ledrio

49 posts

@ledrioi @Longterms1 Många blankare som låg snett innan detta citat också: "Intellego Technologies’ CEO has been arrested on suspicion of gross fraud".

Svenska

Sivers kund $poet kanske inte är så bra trots allt? Nedan påminner kanske också lite om beskrivningen EFN gav efter deras besök hos Sivers. Men framtiden för sig har dom ju säkert iallafall, AI och allt.

Night Market Research@NMRtweet

We visited $POET's HQ building in Toronto. We found abandoned rooms and none of the tenants on the same floor recognized POET.

Svenska

@Longterms1 Respekterar din conviction. Men antar att du legat jäkligt fel med din korta position som du tog för någon vecka sen 🥶

Svenska

ledrio retweetledi

$SIVE is now aiming to become the next $LITE, a US photonics giant.

They're re-centering their board around US executives + US photonics.

So the core board are now: US $GFS Executives and $CITI Executives, with the company run by UC Berkeley grads and $LITE executives.

The 3 members leaving were local Swedish/EU.

This is just a shift in strategy from focusing on developing local Swedish Semi environments:

To dominating the US/global photonics market. I'm not trying to discredit their service/background.

But in my view to focus around US/global photonics markets, it's likely optimal to have more US executives.

But they should all be proud for helping make $SIVE what it is today.

Selo@Selooo79

@aleabitoreddit Any thoughts on the board members leaving $SIVE ?

English

Gapwaves är ett av mina äldsta innehav och ett av dom större.

Det har legat långt ner i byrålådan länge, kul om dom kan få lite uppmärksamhet 💪

#Gapwaves $GAPWB

#prataaktier #finanstwitter #fintwit #fintwitt

Pep Invest@PepInvestStocks

The next $SIVE - Gapwaves AB $GAPWB occupies a strategic position in the automotive radar value chain as a Tier 2 supplier of proprietary multi-layer waveguide (MLW) antenna technology, delivering compact, cost-efficient, and high-performance solutions optimized for mmWave radar sensors essential to advanced driver assistance systems and fully autonomous vehicles. Its unique waveguide designs minimize signal loss and enable superior resolution, making the technology highly attractive for next-generation imaging radar required in Level 2+ to Level 3 autonomy and beyond. The company’s potential is anchored in its expanding partnerships with leading Tier 1 suppliers including Bosch, Valeo, HELLA, Continental, $NXPI (as a Gold Partner), Infineon Technologies, and Smartmicro, as well as direct integration into major OEM platforms such as the Mercedes-Benz CLA, where Gapwaves’ waveguide antennas are already deployed on Swedish roads. Strategic collaborations extend into the broader ecosystem with confirmed involvement in projects for $AMZN Zoox robotaxis and last-mile logistics, $GOOG Waymo’s high-resolution radar systems, and series production support for $GM via partners like HELLA. A recent Vinnova-funded initiative with Waymo further accelerates development of MLW technology tailored for fully autonomous vehicles, underscoring Gapwaves’ role in enabling scalable, safety-critical radar performance. Additional tailwinds include growing demand for high-bandwidth connectivity in 5G/6G infrastructure serving hyperscalers such as $META and $MSFT, as well as robust distributor networks and an experienced leadership team with deep automotive expertise, including CFO Nils Mösko’s background at Ford, Volvo Cars, and Polestar. With proven industrialization of its antenna technology, strong insider alignment, and clear pathways to volume production across passenger cars, robotaxis, and commercial applications, Gapwaves $GAPWB is exceptionally well positioned to capture significant share in the rapidly expanding global market for autonomous driving sensors.

Svenska

ledrio retweetledi

Just to add to the very positive $SIVE news amid MSCI likely tens of millions of inflow in 2 weeks:

$AMZN has a new private placement with AlChip.

Probably implying design wins with future Trainium.

If you don’t remember… AlChip was Ayar’s lead customer. And $SIVE is the primary laser supplier to Ayar.

So implications for $SIVE, is enormous piggybacking off of Amazon’s ecosystem growth.

