Sabitlenmiş Tweet

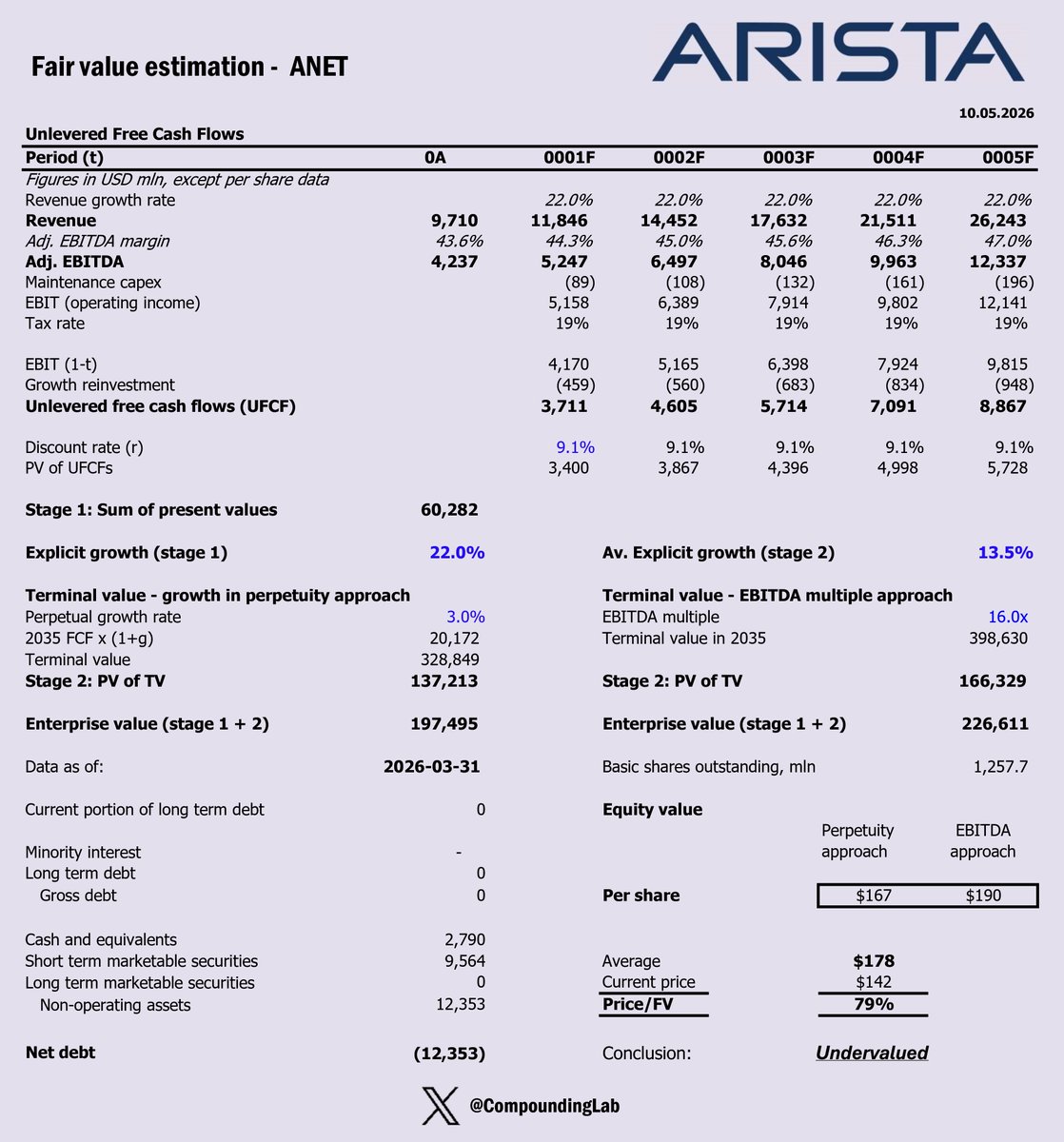

$ANET DCF valuation model

Arista has been a wonderful growth story for shareholders, with an impressive 42% return over the past 10 years. That's genuinely remarkable! But for us investors it's important to consider what lies ahead. Can Arista continue to outperform the index? Let’s take a closer look to find out.

Key assumptions:

* Explicit average 5Y/5Y growth @ 22%/13.5%

* Long-term growth in perpetuity @ 3%

* EBITDA Margin expansion by 0.7pp every year until the end of explicit period

* WACC @ 9.1%.

* Adj. EBITDA exit multiple of 16

* Tax rate 19% - in line with historical average

* The input that drives reinvestment is Sales to Capital ratio = 5.7

More details on Substack - link in bio and below 👇

English