Sabitlenmiş Tweet

**𝐅𝐢𝐧𝐝 𝐌𝐮𝐥𝐭𝐢𝐛𝐚𝐠𝐠𝐞𝐫𝐬 𝐰𝐢𝐭𝐡 𝐌𝐨𝐧𝐭𝐡𝐥𝐲 𝐑𝐒𝐈 𝐬𝐭𝐫𝐚𝐭𝐞𝐠𝐲 **

How do you identify and hold stocks during a bull market to build multibaggers in your portfolio?

What gives you the confidence to stay invested in a stock? Let’s explore this using the monthly RSI.

I have backtested data from the previous bull market and found a common pattern among all the multibagger stocks. The investors who held these stocks in their portfolios noticed that they turned into multibaggers when a specific condition was met.

It’s actually quite simple — when the monthly RSI stays above 70, it clearly indicates a strong uptrend and shows the stock’s potential to become a multibagger.

I have tested this pattern across multiple stocks and observed the same consistent results. Now, let’s look at some examples below where you’ll notice this same pattern. You can even backtest it yourself — you’ll likely find similar situations.

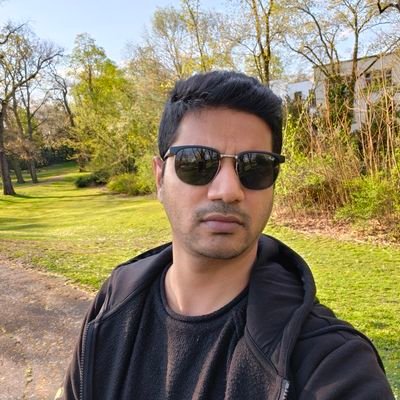

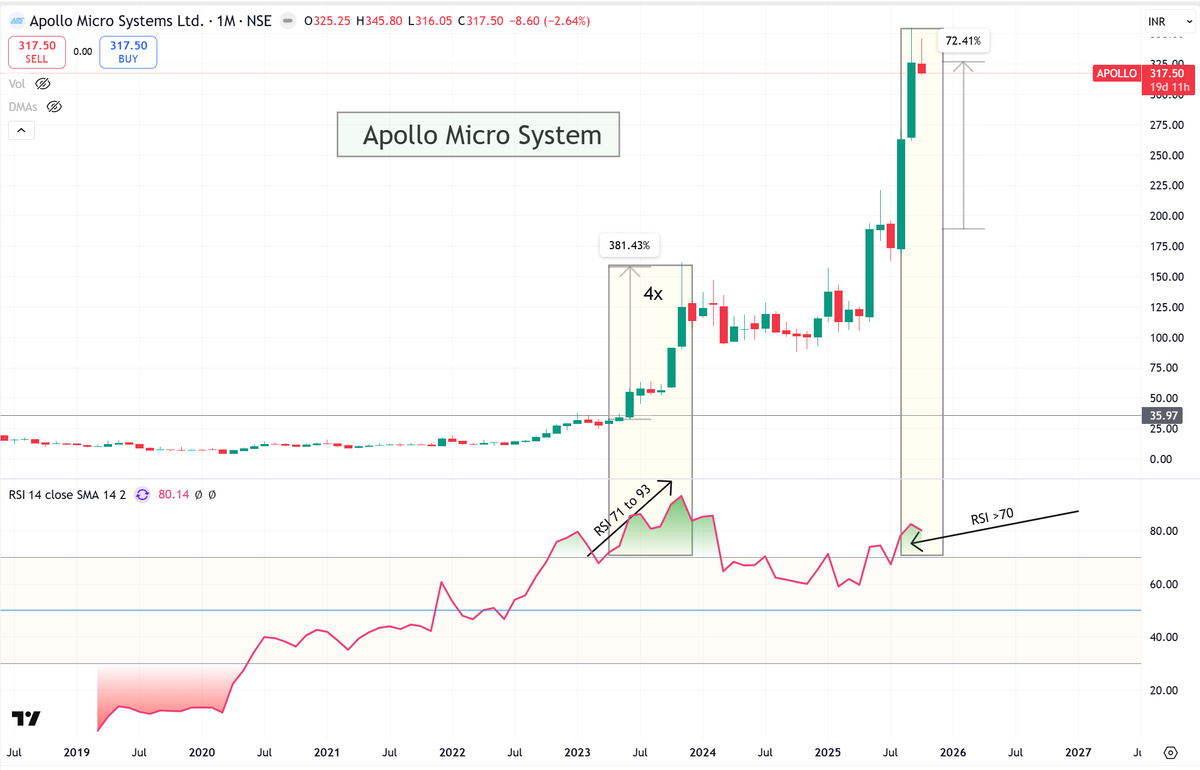

In my backtests, I’ve observed that when the monthly RSI rises from 70 to around 85, the stock price often doubles within a few candles. When the RSI further climbs to 93–94, the stock typically becomes a 4x to 7x multibagger. Of course, this move takes a few months, but with careful observation of chart patterns and sector strength, you can gain the confidence to stay invested and capture the full potential of the rally.

These patterns work effectively during a bull market. Now, the question is — how do you identify a bull market?

It’s actually quite simple. If the percentage of stocks trading below their 40W / 200 DMA moving average is less than 30%, it usually indicates that you are in a bull market.

Once you confirm that, the next step is to find the right sector leading the rally ( Ex: Power Sector ), and within that sector, identify the right stocks. When a stock’s monthly RSI crosses above 70, you’ll often see live examples of strong momentum and potential multibaggers forming right in front of you.

This insight can help you prepare for the next bull market and identify which stocks to hold in your portfolio for potential multibagger returns.

One important point to remember — this method is only for riding the stock, not for deciding your exit. For exits, you should always follow a separate strategy that suits your trading or investment plan

Shakti Pumps and Suzlon were part of my backtested examples, while Apollo and TD Power are currently showing similar setups — with their monthly RSI > 70.

One important point — you can set an alert in TradingView for when the monthly RSI crosses 70. Once it happens, TradingView will notify you automatically, making it easier to track potential breakout stocks in real time.

English