Serenity@aleabitoreddit

$SIVE 2025 annual report analysis. TLDR: Extremely Bullish. Sivers main growth vector is CPO, but they've TAM expansioned to pluggable transcivers + multiple new qualifications/development. 1. "We are currently seeing great interest... testing our DFB lasers across multiple manufacturers in pluggable transceivers" For pluggable angle, we've seen this with $JBL 1.6T LRO already, but annual report hinted they're developing/qualifying with more hyperscaler suppliers. "Our serviceable markets have now been expanded to include pluggable optical interconnects as well as scale-up and scale-out architectures for co-packaged" (TAM expansion) 2. "Discussions with hyperscalers and pluggable transceiver suppliers indicate a shortage of CW lasers in the coming years" $LITE already signaled CW laser bottlenecks, and they had to buy externally from competitors. So we kinda guessed CW Laser was a bottleneck. And this confirmed it, so was wondering about Win semi. "The partnership announced with high-volume supplier Win Semiconductor in March 2025 now gives us a strong position to meet growing demand" $SIVE likely has capacity locked in with Win from this nuance, which is exactly what I wanted to know. This positions Sivers in the CW laser as both a bottleneck and CPO laser architectural leader. VOLUME PRODUCTION H2 INDICATIONS (BULLISH): 3. "The collaboration positions both companies to address the rapidly growing market for optical AI connectivity, with prototypes to be demonstrated to customers during the first half of 2026 and with the goal of scaling up production by the end of 2026" H1 is more preproduction, H2 production signaled starting with names like $POET. 4. "We are pleased that our largest LIDAR customer will increase production starting in the fourth quarter of 2026" $AEVA start of volume production Q4 with $SIVE = bullish for both. Revenue floor from LIDAR as their CPO scales. 5. Sivers announced a partnership with LIGHTIUM AG to integrate their CW lasers directly onto TFLN wafers. 3.2T+ cycle. (future proofing) FYI no decent investor cares about last year's 2025 financials from development contracts aside from Swedish Media/Locals. Especially when you're forward looking for the 2027-2028 CPO supercycle. But the hint from you can take away from financials + geography that is $NOK is now the high confidence customer of $SIVE. TLDR: -> Win Semi implied capacity lock in during CW laser bottleneck -> Hints of new group of hyperscaler suppliers testing/qualification for pluggable transcivers, which is massive TAM expansion. -> New customers for CW lasers -> Volume production scaling starting H2 for both photonics and lidar.

English

@AbcpokerBI Känns som du ligger rätt snett i en kort position eller lite avis på att du missat tåget 😁

Svenska

ledrio retweetledi

$SIVE 2025 annual report analysis.

TLDR: Extremely Bullish.

Sivers main growth vector is CPO, but they've TAM expansioned to pluggable transcivers + multiple new qualifications/development.

1. "We are currently seeing great interest... testing our DFB lasers across multiple manufacturers in pluggable transceivers"

For pluggable angle, we've seen this with $JBL 1.6T LRO already, but annual report hinted they're developing/qualifying with more hyperscaler suppliers.

"Our serviceable markets have now been expanded to include pluggable optical interconnects as well as scale-up and scale-out architectures for co-packaged" (TAM expansion)

2. "Discussions with hyperscalers and pluggable transceiver suppliers indicate a shortage of CW lasers in the coming years"

$LITE already signaled CW laser bottlenecks, and they had to buy externally from competitors. So we kinda guessed CW Laser was a bottleneck.

And this confirmed it, so was wondering about Win semi.

"The partnership announced with high-volume supplier Win Semiconductor in March 2025 now gives us a strong position to meet growing demand"

$SIVE likely has capacity locked in with Win from this nuance, which is exactly what I wanted to know.

This positions Sivers in the CW laser as both a bottleneck and CPO laser architectural leader.

VOLUME PRODUCTION H2 INDICATIONS (BULLISH):

3. "The collaboration positions both companies to address the rapidly growing market for optical AI connectivity, with prototypes to be demonstrated to customers during the first half of 2026 and with the goal of scaling up production by the end of 2026"

H1 is more preproduction, H2 production signaled starting with names like $POET.

4. "We are pleased that our largest LIDAR customer will increase production starting in the fourth quarter of 2026"

$AEVA start of volume production Q4 with $SIVE = bullish for both.

Revenue floor from LIDAR as their CPO scales.

5. Sivers announced a partnership with LIGHTIUM AG to integrate their CW lasers directly onto TFLN wafers. 3.2T+ cycle. (future proofing)

FYI no decent investor cares about last year's 2025 financials from development contracts aside from Swedish Media/Locals.

Especially when you're forward looking for the 2027-2028 CPO supercycle.

