mtx

262 posts

mtx

@mattmtxsc

sloppy vibecoder on the lookout for arb oppties

United States Katılım Mayıs 2012

4K Takip Edilen295 Takipçiler

Sending 9 out of 195 graduating seniors to Stanford is insane

Guess which Bay Area high school this is

English

mtx retweetledi

I have always thought $UBER’s AV future may look similar to what is happening in China today. I see three somewhat bearish points and one more bullish point.

a) In China, the top three ride-hailing platforms are already profitable, even though the market has hundreds, maybe even thousands, of ride-hailing companies.

b) In an AV world, $UBER’s suppliers could become much more concentrated. That would give suppliers more bargaining power and likely pressure Uber’s margins.

c) The big AV suppliers may only “outsource” their fleets to Uber when they have excess capacity. That means Uber’s market share could be much lower than it was before AVs.

d) If Uber is only the aggregation layer and does not manage much of the fleet itself, then traffic platforms could also build their own aggregation products pretty easily. Tencent, Alibaba, and Meituan already have their own aggregation offerings in China.

And selling traffic is exactly what Meta and other Western platforms are good at. If they do not need to manage the fleet themselves, they may also enter this layer. So Uber’s competition may not just come from AV companies, but also from large traffic platforms.

English

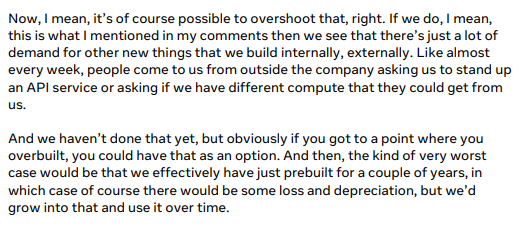

The market reaction of punishing $META because of the increase in CapEx will turn out to be very wrong IMO.

In the $META Q325 earnings call, Zuck already explained well that if $META overbuilds their compute infrastructure for internal needs, they can sell it to external parties.

We are in one of the biggest compute demand/supply imbalances that seems to be getting worse, not better. $GOOGL GCP CEO Kurian expects demand to be bigger than supply for 10 years.

$META's enormous AI compute capabilities will either return ROI in the form of their products (which they are already showing) or/and give great ROI by selling compute to external companies. $META investing in AI data center compute is a big asset, not a cash burn, similar to what metaverse investments were in large.

The market is viewing it as a negative, instead of an enormous strategic advantage in a compute-constrained world.

English

@Flyingfishtrump @Midnight_Captl @austinsemis doesn’t that actually make amd more attractive to enable more HBM at lower unit cost?

English

@Midnight_Captl @austinsemis Look at it as investing in growth with rising interest rates. When money is free, investors buy any unprofitable trash. When money becomes more expensive, they have to be more selective. Good luck to AMD selling at a discount to Nvidia with 1.5x more latest-gen HBM per chip.

English

Memory starting to worry me a bit @austinsemis covered this in his recent podcast (SemiDoped - highly recommend)

Memory is effectively a tax on the AI ecosystem. Incremental spend on memory is ~$0 ROI for the Hyperscalers

