@glcarlstrom @BenjySarlin Isn’t he just listing off the “three” violations? Violation #1, #2, #3? I don’t think he was actually numbering the clauses in his post.

English

Kyle Davidson

9.4K posts

@kylejdavidson

Wreck it buy a new one.

🚨 BREAKING

Trump on Greenland: If we do not do it the easy way, we will do it the hard way. By the way, I am a fan of Denmark. The fact they had a boat land there 500 years ago does not mean they own the land. We will be doing something with Greenland—the nice way, or the more difficult way

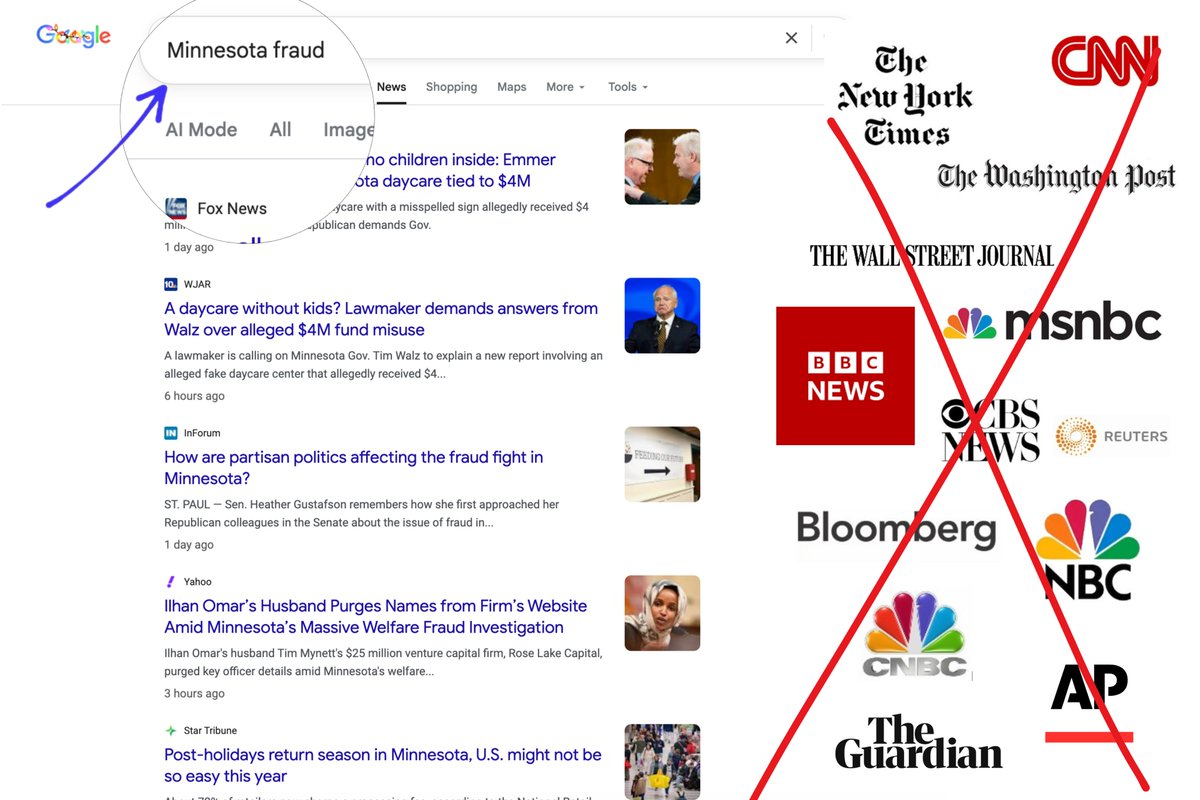

🚨 Here is the full 42 minutes of my crew and I exposing Minnesota fraud, this might be my most important work yet. We uncovered over $110,000,000 in ONE day. Like it and share it around like wildfire! Its time to hold these corrupt politicians and fraudsters accountable We ALL work way too hard and pay too much in taxes for this to be happening, the fraud must be stopped.