But the hint from you can take away from financials + geography that is $NOK is now the high confidence customer of $SIVE.

TLDR:

-> Win Semi implied capacity lock in during CW laser bottleneck

-> Hints of new group of hyperscaler suppliers testing/qualification for pluggable transcivers, which is massive TAM expansion.

-> New customers for CW lasers

-> Volume production scaling starting H2 for both photonics and lidar.

English

ledrio retweetledi

Sivers just dropped their annual report for 2025, I'll dig into it and make another post later but here's a quick one..

$SIVE and $NOK? 👀

I've thought so for long and now I'm sure... Don't think there is another one possible in Finland?

English

ledrio retweetledi

I’ve followed $SIVE long enough to know that this has never been a simple story.

For years, the technology looked ahead of the market, while the stock was still priced like execution would never arrive.

But that gap may now be closing.

What makes the setup so interesting today is not just one contract, one customer, or one vertical. It’s the convergence of several major infrastructure trends at the same time: AI optics, CPO, pluggables, mmWave, SATCOM, LiDAR and defense.

That is where I think the market may still be too slow.

It is still valuing $SIVE like an early-stage promise, while the company may be moving into a phase where the operating leverage finally starts to show.

Deep Dive: 10 questions about $SIVE, and why I think the market may still be underestimating the setup 🧵

English

ledrio retweetledi

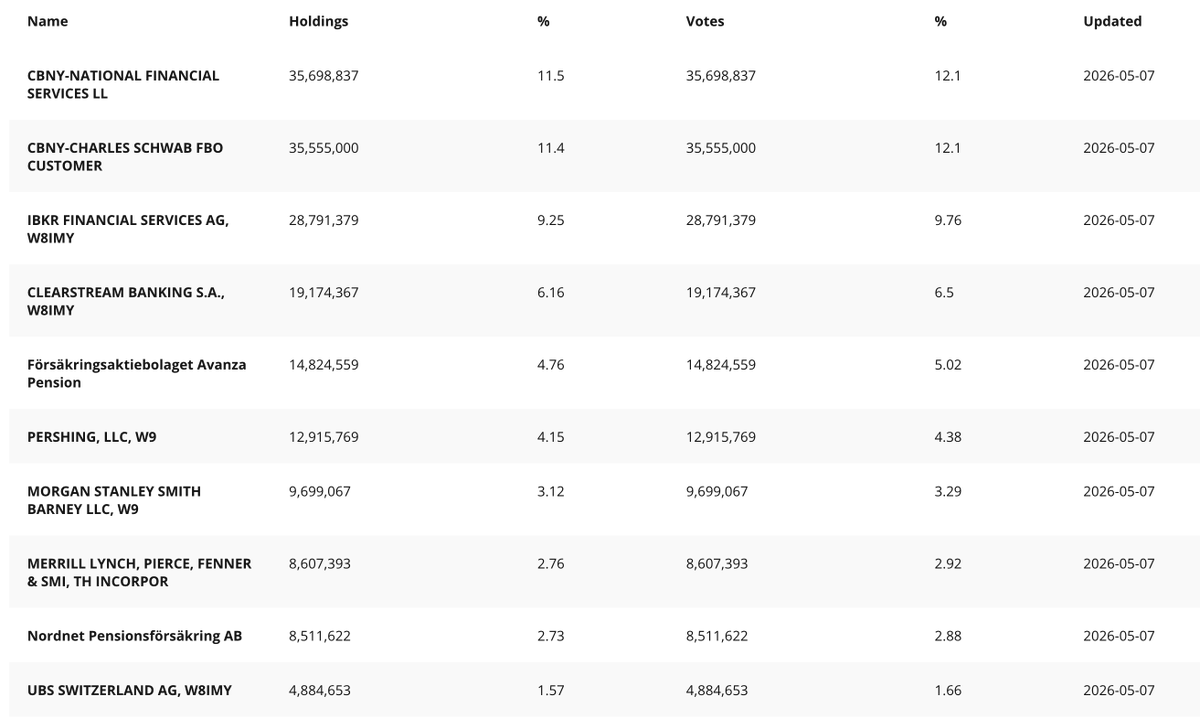

What did I say? $SIVE was undergoing a transfer of Swedish ownership over to the US...

If I'm interpreting things right from the new cap table.

