely retweetledi

Josef Vesely retweetledi

Josef Vesely retweetledi

Josef Vesely retweetledi

'Tis the season! ❄️

Celebrate Christmas with #Binance for a chance to become 1/5 winners to share 0.5 #BTC!

To enter:

🔸 Retweet & follow @binance

🔸 Share your Binance-themed Christmas pics using #BinanceChristmas

10 runners-up will get rare #Binance merch, so get creative!

English

Josef Vesely retweetledi

1️⃣5️⃣

@Jiri_BJP is our fifteenth undisputed UFC light heavyweight champion and our first EVER Czech champ! 🇨🇿

English