Sabitlenmiş Tweet

Lavin Mirchandani | GetEvangelized

12.8K posts

Lavin Mirchandani | GetEvangelized

@LavinM

founder @GetEvangelized I Share your story via KOL engagement, Founder branding & YouTube growth | Founder Coach for Zero to One GTM

Mumbai Katılım Kasım 2008

2.4K Takip Edilen4.6K Takipçiler

"Do seeti ke baad cooker band kar dena!"

Harsh Goenka@hvgoenka

AI based cooker now in our country…..

हिन्दी

Lavin Mirchandani | GetEvangelized retweetledi

I just minted DEATH TOUCH ALPHA SEASON 1 PASS from @Deadfellaz

You can still get in on this OG Bluechip project from circa '21. the founders keep grinding and keep building value for the holders AND they believe that airdrops should just be "dropped" not any other way.

LFG!

Deadfellaz@Deadfellaz

Announcing S1 pass mint for Death Touch TCG - @deadfellaz fast-paced, post apocalyptic card battler. We are taking a web3 ‘patreon/kickstarter’ approach to development, bringing our community along for the ride at every stage. Mint your S1 pass for .01eth (500 passes available only) and receive exclusive drops, voting rights, and more. Each season is 30 days, all existing packs, vaults, and cards will break and be playable in game at the end of season 3. Mint and get more info: deathtouchtcg.com/seasonpass.html

English

Infact zerodha "nudges" you to not trade where things are risky, struggling to shortlist an alt broker for the satelite port.

Nithin Kamath@Nithin0dha

❤️

English

This team keeps building, inspiring and the mojo up for the class of '21

Looking forward to celebrating the summer and much more @betty_nft @psych_nft 🚀

English

@betty_nft @Deadfellaz That last line is just 💯

English

Gonna start posting Horde History lessons every day until @Deadfellaz is in its rightful place because there just isn’t an OG collection more undervalued in this moment and it cannot stand.

English

@sainik636 @Crazynaval the hosts missed inviting you to this party ;-)

English

Is PPFAS going the RAJESH KHANNA WAY ??

Rajesh Khanna was the Original Superstar. Right from his debut in 1966, he was a successful star.

He was like a Breath of Fresh Air, very different in Style & Mannerisms from the previous era heroes.

He attained Superstardom with Aradhana in 1969 & went on to rule the screen for the next 4–5 years.

After the mid-70s, his films began to flop, though he continued acting with a sprinkling of hits over the three decades.

But he never regained the cult status of his first decade.

When I met him in 1987, he still looked like a Greek God; was still charismatic; had a strong cult following, but his films were just not working.

The reasons were clear:

1. Choice of scripts: Rejected Zanjeer; Deewar; Amanush; Parvarish;Seeta Aur Geeta Mr. India etc

2. Holding on to his "romantic" image & not changing with the times

3. Rigidity in approach & style, justifying his actions even though it was backfiring

4. Depending on his erstwhile cult to flock to theatres

PPFAS started in 2013 & was like a Breath of Fresh Air in the murky world of mutual funds

1. Great pedigree

2. Unique style & approach

3. Caught the boom in MF investing & attained superstardom in the first decade

NOW is the crunch time:

They are the best-performing MF over the past decade

However, they are not even in the top 10 over the last 5 years

They have been fighting for the 20th place over the past 3 years

Last year, they delivered negative returns even though they diversified into US equities, which they wear as a badge of honor

So what gives ??

1. Their choice of scrips: They are a Flexi-cap fund & benchmarked to CNX 500, which has a weightage of 70% to large caps, 20% to midcaps & 10% to small caps, yet their fund is focused on large caps to the extent of nearly 90–95%

2. Holding significant cash (more than 20%) during the last 3 years

3. Rigidity in approach & style, preferring large caps whenever they invested incrementally & in Large Caps which were erstwhile heroes, e.g., ITC; HDFC Bank; TCS, even though the strategy was backfiring & shunning opportunities when there were bargains in stellar Midcaps & Small Caps in the recent correction.

4. Hoping the cult-like status will help them garner AUMs, even though they do not effectively deploy into equity, which is their primary purpose.

When I was an MFD, the first & only MF I ever recommended was PPFAS, since the late Parag Parikh was my icon.

I was a fan of Rajesh Khanna & hoped that he would change his ways sooner or later, but sadly that did not happen.

I hope I am not disappointed a second time around.