The US / West now owns 42.18% of $SIVE:

~ $FNF (Fidelity) - 11.5% (US/West)

~ $SCHW (Schwab) - 11.4% (US/West)

~ $IBKR - 9.25% (US/International)

~ Pershing (BNY Melon) - 4.15% (US/West)

~ Morgan Stanley - 3.12%

~Merrill Lynch ( $BOA ) - 2.76%

Europe: ~7.73%:

Clearstream Banking - 6.16% (European)

UBS Switzerland AG - 1.57% (Swedish/EU)

While Swedish now hold ~7.49% of $SIVE:

Försäkringsaktiebolaget Avanza Pension - 4.76%

Nordnet Pensionsförsäkring AB - 2.73

Before, Sivers was a ~60% European/Swedish retail owned company...

They went from that, down closer to 0 as they keep selling their shares.

US has close to majority control, right before the CPO supercycle of 2027.

Transfer seems almost complete?

Per Dahlström@PerDahlstrm

@aleabitoreddit Updated shareholder list………

English

ledrio retweetledi

I'm still laughing how much Swedish hate their own frontier companies so much.

That they write hit pieces every day on $SIVE.

This one was entertaining: Local journalists show up to an empty $SIVE administrative building uninvited.

Because they can't fathom the CEO is in Silicon Valley or design team is working on US Gov CHIPS act dev in the US. And because there weren't many cars parked outside + CFO wouldn't take questions about secretive hyperscaler deal financials.

They wrote a random negative hit piece.

By repeating "There are several who make lasers like these and Sivers are far from alone".

Several like $LITE, $COHR, $60B+ companies.

and reported earlier that "CPO is nothing special, it's been around for years."

While GS projects CPO going from $1B -> $91B TAM over the next two years.

Even put "Plans" in quotation marks because they didn't think Sivers is supplying lasers to $JBL 1.6T LRO.

IMO, $SIVE ends up as a $10B+ company next year, especially if they follow what $LITE / $COHR did with downstream IP integration to capture more of CPO module BOM.

Just don't think Swedish people understand hyperscaler supply chains, concept of forward growth, or the fact that employee count doesn't equate to revenue.

Transfer of control from local Swedish -> West is always appreciated, as this was a majority owned local retail company before.

English

@Longterms1 Storm var både aktiv o engagerad under sin tid som vd. Men du inser nog själv att en vd inte bör sitta och kommentera aktiekursen öppet på X, det hör inte till rollen. Nu när han inte längre har den rollen, kan han uttala sig friare och det gör han dessutom riktigt bra.

Svenska

ledrio retweetledi

We are now wating for the second round of US ChipAct funding for $SIVE. CEO shared in Q4 report and webinar that it has been delayed, but it is soon to be shared.

Mean while here you can watch details about the first founding round here ⤵️

Partnership with Ericsson $ERIC

and Raytheon $RTX

youtu.be/KIqEJ2mR8P8?si…

YouTube

English

ledrio retweetledi

Hint... $SIVE CHIPS Act round 2 incoming soon (consistent with the CHIPS Act renewal cycle)

The U.S. government doesn't just give out funding to random $1B Swedish companies.

It's highly unusual. And there's probably something markets are missing.

Since they got funding for:

-> $RTX and $ERIC Beamformers (space/telecom).

-> BAE Systems for STAR duplex arrays (radar jamming during electronic warfare)

Defense Primes are likely using Sivers microchip IP to build the final products with this.

As for the final products... What other space + military contractor applications are there involving LEO satellites? And I think you can guess.

The defense primes aren't trying to play Taylor Swift Youtube videos in space...

But the commercial spinoff can also be used for SpaceX/Amazon LEO Kuiper type applications.

Regardless, you have the side of the AI photonics story, which is the core growth vertical.

I'm most excited for photonics... but you also happen to get a company backed with U.S. CHIPS ACT embedded in Raytheon and BAE Systems for whatever black magic they want to do in Space.

Just nobody knows exact timeline + applications because due to the nature of CHIPS ACT defense contracts.

But it might appear randomly in financial statements down the road.

