Mani

211 posts

Mani

@manikanth2304

IT Consultant,Investor, learning new things.

Washington.D.C. Katılım Eylül 2010

557 Takip Edilen903 Takipçiler

Everyone talks about GPUs in AI.

But power is becoming the real need.

Bloom Energy’s AI data center deals could also help MTAR through its connection in the supply chain. $MTAR finance.yahoo.com/news/bloom-ene…

English

Mani retweetledi

Cheat code for investors - Warrants.

9/10 times ull be right in buying stocks post warrants are issued. Stock price goes multifold post that.

And if u get a stock which has rallied past previous warrant issued and new warrants are issued now, probability is 1 for making money

English

Just analyzed the last several months worth of market data

Here's every scenario that could play out and exactly what it means for the market:

Deal with Iran announced = Market hits all-time high

Negotiations underway with Iran = Market hits all-time high

Iran walks away from negotiations = Market hits all-time high

No deal with Iran = Market hits all-time high

English

Best way to evaluate personal year end performance is simple. What was your allocation to the top 5% winning stocks in any given year and what % of the upmove you could capture per stock. Forget CAGR it will take care of itself. #SDW

English

Addiction to dopamine rush you get from rearching a new stock idea silently compounds your biases and prevents you from focussing on top 5% winning stocks in any given year with sizeable allocation. Your capital and attention bandwidth are limited resources, use them wisely. #SDW

English

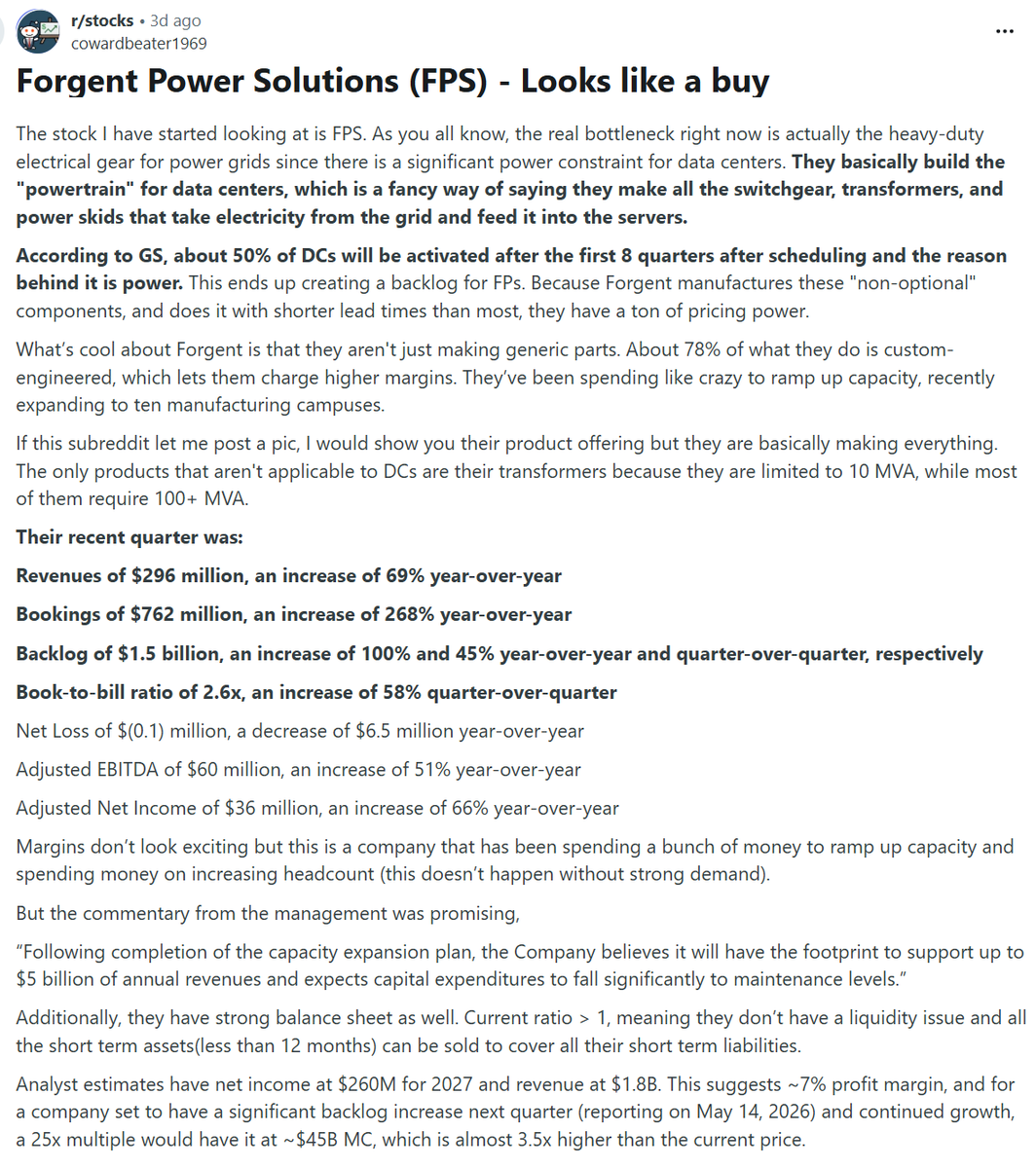

$FPS

Forgent Power Solutions

The new IPO and BO the base

Power theme- DC proxy.

@manikanth2304 the blog matching your thesis. check out.

Mani@manikanth2304

$AMSC and $FPS look like direct beneficiaries of the recent US push toward grid modernization and power infrastructure.

