NΞLSXN

166 posts

Bitcoin has been bleeding to Gold since December 2024.

A single green monthly candle after 7 red consecutive monthly candles does not automatically mean the trend is over.

English

@brianbeers You know robotics and AI will do whatever you are doing in 10 years right? Be on the right side.

English

This is me

I own 36 auto repair shops, doing $50M a year in revenue

So, you’re probably thinking I have investors or trust fund.

But the reality is I don’t have either

I started 10 years ago when my brother and I bought 2 stores from a boomer.

Took all the money I made and bought another store in 2017.

Then 2 more in 2018 and every year since.

While everyone else is chasing crypto, AI, and all this “cool” shit.

I’m doing the opposite.

Just trying to buy auto repair shops from old people and run them better.

I’m not a mechanic and I’ve never fixed a car in my life.

But I got really good at building teams and betting on myself.

We’re just getting started

So, follow along for the journey.

English

NEWS: Mercedes has unveiled the VLE, a new all-electric van that will launch in the U.S. in 2027.

• Price (estimate): $100,000+

• Up to 370 mile range

• 300kW peak charging. 189 miles in 15 mins

• 31" rear retractable panoramic screen (8K resolution, split-screen capable) with 8-megapixel camera for rear-space video feed

• 115 kWh battery

• Sensors: 10 cameras, 5 radars, 12 ultrasonic sensors

• 800v architecture

• 0-60 mph: As low as 6.4s

• 93% battery-to-wheel efficiency

• Up to 408 hp

• Drag coefficient: 0.25 Cd

• Rear-axle steering: Up to 7-degree steering angle

• AIRMATIC air suspension with intelligent damping. Predictive height adjustment using Google Maps data

• Seating capacity: Up to 8 passengers

• Cargo volume with seats up: Up to 28 cubic feet

• Grand Comfort Seats (includes additional pillow, wireless charging, lumbar support, massage function, calf support)

• Panoramic roof: Sky View one-piece fixed-glass roof from B-pillar to rear with electric sunshade

• Additional features: Folding tables, wireless charging, Bluetooth gaming controller support

• Displays: 10.25" driver display, 14" central, 14" front passenger

• Audio: 22 speakers and Dolby Atmos

• Head-up display: Augmented reality navigation (virtual 23" image appearing ~13 feet ahead)

• Systems: MB. DRIVE with Distance Assist DISTRONIC, Lane Change Assist, semi-autonomous steering on motorways

Pricing will be announced later, but Mercedes said North American will only get the long wheelbase version and higher spec trims. Deliveries start in the U.S. in 2027.

More photos of the Van in the thread below:

English

@milesdeutscher You can’t drive an uber in 2028 anymore. FSD my friend.

English

I got chills when reading this article.

I've never been more bullish on AI. And I've never been more terrified of what that means.

It's written from the POV of June 2028.

But it's long, so I summarised it for you:

• AI gets good. Companies lay off workers. Margins expand. Stocks rip. S&P hits 8,000. Everyone celebrates.

• But fired workers stop spending. Companies weaken. They buy more AI to cut costs. More layoffs. Less spending. A negative feedback loop with no natural brake.

• The top 10% of earners drive 50%+ of all consumer spending. They're the ones getting replaced. A $180K product manager ends up driving Uber for $45K. Multiply that across every major city.

• Ghost GDP emerges - the economy is "growing" on paper, but the money never reaches real people. Productivity is booming. Wages are collapsing.

• Then it hits housing. $13 trillion in mortgages, all underwritten on one assumption: you keep your job for 30 years. In 2008, the loans were bad on day one. In 2028, the loans were good. The world just changed after they were written.

• S&P crashes 38% from highs. Unemployment hits 10.2%. Markets barely react anymore.

• The punchline: you're not reading this in 2028. You're reading it in February 2026. Every domino they describe has already started falling.

The canary is still alive. Barely.

Citrini@citrini

JUNE 2028. The S&P is down 38% from its highs. Unemployment just printed 10.2%. Private credit is unraveling. Prime mortgages are cracking. AI didn’t disappoint. It exceeded every expectation. What happened? citriniresearch.com/p/2028gic

English

SBF lost control of a $136 billion portfolio because he couldn't survive a 72-hour bank run.

On November 10, 2022, he was still CEO. Anthropic at 7.84%. 58 million Solana tokens. SpaceX through K5 Global. Robinhood at 7.6%. By November 11, he wasn't CEO of anything.

He made illiquid investments with customer deposits. Venture stakes in Anthropic and SpaceX. Massive Solana and SUI bags. Real estate. Every single one of these was a brilliant call. Anthropic became one of the most valuable AI companies on earth. Solana did a 15x. Bitcoin went from $16K to six figures. Buying Anthropic in April 2021 for $500 million when nobody in crypto cared about AI was visionary. On pure investment selection, SBF's track record is extraordinary.