Anders Storm@StormDirac

We are now wating for the second round of US ChipAct funding for $SIVE. CEO shared in Q4 report and webinar that it has been delayed, but it is soon to be shared. Mean while here you can watch details about the first founding round here ⤵️ Partnership with Ericsson $ERIC and Raytheon $RTX youtu.be/KIqEJ2mR8P8?si…

English

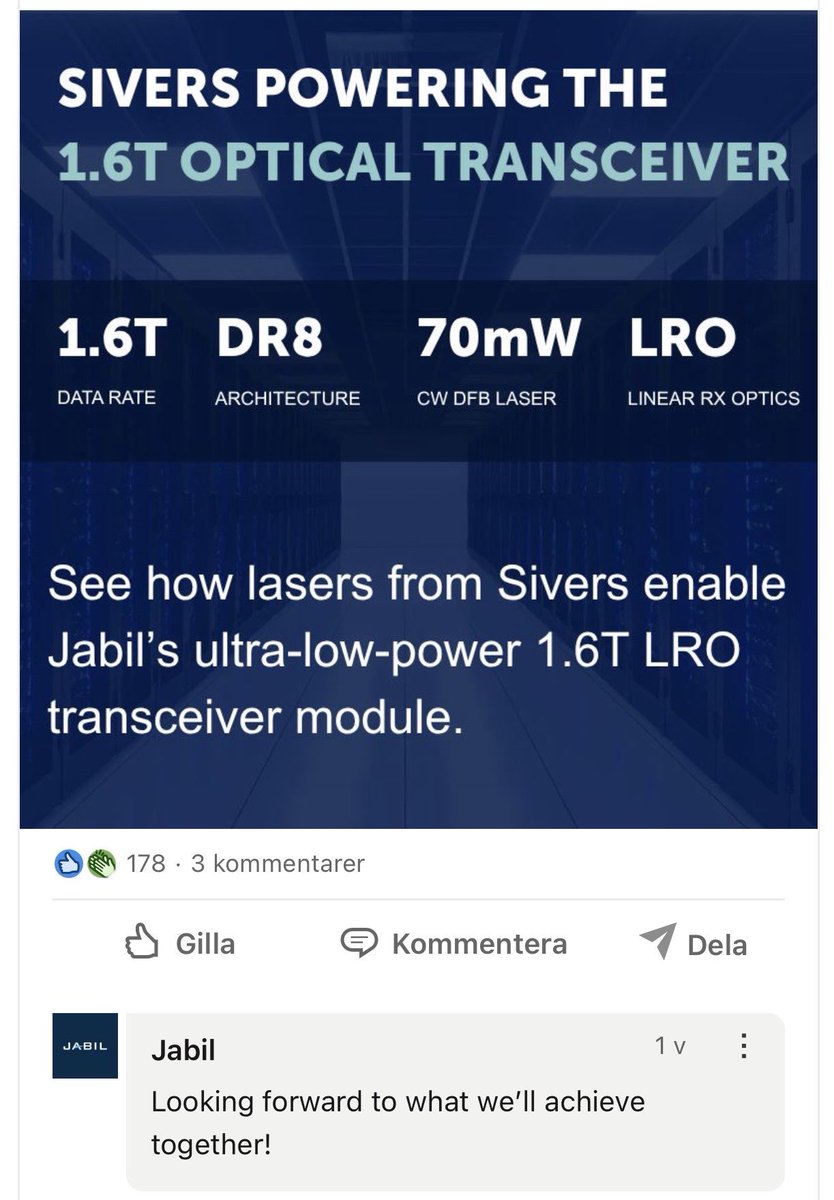

ledrio retweetledi

Look at this recent interaction on LinkedIn.

Jabil, a $34 Billion Fortune 500 manufacturing titan, publicly confirming their partnership with Sivers Semiconductors ( $SIVE / $SIVEF ).

What are they building together? An ultra-low-power 1.6T optical transceiver, powered by Sivers' custom CW-DFB Indium Phosphide lasers.

▪️ The Tech: CW-DFB is the exact high-power laser architecture required to solve the AI datacenter heat and bottleneck crisis.

▪️ The Partner: Jabil manufactures hardware for the biggest tech giants on the planet. When a Tier-1 foundry adopts your laser for their 1.6T module, you have successfully penetrated the global supply chain.

▪️ The Pick & Shovel Play: It doesn't matter if data centers buy custom Co-Packaged Optics or standard 1.6T pluggables from Jabil. $SIVE supplies the light engine for both.

