pogi kr

11 posts

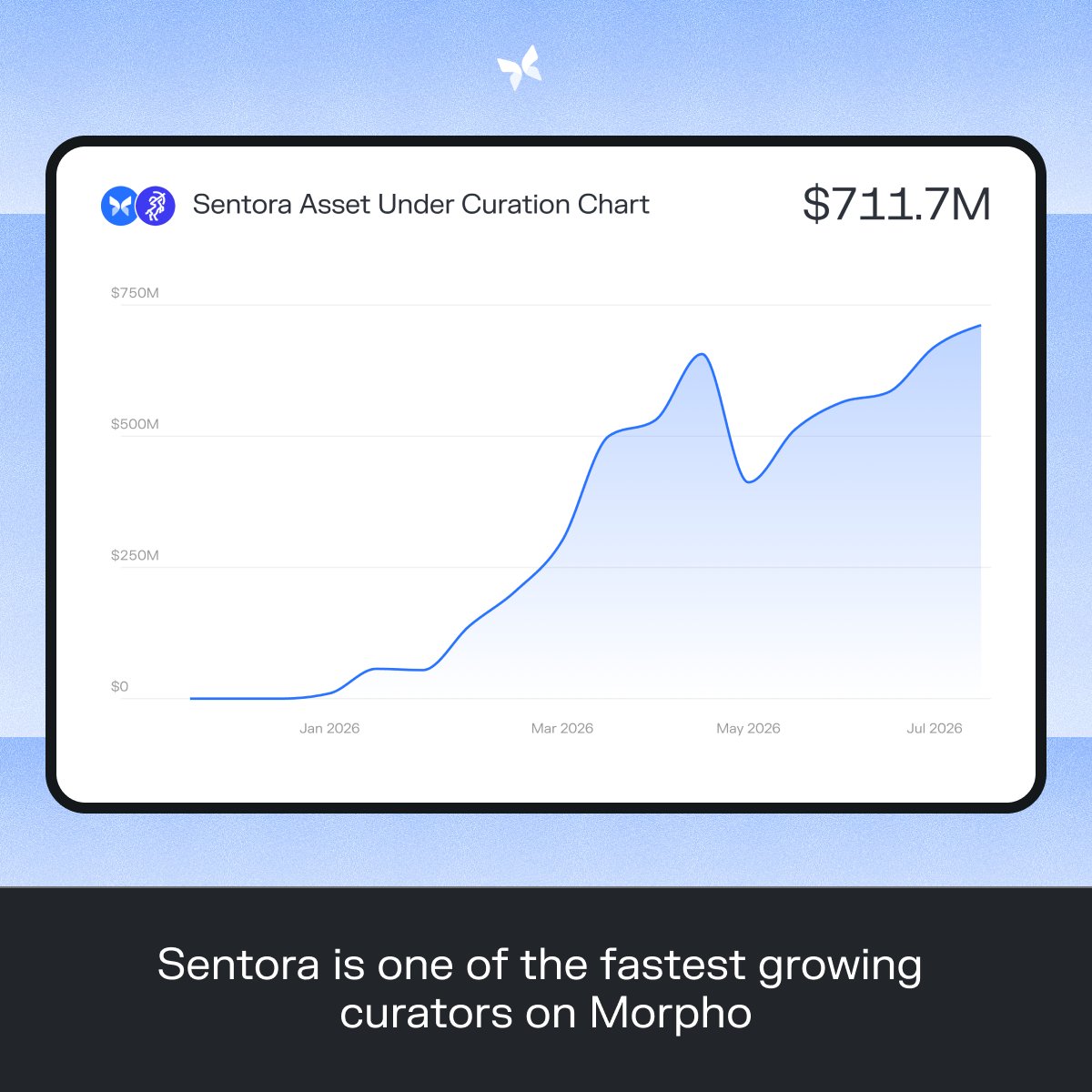

Learn how @SentoraHQ grew from 0 to $700M+ in assets under curation on Morpho in half a year.

Sentora's growth coincides with the growing demand from asset issuers like @paypal, @ripple, @hastra by @figure looking for distribution, either natively onchain or via leading fintechs like @krakenfx and @deel.

English

@0xAlphaping Currently, the curator on Delta vault is showing as disabled. Is there a problem? It's registered normally on-chain, but it's only missing from Morpho.

English

@Main_St_Finance Thank you for update, can you share the expected maturity breakdown of the remaining box positions (e.g. 30/60/90/180/300+ days)?

English

Main Street Update

We wanted to provide a further update on the remaining box positions, the minter, and the Morpho market.

The key point is that Main Street remains collateralized above 100% when valuing the remaining box positions at expiry. The boxes are expected to mature at $1, and our focus remains on liquidating them safely and efficiently as they move closer to expiry.