Worried it’s going to start suffocating growth

English

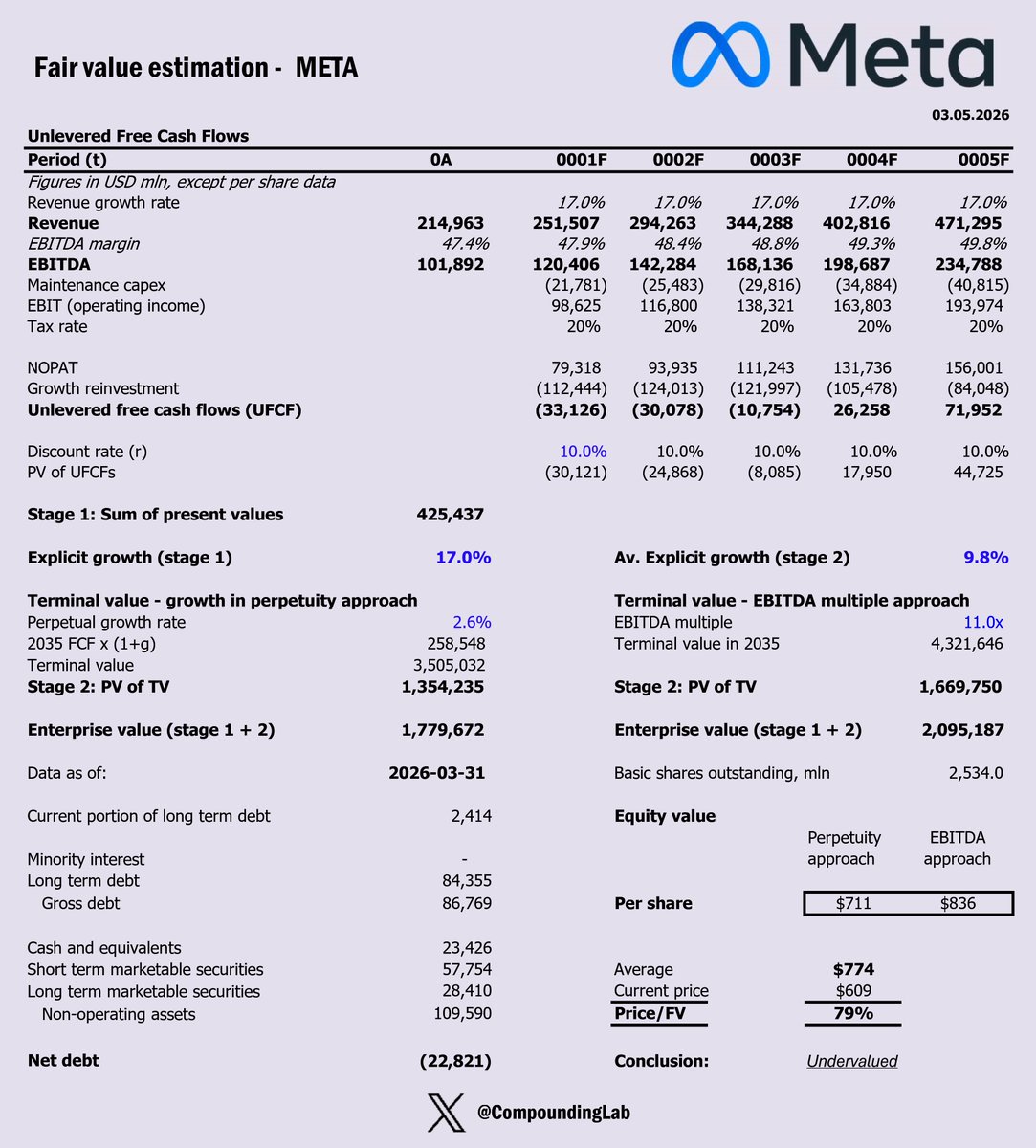

@CompoundingLab constant growth at 17% and then step down to 2.6% in terminal growth?

English

$Meta DCF valuation model (revised)

Subs,

Last time I shared my insights on META was in November 2025. Since then, many developments have occurred. The Capex Supercycle for Mag7 is now approaching a parabolic trajectory, making an update to the model essential. Let’s dive in.

Key assumptions:

* Explicit average 5Y/5Y growth @ 17%/10%

* Long-term growth in perpetuity @ 2.6%

* Adj. EBITDA Margin expansion from 48% to 52% in the terminal year.

* WACC @ 10%.

* Adj. EBITDA exit multiple of 11

* Tax rate 20% - in line with historical marginal rate

* The input that drives reinvestment is linearly regressed from current levels closer to the Software (Entertainment) average rate of 1.67 in year 10

Follow my Substack for regular actionable investing frameworks, incl. a more detailed DCF.

English

@thsottiaux codex desktop app not connecting to github repo and / or codex web

English

@FinanceJack44 why keep looking at financials only instead of operating metrics? meta is mortgaging the future of its existing business without a clear second growth driver

English

Most $META investors are getting caught up looking at EPS and FCF.

What I'm looking at is OCF, which has been exploding.

When CapEx is high OCF can be a great proxy for what future profitability could look like.

$META just grew OCF 34%…

This business is still an absolute beast even in an investment cycle.

English

@gmoneyofficial is that alarming to you? maybe the market is not as stupid as you think?

English

Gas is now $6.799/gallon in the Bay Area and SF.

It cost me $133 to fill up my car. 🫠

English

What isn’t priced into Anthropic’s or OpenAI’s gigantic valuations is that they have no moat.

