@theficouple Its not all about the time spent on the house...it does matter, but more over its having a safe, comfortable place to just be...

English

landager.com

101 posts

@landagerAI

Property management made simple for independent landlords. AI-powered tools to track tenants, rent, maintenance and more. Try Landager for free.

If you’ve ever been to Norway you’d realize it’s a very lovely place but the people live very utilitarian lives and there is nowhere near the quality of life you find in the US. It’s a nice, basic place to live with no urban turmoil, an homogeneous culture and not a lot of sunlight…

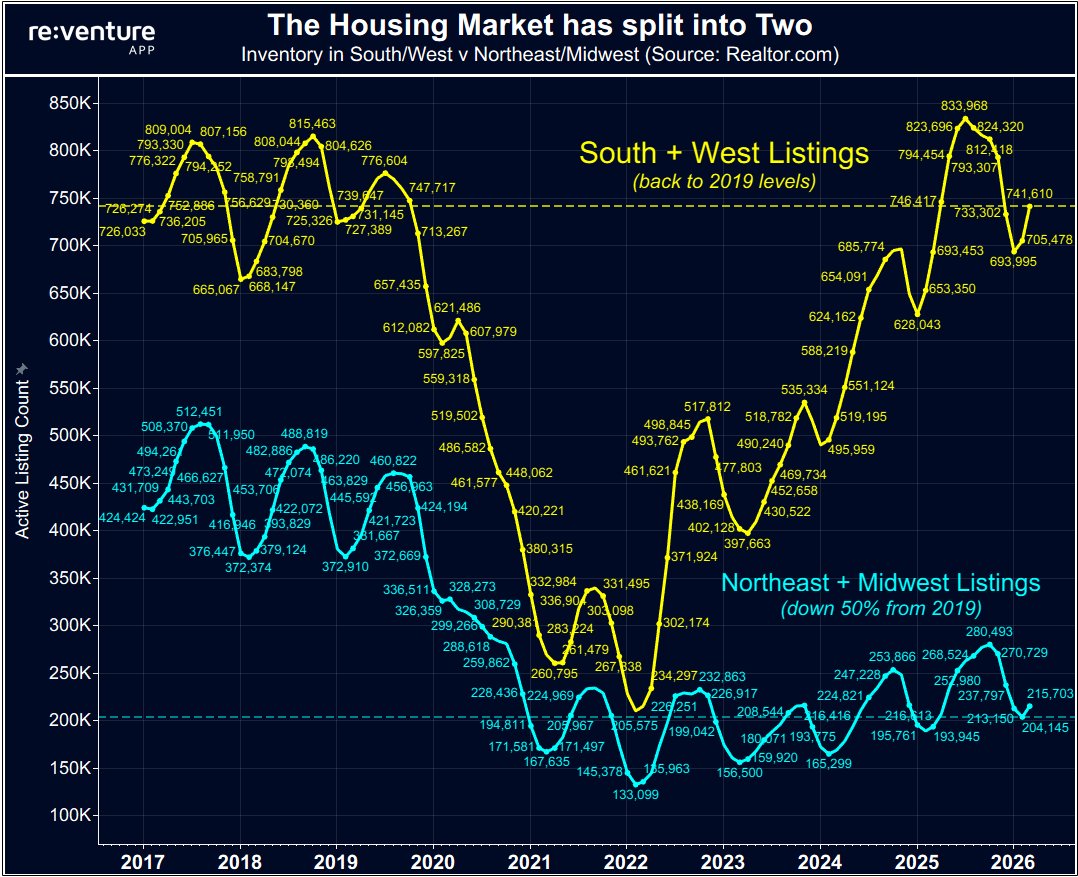

Average rents have gone from $1530 to $1300 in DFW. Probably lower through the year and maybe next year, but should rebound thereafter. There’s opportunity in the window.

Ireland's personal taxation regime is the second worst among 38 peer countries according to the Tax Foundation. High marginal taxes (paid at very modest thresholds) have been in place since 2008. There has been almost no improvement over two decades despite having the resources to do so - a relentless rise in government expenditure has been prioritised year after year. A simple example illustrates how bad it is. The average electrician or plumber working for construction company will be on the top marginal rate, whereby the state takes more of every additional euro than the person gets to keep. If he/she wants to earn self employed income, the government will take more than the worker, and a tax return will have to be filed, involving time and/or accountancy fees. Is it any wonder finding tradespeople is hard?

Oil at $150 would trigger global recession, per Fink of BlackRock.

My experience has been the opposite. Bought our first home in 2009 for $196K. Sold it in 2017 for $300K. At the time I had paid that mortgage down to $120K. So you do the math but I got a check for $180K when we sold our house in 2017. And that house provided a great place for my family to live for 8+ years. Pretty great deal.

% of London properties resold at a loss in 2025: Flats: 17.9% Terraced: 2.8% Detached: 3.0% Semi-detached: 2.2% Roughly 1 in 5 flats vs 1 in 40 houses. Source: HM Land Registry, 22,000+ London resales analysed

California is going bankrupt before our eyes.

Remember when those idiots at UCLA published the paper showing that taxing away 5% of the gross sale proceeds of every piece of real estate in LA >$5MM wouldn't impact housing production?

Pensioners tea party