@PPFAS @ppfasmf @latha_venkatesh @dugalira @_prashantnair @Iamsamirarora @nagappanv @sahneydeepak @Moneylifers @TheMFGuy1 @BaluGorade @datta_arvind @BeatTheStreet10 @ActusDei @ayushagarwal @contrarianEPS @ChanderBhatia01 @riteshmjn @AdityaD_Shah @jitenkparmar @_KiranRajput

English

Lavin Mirchandani | GetEvangelized retweetledi

The Colourful Truth of Sugary Soft Drinks in India. Love the way this bro explains to kids.

Infact No Human deserves to Consume this.

FSSAI team - For your kind information.

This video needs to go Viral.

#FI

English

@betty_nft @Deadfellaz Welcome Zach

It’s going to be an interesting ride from here ✌️

English

Founders who don’t fold, fade.

For every founder that raises capital, for every business that hits a major liquidity event, there are many more founders and businesses that don’t get to a logical end.

They neither fold, nor do they exit with a liquidation event; sometimes it’s a pivot with the same name or they move on but retain the brand name until it slowly sunsets.

What they have built over years with sweat, passion, personal capital and all their heart sticks on to them as an identity; until they discover their next calling. Very often this next calling is the same old wine packaged in a new bottle- even if it had a 400Cr exit, for that became an itch that wasn’t fully scratched.

Unscratched itches and unresolved identities are common traits you will find in such entrepreneurs; if you do come across one and have the intent to support, do give them a hug, some acknowledgment and ignite a conversation to help accept closure. For what they will build next, after being unleashed, is likely to be a blockbuster- and you may feature somewhere in the credits.

English

Start a new Faceless YouTube Channel now! April 2026: Get monetized. And earn your first $10,000 by June 2026.

Usually, I charge $89 for this guide, but today I'm giving it away for FREE.

Like + Reply 'YT' & I'll send you my guide for FREE.

Must follow me to get DM.

FREE for 48 hrs

English

Many such concepts are lost in translation. Good to see such educational content being created lest our generation and ones to come are anyway being whitewashed.

Also read up on “Adaan-pradaan” in similar context.

Aviator Anil Chopra@Chopsyturvey

Very interesting #Kanyadan

English

Lavin Mirchandani | GetEvangelized retweetledi

Absolutely no AI was used in creating this.

You will enjoy this reaction from Bollywood 🤣

English

Lavin Mirchandani | GetEvangelized retweetledi

No complexity. No accident.

10/10 was caused by irresponsible marketing campaigns by certain companies.

