Sabitlenmiş Tweet

Founders, stop paying for cabs, coffee, and client lunches from your own pocket.

As founders, we constantly pay small company expenses - cab rides, coffee meetings, team lunches - and then forget to reimburse ourselves.

It’s basically an unofficial "founder tax”!

That hit home 🎯 - because I’ve been there.

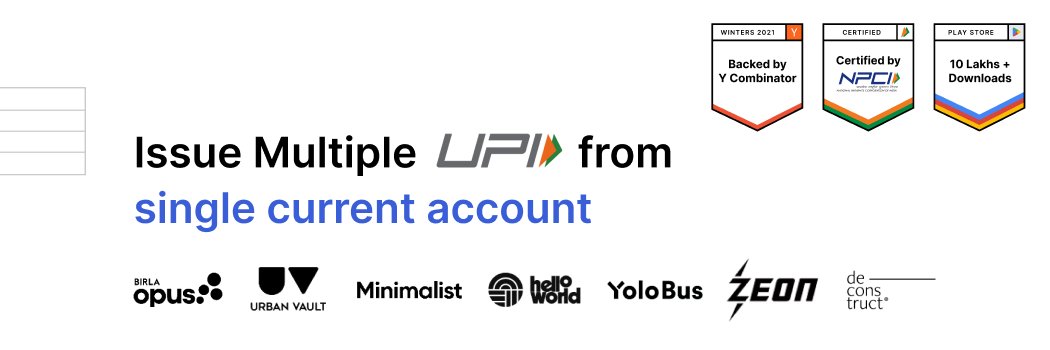

At @CashBook_App : UPI Wallets for Employees, we decided it’s time to fix this.

Introducing our Founder Launch Plan 🎊

FREE UPI wallets for founders for the first full year 🗓️.

Load your wallets from your company’s current account, spend instantly on cabs or client lunches and effortlessly attach invoices right then and there. No reimbursements, no hassle, no forgotten expenses ✅

After the first year, you’ll have the option to renew at a simple, affordable monthly price. Ready to stop mixing personal funds with company spends? Drop a 🚀 below, and we’ll set you up within minutes!

English