English

Mani retweetledi

This is one of the most important framework to keep in mind when investing in AI landscape. Currently we are in A phase of AI and gradually will move to V phase where AI apps will sit on top, churning out some phenomenal businesses. Successful investing is all about 'timing' the migration of profit pool within a value chain.

English

@3bagsfulll @SniPayne Euphoria can keep pushing the same target higher and higher. In the end, perception is what matters most.

English

Stocks sitting at the intersection of two or more live themes are where things get interesting.

Power + Data Centers

Semis + Optical Fiber

Defense + Electronics

Manufacturing + AI

Each theme attracts its own capital flow.

Rarely do both narratives break at the same time.

That creates multiple option-like payoffs from a single position.

English

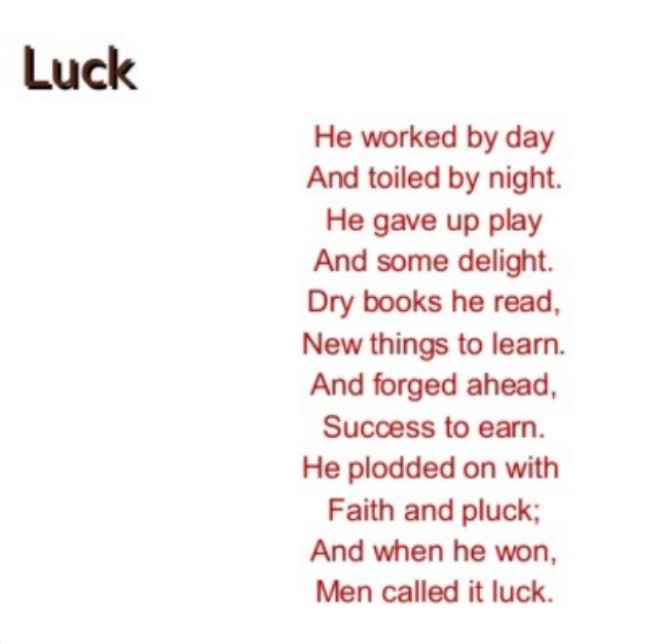

Mani retweetledi

The greatest compliment you would ever receive, if you are called lucky by many. Agree to them it was mere luck that brought you success☺️

English

Jeena Sikho Lifecare Ltd

#JSLL

What the market is missing ?

① OTC Optionality — Under-modelled

Street expectations are already moving towards ~250 Cr. OTC potential by FY28, but the actual optionality can be significantly larger. The company has rapidly expanded distribution, entered new topical OTC categories, and is building a portfolio with structurally better margins compared to prescription products. If execution continues at the current pace, OTC itself can become a major standalone value creator over the next few years.

━━━━━━━━━━━━━━

② Capital-Light Diagnostics

#Chandan_Diagnostics

The diagnostics business has the potential to create a ~50 Cr. annual revenue stream with almost zero incremental capex. Since the ecosystem, lab partnerships, and collection infrastructure are already in place, scaling becomes highly efficient from here. This is the kind of expansion that improves operating leverage without putting pressure on the balance sheet.

━━━━━━━━━━━━━━

③ Insurance Tailwind — Silent Re-rating Trigger

A structural shift is happening in reimbursement behaviour. Treatments and day-care procedures that were previously ignored are now increasingly getting insurance acceptance. This improves affordability for patients, increases treatment continuity, and can meaningfully improve demand visibility. Markets are still underestimating how powerful this change can become over time.

━━━━━━━━━━━━━━

④ Governance Upgrade

Statutory auditor Walker Chandiok (GT, Big 5), internal auditor Forvis Mazars (World #7), ERP migrated to Oracle, CRM live on Salesforce. In a sector rife with unorganised family-run clinics, this is a material re-rating trigger as institutional allocators have historically discounted the category.

━━━━━━━━━━━━━━

⑤ UAE Insurance Expansion

The company’s positioning in UAE creates access to a premium-paying patient base with better realization and higher ARPU. Insurance-backed acceptance of alternative medicine is improving steadily, which opens a much larger monetisation opportunity. This international optionality is still not fully reflected in market expectations.

Some Key Triggers:

① Entero distribution partnership.

Exclusive Ayurveda distribution tie-up with Entero Healthcare (Jan 2026). Opens up 1.25 lakh chemist network nationwide. Instant national footprint that would have cost JSLL 5 years and ₹200 Cr+ to build.

Revenue potential: ₹150-300 Cr in FY27 if even 20% of 16 SKUs achieve meaningful retail velocity. Entero's track record with Emami and similar brands is the sanity check.

② Bed capacity scale-up to 5,800.

Current: 2,850 built / 2,290 operational. Target: 5,800 beds by FY28 across owned + franchisee + college-partnership models. Capex-light (₹34 lakh/bed vs allopathy's ₹70L-1Cr).

If mature-cohort occupancy of 80% holds, 5,800 beds at ₹8,500 ARPOB generates ~₹1,440 Cr service revenue alone — 10x current. Plus medicine cross-sell follows proportionately.

Disc: Info for educations.

@manikanth2304 @LearningEleven if you are also tracking this company, please share the key points of your thesis in case I have missed anything here.

The Catalyst Decoder@YourShami

Jeena Sikho Lifecare Ltd #JSLL getting ready

English

The GOAT is in $BE #MTARTECH

Vineet Gala@VineetGala

Stanley Druckenmiller turned a 90day 400% gain in SanDisk into a rotation straight into the next AI bottleneck: power He loaded up on Bloom Energy, which is already up 150% in the last month. Different league altogether 🐐⚡️ thestreet.com/investing/stoc…

English