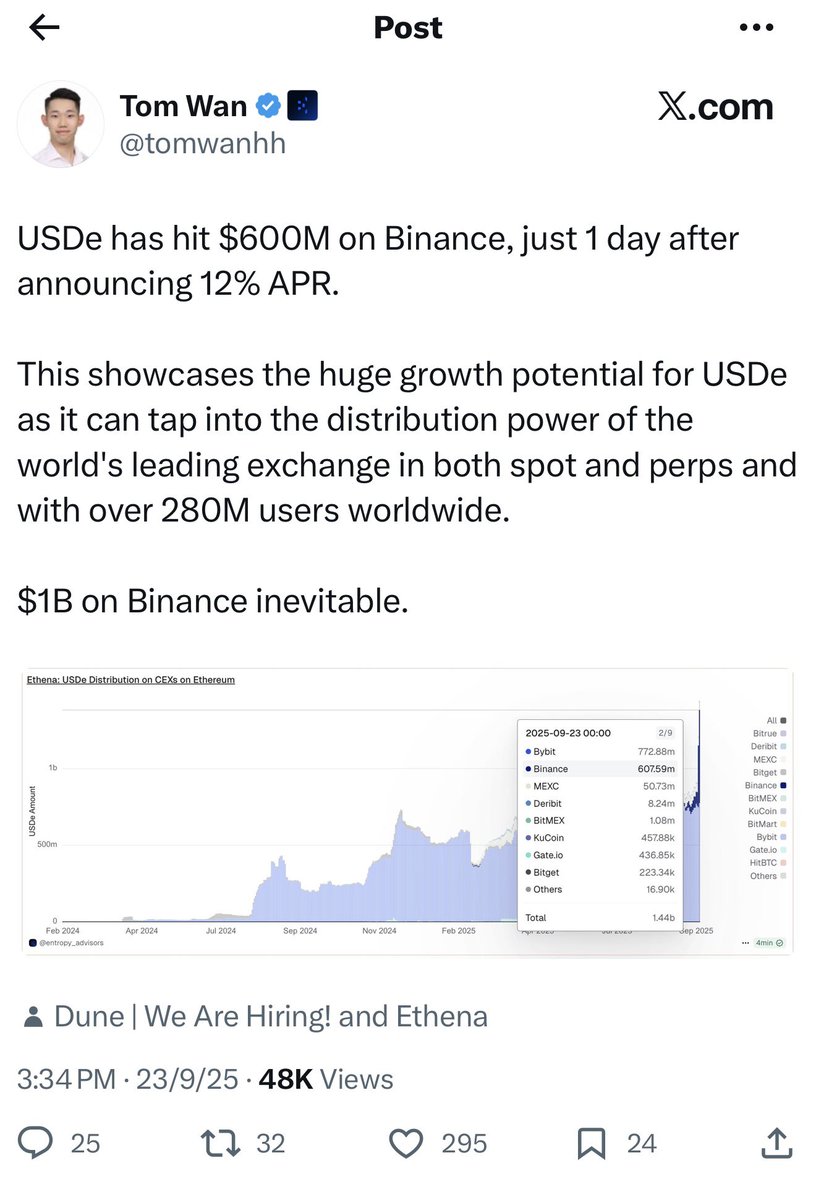

On October 10, tens of billions of dollars were liquidated. As CEO of OKX, we observed clearly that the crypto market’s microstructure fundamentally changed after that day.

Many industry participants believe the damage was more severe than the FTX collapse. Since then, there has been extensive discussion about why it happened and how to prevent a recurrence. The root causes are not difficult to identify.

⸻

What actually happened

1.Binance launched a temporary user-acquisition campaign offering 12% APY on USDe, while allowing USDe to be used as collateral with the same treatment as USDT and USDC, and without effective limits.

2.USDe is a tokenized hedge fund product.

Ethena raises capital via a so-called “stablecoin,” deploys it into index arbitrage and algorithmic trading strategies, and tokenizes the resulting fund. The token can then be deposited on exchanges to earn yield.

3.USDe is fundamentally different from products such as

BlackRock BUIDL and Franklin Templeton BENJI, which are tokenized money market funds with low-risk profiles.

USDe, by contrast, embeds hedge-fund-level risk. This difference is structural, not cosmetic.

4.Binance users were encouraged to convert USDT and USDC into USDe to earn attractive yields, without sufficient emphasis on the underlying risks. From a user’s perspective, trading with USDe appeared no different from trading with traditional stablecoins—while the actual risk profile was materially higher.

5.Risk escalated further as users:

•converted USDT/USDC into USDe,

•used USDe as collateral to borrow USDT,

•converted the borrowed USDT back into USDe,

•and repeated the cycle.

This leverage loop produced artificial APYs of 24%, 36%, and even 70%+, widely perceived as “low risk” simply because they were offered by a major platform. Systemic risk accumulated rapidly across the global crypto market.

6.At that point, even a small market shock was sufficient to trigger a collapse.

When volatility hit, USDe depegged quickly. Cascading liquidations followed, and weaknesses in risk management around assets such as WETH and BNSOL further amplified the crash. Some tokens briefly traded near zero.

The damage to global users and companies—including OKX customers—was severe, and recovery will take time.

⸻

Why this matters

I am discussing the root cause, not assigning blame or launching an attack on Binance. Speaking openly about systemic risks is sometimes uncomfortable, but it is necessary if the industry is to mature responsibly.

I expect there may be significant misinformation and coordinated FUD directed at OKX in the near future. Even so, speaking honestly about systemic risk is the right thing to do—and we will continue to do so.

As the largest global platform, Binance has outsized influence—and corresponding responsibility—as an industry leader. Long-term trust in crypto cannot be built on short-term yield games, excessive leverage, or marketing practices that obscure risk.

The industry needs leaders who prioritize market stability, transparency, and responsible innovation—not a winner-take-all mentality where criticism is treated as hostility.

Crypto is still early.

What we choose to normalize today will determine whether this industry earns lasting trust—or repeats the same mistakes again.

English

Lavin Mirchandani | GetEvangelized retweetledi

@hmalviya9 Pls elaborate how did you arrive at this conclusion or did you miss adding </sarcasm> 😉

English

Lavin Mirchandani | GetEvangelized retweetledi

Join us for this chat where we discuss farming, alpha, product,macros & more with the founding team. Set your reminder and RT for good karma 🙏

Pacifica@pacifica_fi

Pacifica India AMA is here! Join our Spaces on January 15th at 10PM SGT / 2PM UTC / 9AM EST 🗣 This week’s guest: 🎙 @NamasteWeb3 Set your reminders, you won’t want to miss this! 🌊 x.com/i/spaces/1mrGm…

English