Also make sure to read @PepInvestStocks post below, where he highlights the chain to $INTC

$SIVE $SIVEF $JBL #DeepTech #SiliconPhotonics #AI

Pep Invest@PepInvestStocks

$SIVE The deal that changes everything 🔥 $JBL $INTC Jabil + Sivers = 1.6T LRO in volume On April 15, 2026, Jabil (JBL) and Sivers Semiconductors announced a strategic partnership. Jabil is developing and manufacturing a 1.6‑terabit Linear Receive Optical (LRO) pluggable transceiver module - and is relying exclusively on Sivers’ high‑power DFB laser chips and arrays. Why is this so crucial? LRO is the logical evolution of Linear Pluggable Optics (LPO): DSP/retiming functions move into the switch ASIC (Broadcom Tomahawk 5/6, etc.). The result: up to 2.5× lower power consumption per bit and significantly less heat. Exactly what hyperscalers (Meta, Google, Microsoft, Amazon, xAI) need for 100k+ GPU clusters to break through power walls and cooling limits. Each individual 1.6T LRO module requires multiple high‑precision InP DFB lasers from Sivers - not commodity parts, but customized, high‑power, low‑noise light sources optimized for silicon photonics and CPO. Scaling at Jabil = direct scaling at Sivers. With a market cap of over USD 27 billion and as one of the largest EMS/supply‑chain partners of the hyperscalers, Jabil has the manufacturing power to bring these modules into the tens of thousands, later hundreds of thousands. If Jabil produces 1.6T LRO in volume, Sivers’ laser demand scales 1:1. The real bottleneck: InP lasers are the new “silicon wafer” of the AI era The AI‑optics market is exploding: Optical interconnects for AI: from ~USD 8.6B (2025) to USD 38B by 2034 1.6T modules alone are expected to exceed 5 million units in 2026 The entire pluggable + CPO market is growing at 20%+ CAGR But here’s the catch: wafer yields for InP lasers are below 30% for many players. Scaling is extremely difficult - it requires years of process expertise, specialized epitaxy, and yield‑ramp know‑how. Sivers has exactly that: one of the few scalable, commercially validated InP platforms.

English

ledrio retweetledi

This is true.

