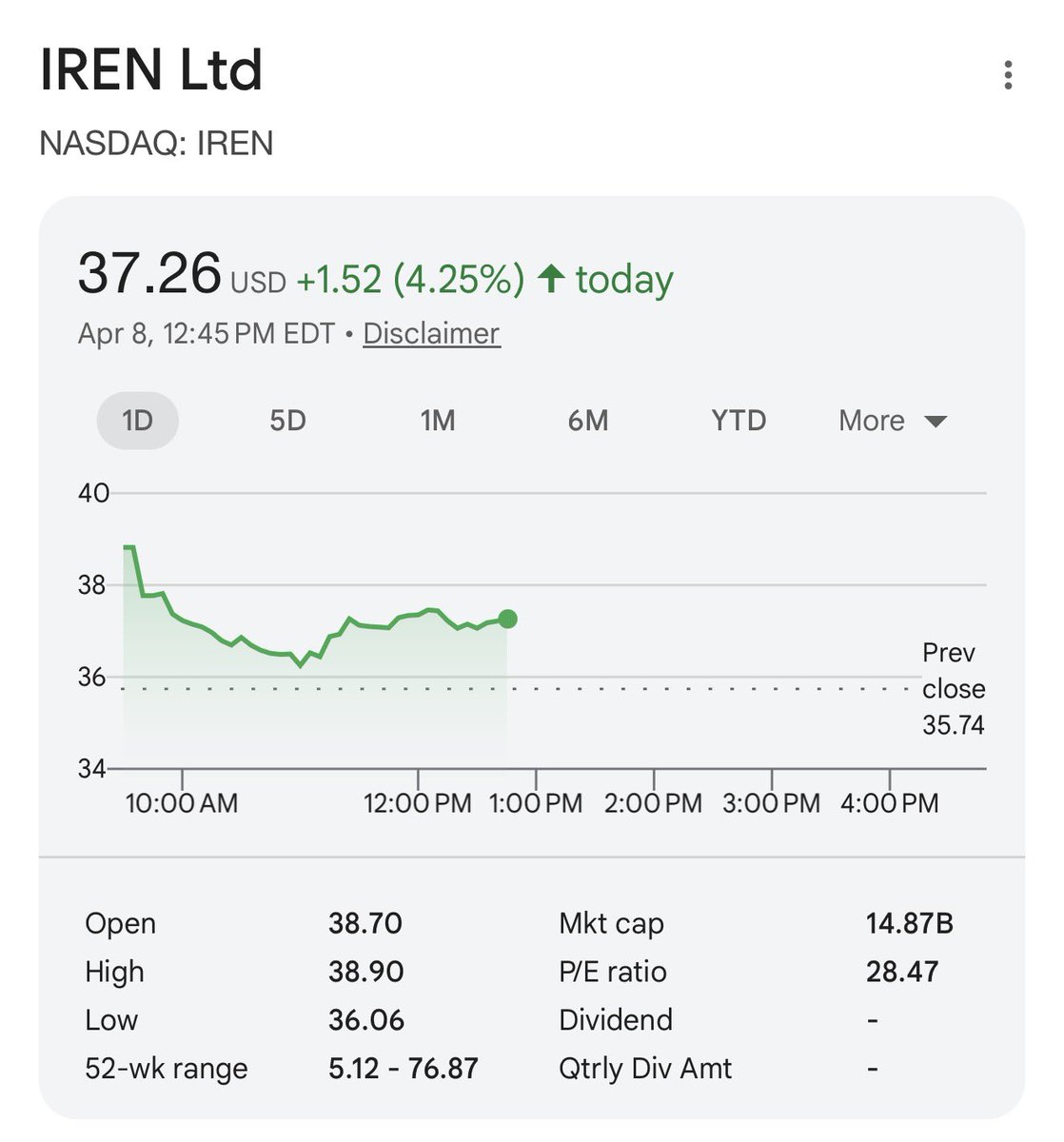

@Fibonacci_TA Thank you for the update. Flow being bearish for 24 hours doesn't change anything in Iren's structural thesis even if the print is bad tomorrow.

English

Lev Myshkin

27 posts

🔥 $IREN Flow Heatmap The $50 strike is telling two different stories depending on where you look. This Friday it carries the biggest put position on the entire grid — heavy near-term pressure right above current levels. Flip to June and the same strike is the most active green cell on the heatmap, with calls building for a move higher. January 2027 removes all ambiguity. Calls are green across every strike from $45 to $70 with no red in sight. The LEAP column is a clean bull sweep. The flow says expect friction near $50 through May, then the structure opens up. January positioning is already building for a run well above current levels.

IREN is acquiring Mirantis. Our advantage is infrastructure and execution. This builds on existing capabilities and strengthens how compute is deployed, managed and operated. Read more: iren.gcs-web.com/static-files/8…

IREN is acquiring Mirantis. Our advantage is infrastructure and execution. This builds on existing capabilities and strengthens how compute is deployed, managed and operated. Read more: iren.gcs-web.com/static-files/8…

@aleabitoreddit Too bad you fked up being an iren bear

🚨 "We’re building one of the world’s largest AI cloud platforms." $IREN 2026: 4.5GW $NBIS 2030 Target: 5GW The potential is beyond imagination for those who read the big picture. 👇 "The next cloud wave on the ground behaves more like an industrial buildout, where the scarce input is not GPU or code or even money, but (1) synchronized access to land, (2) substations, (3) transformers, (4) transmission capacity, and (5) utility approvals." The gap between those who started earlier and those who followed the trend is staggering.