I use both ChatGPT Pro and Claude Max, and we’re reaching the point where there’s very little practical difference between Codex, Claude Code, GPT-5.5, and Opus 4.7.

That tells me the long-term value won’t sit in the model or harness layer. Those layers will become commodities, with pricing pushed down to token cost plus a thin margin.

English

mtx retweetledi

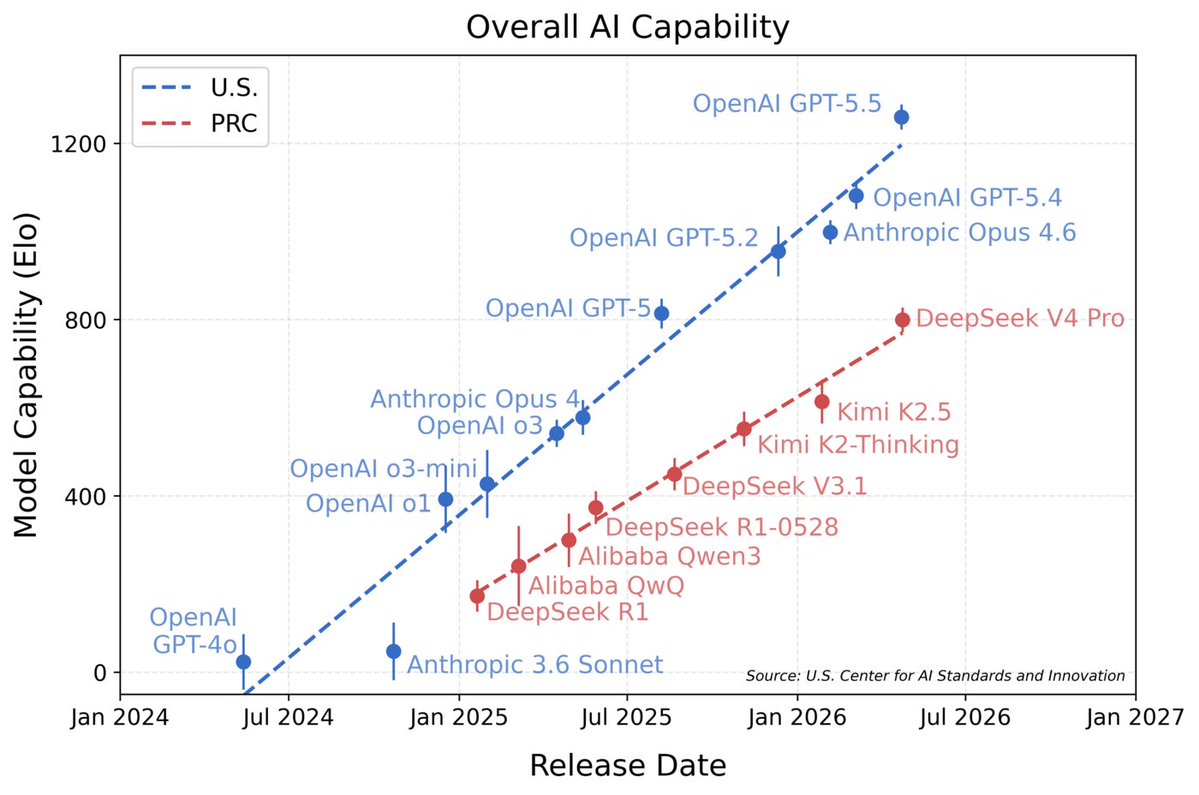

DeepSeek V4’s capability lags behind leading U.S. models by about 8 months. nist.gov/news-events/ne…

English

I am still curious as to why Claude is SO MUCH better than ChatGPT or Gemini.

One part is that Opus is better than GPT 4.5 and Gemini 3X

Another part is that the harness tools are much more extensive

It's not just for coding. Claude on the Mac is like 10X better than using either product.

Thoughts?

English

@dalibali2 the flip argument is that saas industry spends more on data lock-ins that actual innovation (R&D). now the workflow is changing, the data moat is also eroding

English

Enterprise software only spends 20-30% of revenue on R&D, the majority of opex is on acquiring, retaining and contracting customers. Which makes the argument that labs will own all areas of b2b hard to believe. It’s more likely that they focus on specific areas that makes sense for their individual customer acquisition funnel.