We are continuing to actively monitor the remaining boxes. As these positions get closer to expiry, pricing generally improves and we are able to exit more of them without taking unnecessary haircuts. Whenever boxes can be sold in a way that is accretive and does not harm overall backing, we will continue to do so.

As USDC is freed up, there will be two separate processes:

1. msY holders outside of Morpho

For msY holders outside of the Morpho market, USDC will continue to be added to the minter and used to support the pool. This allows users to continue exiting through the normal pool/minter process as liquidity is restored.

The minter will continue buying msY from the pool and redeeming/burning that supply over time. As more boxes are liquidated or mature, more USDC can be used to support this process, with the goal of continuing to reduce circulating msY supply outside of Morpho.

2. USDC lenders in the Morpho market

Morpho needs to be handled separately because of the way Morpho v1.1 works under extreme utilization.

Some looped borrowers are now accruing interest at very high rates. Over time, this can cause their debt to become larger than the value of their msY collateral, even when valuing msY at $1. This creates a technical bad debt issue inside the Morpho vault.

It is important to be very clear: users who lent $1 of USDC into Morpho should receive $1 of USDC back. The issue is not around the original principal that was lent into the market. The issue is the excess interest that has accrued on top due to extreme utilization.

That excess interest will effectively need to be sacrificed and remain as bad debt within the vault. This does not mean that lenders lose the dollar they originally lent. It means that the additional interest above principal cannot be safely paid out without creating unfair outcomes elsewhere.

Because of this, the msY collateral currently inside the Morpho market will effectively remain there and be treated as written off from the rest of the system. The portion of backing associated with that msY will instead be allocated to USDC lenders in the Morpho market through a dedicated claim process.

In practice, this means:

msY outside of Morpho will continue to be bought through the pool/minter and redeemed over time.

The circulating msY supply outside of Morpho will continue to be reduced as USDC becomes available.

The msY left inside the Morpho market will remain there as the residual written-off supply.

Morpho lenders will receive a separate USDC claim corresponding to the principal they originally lent.

Once the remaining boxes have either expired or been liquidated, and the final amount of available USDC is known, we will create a dedicated claim contract for Morpho lenders. This ensures the process is based on final confirmed numbers and avoids creating unfair outcomes between different groups of users.

The end state is designed to be clean: msY outside of Morpho is bought and redeemed through the minter until that circulating supply is reduced down, while the only remaining msY will be the written-off collateral inside the Morpho market. Morpho lenders will then claim USDC separately, and economically the system nets down as though the remaining redeemable msY supply has been reduced to zero.

We understand that this has been a stressful period, especially for users affected by the Morpho market. The team is working through this carefully and methodically to avoid rushed actions that could create worse outcomes.

The goal remains the same: continue liquidating boxes efficiently, restore liquidity through the minter for msY holders outside of Morpho, and ensure that Morpho lenders are able to recover the USDC they originally lent.

We will continue to provide updates as more boxes are liquidated and as more USDC becomes available.

English

@0xAlphaping I hope team at least give us an update on how things are going on now. It's been over a week, after all.

English

Update:

Another $800k worth of Altura positions have been liquidated on HyperEVM today. 🔥

Super happy to see the progress on the Altura vaults moving swiftly.

Next week we expect some bigger moves on other vaults to happen. We will update you once it becomes factual.

English

@GabeWeide Could you explain the current situation? And shouldn't this have been blocked as well? Or shouldn't it have been posted officially on AlphaPing so everyone could see it?

English

@0xAlphaping Please share an update on the current situation. Also, why did you withdraw funds from AVLT/USDC and remove them from Delta Allocation? A withdrawal of at least 3M was made while the vault was closed; please explain.

English

@Main_St_Finance When is the update scheduled to be released? It’s been almost a week already. You should at least let us know that your team is currently working on it.

English

msY Portfolio & Redemption Update

We want to provide a clear update on the current msY portfolio, the remaining box-spread maturity profile, and the path forward for restoring liquidity to the minter.

As previously communicated, the msY box-spread strategy began approaching capacity in its original short-duration Deribit execution environment. In response, Main Street expanded execution across additional centralized venues and OTC box-spread counterparties in order to continue optimizing risk-adjusted yield for holders and avoid forcing new capital into increasingly compressed shorter-dated opportunities.

As part of that expansion, certain OTC box-spread opportunities were executed at longer maturities than the initial short-duration target range. Following the unwind of the shortest-dated and most liquid positions during the initial phase of the Morpho market squeeze, the remaining portfolio now consists of boxes with approximately 60 to 340 days remaining to expiry. The remaining book is therefore naturally more concentrated in the medium-to-longer dated part of the maturity ladder, because the shortest-dated liquidity was used first to support the minter and reduce near-term pressure.