He made really good investments. With other people's money. In assets he couldn't sell fast enough when those people wanted their money back.

A bank run can happen at any time when you're running a financial exchange. CoinDesk leaks a balance sheet, CZ tweets, and $6 billion in withdrawals hit in 72 hours. You can't liquidate a 7.84% Anthropic stake in an afternoon. That's the whole game. As CEO of a financial company, SBF massively under-invested in the one thing that would have saved him: asset controls. No reserves. No fund segregation. No asset-liability matching. No risk limits on Alameda's borrowing. A $32 billion exchange with the controls of a dorm room Robinhood account.

The bankruptcy lawyers then sold everything at cycle lows. Anthropic went for $1.3 billion. Worth $30 billion today. Solana in the low teens. Worth $12.4 billion today. Total recovered: $18 billion. Total value if held: $136 billion.

SBF was an awesome investor. We shouldn't all feel bad for him. He had every resource to build proper controls and chose to skip them because controls would have prevented the exact trades that produced this spreadsheet. That's the trade he actually made. And 25 years is what he gets.

SBF@SBF_FTX

English

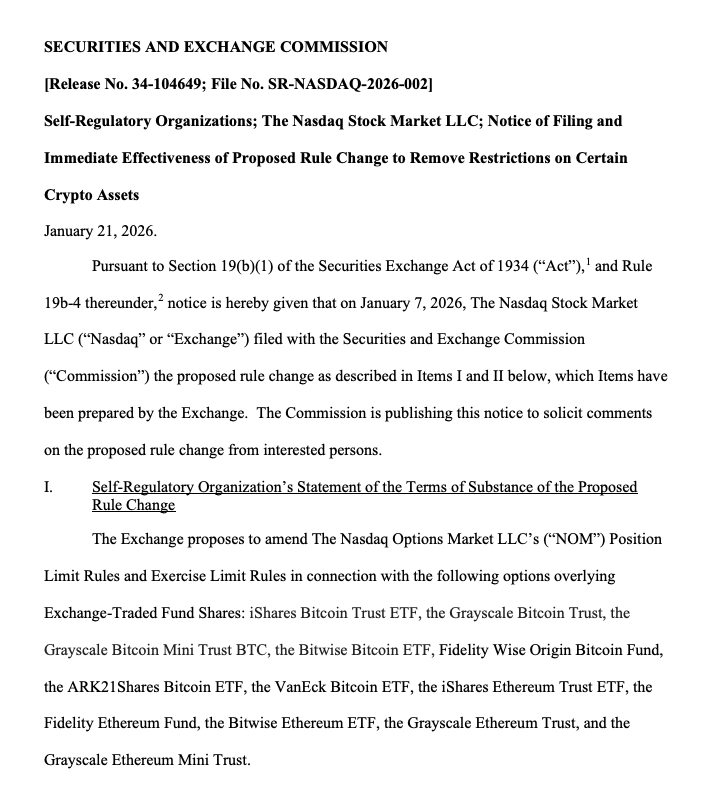

Kinda sus. Nasdaq requested that the SEC allow them to remove the options contract caps on the major BTC and ETH ETFs, and requested that they do so immediately without the standard 30 day waiting period. The SEC obliged. The contract caps were removed on Jan 21. $BTC went cliff diving on Jan 29.

Why the urgency by Nasdaq, a very buttoned up organization that isn't typically in a rush, especially with the crypto markets as weak as they were? These guys aren't dumb to the massive leverage options can inject. Maybe one or more funds had already blown up and a prime broker was panic requesting this change so they could liquidate the fund(s) before anything else went bad?

Could this have been the same fund(s) that blew up yesterday or are these things entirely unrelated?

At the very least, the removal of the contract limits has made the leverage available with IBIT FAR greater than leverage available anywhere else in crypto. Crypto was finally given our very own leverage nuclear weapon.

English

This was the highest volume day on $IBIT, ever, by a factor of nearly 2x, trading $10.7B today. Additionally, roughly $900M in options premiums were traded today, also the highest ever for IBIT. Given these facts and the way $BTC and $SOL traded down in lockstep today (normally SOL trades with beta) + the relatively lower liquidations on CeFi exchanges, this leads me to believe that the nexus of the problem lies with a large IBIT holder. IBIT has become the #1 venue for BTC options trading, so my guess is that a hedge fund trading IBIT options is the culprit.

If you look at the 13F filings for IBIT (I like whalewisdom dot com), you'll find a number of interesting names that have the majority of their fund in IBIT. In fact, there are a few in there (not naming names) that have 100% of their fund in IBIT, which likely means no cross margin. In fact, the biggest reason to set up a fund to hold a single asset would be to isolate margin, so that if the trade blew up, the brokers wouldn't have claim to any other assets.