A few less discussed predictions from me:

1/ low end M&A dies. <20M ARR deals generally are feature tuckin when the cost to build drastically decreases the value of sub scale feature deals also decreases

2/ implementation margins erode faster than product margin. Real or not customers have a perception that SW time to value must now be faster. Those heavy duty implementation like ERP that used to get 35% margin quickly get squeezed

3/ the end state is that AI is a core platform feature but before we get there we’ll see many companies try and fail to pass that cost through to customers. Long term to protect margins, large ecosystem vendor will monetize their API access to extract toll from ISVs. After all why have some AI feature sit on top of ur records for free? It’ll look bad at first (eg Salesforce) but then everyone will do it)

English

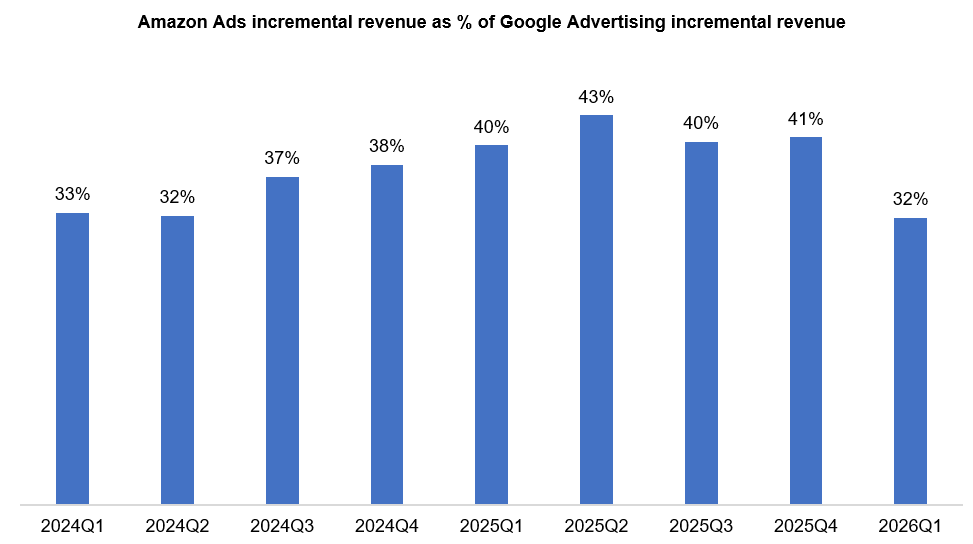

"It is interesting to observe a noticeable drop in Amazon ads incremental share compared to Google advertising which itself is losing share to Meta’s FOA.

For the last four consecutive quarters, Amazon ads grew at 22%. In contrast, Google advertising accelerated in each of the last four quarters"

Mostly Borrowed Ideas@borrowed_ideas

$AMZN 1Q'26: Rosy Near-term but "Cloudy" Long-term

English

I’m really struggling to see how the back of the envelope math on this works out…

There are generously 4 million characterized “software workers” in America. That’s pretty broad and includes a lot of people who aren’t really classical engineers don’t produce that much code.

That comes out to nearly $1k per month of average Claude spend across every dev in America. Yes, there’s some international usage, but it can’t be that much. Yes there is some non software Cowork usage, but that doesn’t use that many tokens. Yes, some non engineers are using Claude to vibe code, but I really doubt many are spending hundreds per month on.

Even if we assume 50% of all software workers are using Claude, that comes out to $2k spend per month per Claude user. Thats 10X more than the highest tier Max subscription. So almost all of Anthropics revenue has to be API billing

So the only explanation is that something like 20%+ of software engineers are not only Claude users but on API billing and regularly spending thousands per month. At $5/m Opus tokens that means the average API user has to be going through something like 25 million tokens per day.

*OR* the other possibility is API revenue is heavily power law dominated. Maybe there’s just something like 100k super users who are making up the majority of the revenue. For that to work the typical super user would have to be spending on the order of $50k/month and guzzling nearly 1 billion tokens per day.

Tannor Manson@Futurenvesting

Anthropic is now showing off $44 BILLION in annual recurring revenue. This is up $14 billion (+46.6%) since last month! BULLISH for AI Infrastructure $NVDA $AMD

English