Importantly, this does not change the core economics of the strategy. These are fixed-payoff box-spread positions. If held to expiry, and assuming the relevant venue or counterparty performs, the positions accrete toward their known maturity value. The current situation is therefore primarily one of timing, secondary-market liquidity, and redemption pacing; not a change in the expected terminal payoff of the portfolio.

Current portfolio position:

Current CR, assuming boxes are held to expiry: 100.04%

Insurance fund: $525,527 in msUSD

Insurance fund treatment: if required, the msUSD held in the insurance fund can be burned, increasing protocol coverage

Coverage including the insurance fund: above 100%

Our priority is to preserve full backing and avoid crystallizing unnecessary losses. We are actively exploring opportunities to unwind or sell selected boxes where executable pricing is available and where, after taking into account the insurance fund and any applicable protection mechanisms, the system remains above 100% coverage. Where that threshold can be met, we intend to take those opportunities and use the proceeds to continue refilling the minter.

We do not expect that every remaining box necessarily needs to be held all the way to expiry. As boxes move closer to maturity, the discount between secondary-market pricing and maturity value should naturally compress, which can create further opportunities to exit closer to NAV without impairing coverage. This means liquidity can be restored progressively through a combination of scheduled expiries and selective secondary-market unwinds where pricing is acceptable.

Where secondary liquidity is not available on acceptable terms, we will continue following the approach outlined in our risk framework: allow box positions to mature, release liquidity as expiries occur, and refill the minter as capital becomes available.

Selling fixed-payoff positions at distressed marks simply to accelerate liquidity would be value-destructive for holders. Waiting for better execution, selectively unwinding where coverage remains above 100%, and using the insurance fund as intended gives the protocol the strongest path to preserve backing and restore liquidity in an orderly way.

This is a timing and execution-management issue, and the portfolio remains structured around fixed-payoff positions that accrete toward maturity value. We are confident in the path forward and will continue to provide updates as liquidity is released, boxes are unwound, and the minter is refilled.

Our focus remains unchanged: preserve NAV, protect holders, avoid uneconomic liquidations, maintain coverage, and work through the maturity ladder in the most responsible way possible.

English

@0xAlphaping Withdrawals are currently continue from the AVLT/USDmarket. Given that no liquidity is being supplied to the Alpha USDC Delta vault, is it appropriate to keep withdrawing funds like this? I’m one of the most funds locked in person right now, yet I haven’t received any reponse.

English

Treasury Unwind Update

The Inessa unwind is underway, and transfers to Altura's bank account are now being processed through JPMorgan Chase.

We have added a new Proof of Reserves tab to the Altura app, where every transfer can be followed: app.altura.trade/proof-of-reser…

As funds arrive, Inessa exposure decreases and Altura bank account exposure increases. The Altura POR dashboard reflects these changes immediately. Each transfer is also independently verified by Accountable, and their dashboard may take slightly longer to update, as reconciliation is done manually on their side.

We are scaling transfer sizes up gradually so each step clears cleanly through the banking and verification process. Today's transfers reflect that approach, and amounts are expected to increase over the coming days.

As previously stated, redemptions will open once all treasury assets have been recovered and verified, and will then be processed together, so everyone is treated equally.

For those borrowing against AVLT on Morpho, we understand this is a difficult position. To keep the process fair for all holders, redemptions are handled together rather than individually. Morpho's markets are also immutable, so the terms cannot be changed on-chain by anyone. Your position stays in your control, and you can repay and unwind on Morpho at any time.

We are grateful for the patience and trust this community continues to show, and we will keep sharing progress until the unwind is complete.

English

@0xAlphaping Currently, over 700k in funds are being held in Delta, Im open for a reasonable exit over time, Would it be possible to discuss this matter?

English

@0xAlphaping It appears that funds are continuing to be withdrawn from some wallets and it seems that only some users are able to make withdrawals at this time. Currently, over 700k in funds are being held, Im open for a reasonable exit over time, please assist me if you can.

English

Market participants have begun unwinding positions in the Alpha USDT Vault, driven by expectations of a positive outcome for the AVTL claim following Altura’s announcement of larger repayments from Inessa today.

陈小萌@MengLayer

另一个 $AVLT 神秘大哥出手了 ! 刚刚主动上手清算了 54W $AVLT ,大哥可能觉得二级买的太慢了,干脆直接清算LOOPER仓位~ 目前大哥手里有120W AVLT 这么看已经有不少人押注 AVLT 可以完成unwind 全额退款了,清算说明 Looper们有救了!

English