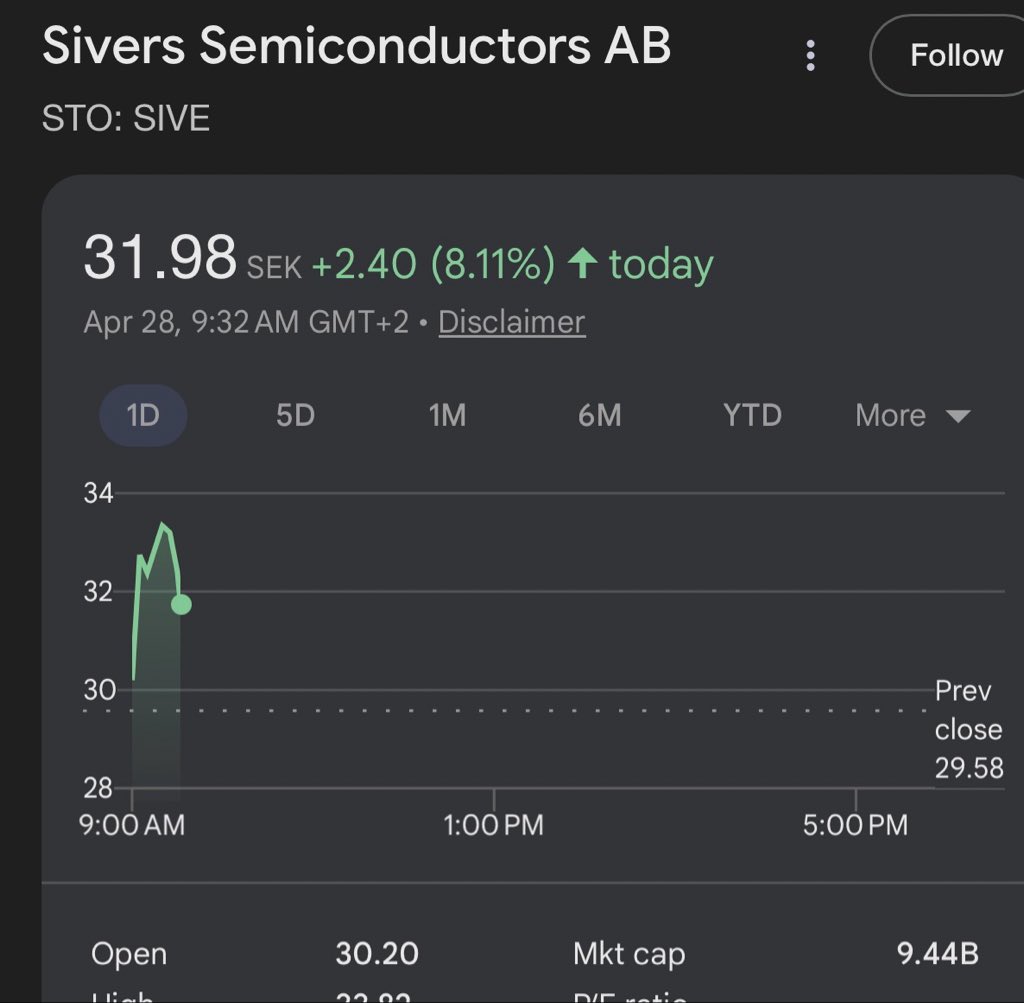

A few of bank analysts got passive aggressive when I called out $SOI back at $40 and it rose 125% since then.

Same with $SIVE and it’s risen a few hundred percent (and keeps going up)

But these same institutions are the one buying afterward on $IQE to $AXTI.

Usually institutions have silent accumulation periods blocks over months to not raise the price + accumulate the float off retail.

Then tell retail investors after it’s risen a lot and they own 5% of the company.

But if markets price that in a lot faster, institutions are forced to buy a lot higher.

Which is basically frontrunning institutions on supercycle names.

TopInvestor@Matrix_B0SS

This is funny, when retail investors are front running institutions they call it a bubble. What are they trying to do? Cause Chaos in market to buy Semi stocks cheaper as a lot of has been discovered. @aleabitoreddit $SIVE $LPKF $AXTI $AAOI

English

ledrio retweetledi

I'm happy Japanese communities started positions in $SIVE after doing research!

A stronger international shareholder base is always positive.

As for some thoughts, my read on the market looks like:

1. $NVDA bought out allocation from $LITE / $COHR

2. $AMD CPO went with $GFS + $SIVE / Win for remaining laser supply maybe $LITE if there’s still allocation.

3. And… $MRVL CPO will need lasers regardless.

$SIVE looks like one of the last remaining pure play merchant laser suppliers.

So Marvell will go with $SIVE (fits Celestial specs already) directly with multi-source down the road (maybe $MTSI). After they vertically integrate away interposer packaging process IP that feeds into Celestial.

Just some interesting things to back that up:

-> Ayar removed $MTSI and $LITE from their website and went with $SIVE as primary. Ayar’s connected to AlChip/GUC and others.

-> If look at the $GFS slide there's only two public players with $SIVE and $LITE after $AMD went with Globalfoundries for their CPO program.

-> $SIVE likely has agreements with Win since last year for laser capacity scaling.

$NVDA likely hasn't fully allocated that laser supply, so the remaining companies like $JBL, $AMD, and others go to Sivers for overflow.

Since $LITE signaled they were already fully allocated for 2028.

I could be wrong, but just based on public information that’s what it looks like.

As for why I think it's a good long:

-> Sivers also basically had no exposure to 800G or previous generations.

-> European markets price in previous 12 months revenue... hence previous depressed valuations

-> they get all the hyperscaler overflow created by market panic from $NVDA

But they also happen to be in the bleeding edge of CPO and even for gen-2 1.6T ( $JBL LRO) scaling next year in 2027.

Then for H2 2027 or 2028, they scale in adjacent areas like Silicon Photonics for likely $AAPL consumer devices.

Or FMCW 4D AI companies like $AEVA.

Many many years of development, finally coming to fruition next year.

I personally think markets are missing something big here, that the public uncovers over time with mapping hyperscaler relationships, website digging, or presentation slides.

Hyperscalers suppliers don't randomly choose a $1B Swedish laser company for no reason.

The direct contract with $JBL was the biggest signal of that.

And it’s my high conviction long moving forward.

みみりん@投資系女子@beauty_oe

インタラクティブブローカーズで、 $SIVE 遂に買えたァァ‼️😭 10日くらいかかった😂😂✨ さすがに調整あるだろうから、半額買って調整待つーっ‼️

English

ledrio retweetledi

High-performance wireless is the backbone of next-gen connectivity.

Sivers Semiconductors is powering this shift with advanced mmWave solutions built to enable everything from 5G infrastructure to SATCOM networks!

Discover more - sivers-semiconductors.com/wireless/

#Wireless #mmWave #5G

English