Interestingly, most of these giant, single asset funds are based in HK.

We know that Asian traders, particularly in China, have been deeply involved in the Silver and Gold trade. Silver was down 20% today, which was the 2nd largest 1 day move in a very long time (largest on Jan 30). We also know that the JPY carry trade has been unwinding at an increasingly rapid pace.

This leads me to think that the culprit for the IBIT blowup today was 1 or more HK-based non-crypto hedge funds. As @FranklinBi pointed out, the fund(s) being non-crypto would explain why no one sniffed them out. They would likely have few/no crypto counterparties, meaning complete isolation from CT.

The last small piece of evidence I have is that I personally know a number of HK-based hedge funds that are holders of $DFDV, which had the worst single down day ever, with a meaningful mNAV decline. The mNAV had been holding steady surprisingly well throughout this pull back until today. One of these fund(s) could have been connected to the IBIT culprit, as I highly doubt a fund taking that large of a position in IBIT and using a single entity structure would only have the one fund.

Now, I could easily see how the fund(s) could have been running a levered options trade on IBIT (think way OTM calls = ultra high gamma) with borrowed capital in JPY. Oct 10th could very well have blown a hole in their balance sheet, that they tried to win back by adding leverage waiting for the "obvious" rebound. As that led to increased losses, coupled with increased funding costs in JPY, I could see how the fund(s) would have gotten more desperate and hopped on the Silver trade. When that blew up, things got dire and this last push in BTC finished them off.

I have no hard evidence here, just some hunches and bread crumbs, but it does seem very plausible. Let's see if some more concrete evidence floats to the surface here soon. The smoking gun will be a large fund fitting this profile filing a 13F showing a giant IBIT holding going to zero. Unfortunately, if a fund had their IBIT position liquidated today, they wouldn't have to disclose the position change until 45 days after the quarter end, so we'd be looking at mid May for the smoking gun from 13F filings most likely.

Hopefully some of you out there with too much time on your hands this weekend can snoop around more. My guess is that word will start to get out, because something of this size is just too hard to hide. Additionally, if the broker was not able to liquidate the fund in time, the broker may have a hole in their balance sheet, which would be even more difficult to hide.

English

@julianhosp If Julian Hosp disappeared, no one would give a shit. Period.

English

If bitcoin disappeared, no one would give a shit. It has absolutely zero utility in the real world. All it has done over the past 15 years is making some people, admittedly, including myself, rich, with this online casino. Let’s call a spade a spade.

Keith Weiner@RealKeithWeiner

This, too (17) is a Lie. Bitcoin *adoption* us exactly zero. It has not entered the field of finance. HODLing is not use.

English

During a very dark period, what was the best thing you ever did for your mental health?

English

I support @Strategy’s position urging MSCI to keep Digital Asset Treasury companies eligible in global indexes.

Neutral, market-reflective standards matter. Let innovation compete.

Read the full letter: strategy.com/msci

English

Adding back into my shorts with SIZE.

Y’all are dumb as fuck.

- Wynn

English

WHY I LOVE THE 50-YEAR MORTGAGE:

Here’s the full picture of the 50-year mortgage opportunity, including the extra interest you get "wrecked" by on the 50-year mortgage.

Monthly payments (6% interest, $500k home):

• 30-year: $2,997.75

• 50-year: $2,632.02

• Monthly difference: $365.73

Total interest paid:

• 30-year interest: $579,190.95

• 50-year interest: $1,079,214.38

• Extra interest from choosing 50-year: $500,023.44

So stretching the loan to 50 years means you pay an extra half a million dollars in interest to the bank.

But here’s the twist:

If you take the $365.73 monthly savings and throw it into Bitcoin compounding at 20% for 30 years, you get:

✅ $8,403,654

So the trade-off is basically:

• Pay the bank $500k more,

• But stack $8.4M in Bitcoin.

Even a 20% CAGR on BTC gets you $1m status in about 18 years with that small monthly contribution.

But remember, this is a 50 year mortgage. Instead of 30 years, you keep stacking $365.73 per month into Bitcoin compounding at 20% annually for 50 years, your final stack becomes:

✅ $445,081,564

Yes.

Four hundred forty five million dollars.

Off the mortgage-payment difference.

This is why the 50-year mortgage discourse is hysterical.

Boomers see “more interest to the bank,” you see “half a billion in BTC.”

Is the 20% terminal CAGR too high?

Perhaps, but a lot of people think it's going to be even higher at 30-40% over the next decade or so.

Saylor himself thinks the terminal CAGR will be around 20% after the next two decades are up.

Crazy numbers, but that's what the math says.

Take it or leave it.

English

@GrindeOptions BTC is a safer bet. Elon can die and that’s the end of it.

English

$100,000 or more held in $TSLA over the next decade will retire you, mark my words.

English