Sabitlenmiş Tweet

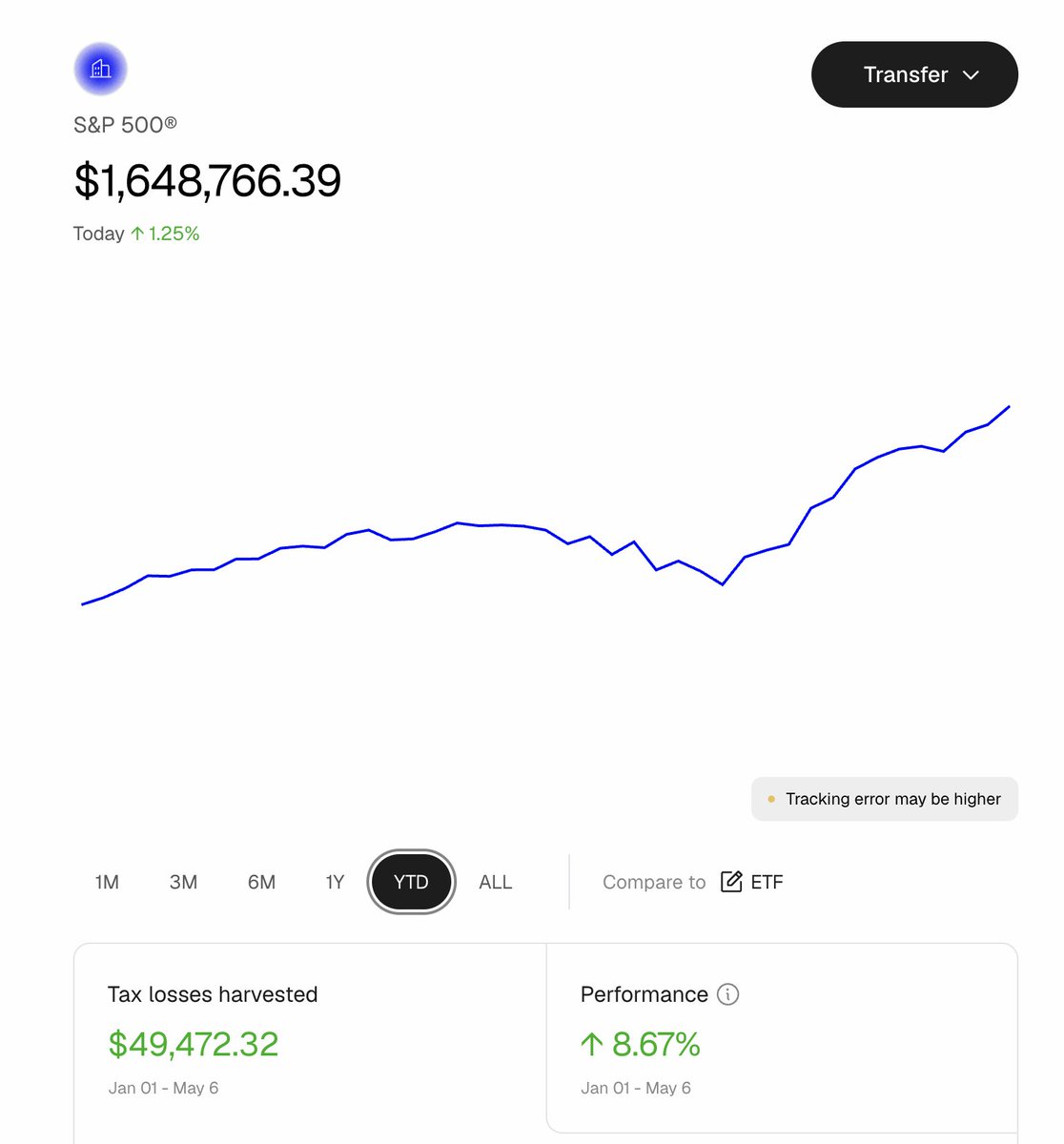

We’re very excited to share that Frec has now surpassed $1 billion in customer assets on the platform. 🚀🚀🚀

The speed of compounding is truly astounding.

It took us one year to reach our first $100 million, another year and a bit to get to $550 million, and less than four months from there to reach $1 billion. And here’s the most surprising metric: we added more than $80 million last week alone.

We always had conviction, but to the rest of the world, this milestone marks the moment Frec goes from “there’s something here” to “that is a real business.” We’ve crossed the chasm. Tax-aware investing delivered directly to customers is here to stay.

We’re deeply grateful to the thousands of customers who placed an enormous amount of trust in us.

And I’m also lucky to be working alongside an incredible team that brings so much grit, customer obsession, and passion to our mission every day.

$10 billion and beyond, here we come!

PS - We’re hiring backend and frontend software engineers, quant researchers, and quant developers. Ping me if interested.

English