Misscrpyto📉📊🚀

94.5K posts

Misscrpyto📉📊🚀

@mhaithaca

Tägliche Krypto News & Marktanalysen für jeden | Bitcoin, Krypto & Web3 | Autorin & YouTube Creatorin | Folge mir für Updates! | Keine Finanzberatung

Katılım Temmuz 2007

5K Takip Edilen3.6K Takipçiler

@wellguys321 @MissCryptoGER Hey, welcome to X and thanks for joining!!! Give me a follow back here on my burner acc I’ve got something for you 🚀🪐

English

@MissCryptoGER naja wenigstens palawerst du nicht wieder über deinen shitcoin bzw. bitcoin….

Deutsch

Gold auf 20.000 $?! 🤯 Während der Kurs fällt, platzieren Wale gerade die "Wette des Jahrzehnts"!

Gold ist kürzlich hart korrigiert. Trotzdem passiert am Optionsmarkt etwas Verrücktes: Trader kaufen massenhaft Call Optionen (Wetten auf steigende Kurse) mit Ziel 15.000 $ bis 20.000 $ für diesen Dezember.

Warum werfen die ihr Geld scheinbar aus dem Fenster? Diese Optionen kosten aktuell fast nichts (wie "Lotto Tickets"). Aber: Wenn Gold wegen geopolitischer Eskalation oder Fed Panik auch nur ansatzweise stark steigt, vervielfacht sich der Wert dieser Optionen explosiv. Es ist eine extrem günstige Versicherung gegen den Systemkollaps.

Großinvestoren erwarten in den nächsten Monaten massive Turbulenzen und gigantische Preisausschläge (Volatilität). Lass also die Wall Street zocken. Wenn es wirklich knallt, bist du mit physischem Gold (oder Xetra Gold) bestens aufgestellt (NFA). Das ist dein echter "Long Call" auf Werterhalt, oder wie siehst du das?

*Walter Bloomberg@DeItaone

GOLD $20,000 CALLS SURGE DESPITE RECORD SELLOFF Deep out-of-the-money bullish bets on gold are building even after a historic correction. After COMEX gold futures briefly topped $5,600 an ounce in late January before suffering their largest one-day drop in decades, traders began accumulating December $15,000/$20,000 call spreads. The position has since grown to roughly 11,000 contracts, even with prices consolidating near $5,000. Aakash Doshi of State Street Investment Management said the size of the trade is striking given its distance from current prices, likening it to a “cheap lottery ticket.” Gold has doubled since early 2024, fueled by speculative flows, geopolitical tensions, concerns about the Federal Reserve’s independence, and diversification away from currencies and sovereign bonds. For the spread to expire in the money, prices would need to nearly triple by December. The structure limits upside but reduces upfront cost, allowing traders to exit on a sharp rally or hold to expiry if gold surpasses $15,000. While spot prices remain far below those levels, the trades have lifted implied volatility for far-upside calls. Despite a recent easing in call skew, realized volatility remains elevated, leaving room for large price swings after January’s 11% plunge and October’s sharp correction to $4,000.

Deutsch

@FHoltzwart @MissCryptoGER Hey, welcome to X and thanks for joining!!! Give me a follow back here on my burner acc I’ve got something for you 🚀🪐

English

@MissCryptoGER Wenn es richtig knallt, gibt es keinen Bäcker mehr, bei dem du für eine Unze Gold dein Brot kaufen kannst. Dein Bitcoin ist wertlos ohne Energie. Nur deine Kartoffeln vom eigenen Land kannst du essen. Denk drüber nach.

Deutsch

@Ziliqa1381 @MissCryptoGER Hey, welcome to X and thanks for joining!!! Give me a follow back here on my burner acc I’ve got something for you 🚀🪐

English

@Serywolk588 @MissCryptoGER Hey, thanks for following and likes on my post. how are you doing today?

English

@MissCryptoGER 7.000$ - 11.000$ sind realistisch, der Rest die Sahne-Kirsche

Deutsch

Misscrpyto📉📊🚀 retweetledi

Misscrpyto📉📊🚀 retweetledi

Schluss mit Kaffeesatzleserei: Kennst du den wahren Wert deiner Sats? 🟠

Nachdem ich euch neulich das Tool für die XRP Army gezeigt habe, wurde ich oft gefragt: "Gibt's das auch für Bitcoin?" Na klar.

👉 Check deinen Status: misscrypto.de/bitcoin

Heute im Fokus meiner Tool Serie: Der Bitcoin Master Hub. Viele starren bei Bitcoin nur auf den Preis in Dollar. Dabei sind die Daten onchain viel spannender. Ich habe euch ein Dashboard gebaut, das euch zeigt, wie gesund das Netzwerk wirklich ist.

Hier sind die Features:

- Sats Richlist: Bist du ein "Shrimp" (< 1 BTC) oder schon auf dem Weg zum "Wholecoiner"? Gib deine Sats ein und vergleiche dich mit der ganzen Welt.

- Gold Flippening: Der beliebteste Rechner. Was ist dein Portfolio wert, wenn Bitcoin die Marktkapitalisierung von Gold knackt? (Spoiler: Die Zahl wird dir gefallen).

- Halving & Supply: Wie viele Bitcoin gibt es wirklich noch zu schürfen? Sieh dir die Verknappung in Echtzeit an.

Egal ob Maxi oder Neuling, diese Daten sollte jeder kennen.

Probier es mal aus und sag mir, welchen "Rang" du auf der Richlist hast! 😉

Deutsch

Misscrpyto📉📊🚀 retweetledi

Today we announced our $15M Series A, led by @Accel, and launched Prism — agentic reporting that can explain your finances.

Prism gives you answers you can follow: what changed, why it changed, and the transactions behind it. It’s reporting that shows its reasoning.

usequanta.com/prism

English

Misscrpyto📉📊🚀 retweetledi

Großbritanniens größter Versicherer baut auf dem XRP Ledger! Ist das der Startschuss für die institutionelle Massenadoption?🧐

Ripple landet einen gewaltigen Treffer in Europa. Aviva Investors (der globale Vermögensverwalter des Versicherungsgiganten Aviva plc) hat eine strategische Partnerschaft mit Ripple angekündigt.

Aviva will seine klassischen Fondsstrukturen tokenisieren und dafür den XRP Ledger (XRPL) nutzen. Das ist Ripples erste Zusammenarbeit dieser Art mit einem großen europäischen Vermögensverwalter. Nigel Khakoo von Ripple betont, dass wir die Phase der "Experimente" verlassen. Es geht jetzt um "Large Scale Production" – also den echten Einsatz von regulierten Finanzprodukten auf der Blockchain.

Warum XRPL? Aviva entscheidet sich bewusst für den XRP Ledger wegen der integrierten Compliance Tools, der Geschwindigkeit und der niedrigen Kosten. Das bestätigt, dass die Infrastruktur von Ripple für streng regulierte Finanzinstitute attraktiv ist.

Für Anleger bedeutet das langfristig schnellere Abwicklungen und geringere Kosten, da Zwischenhändler durch die Blockchain Technologie (ohne energieintensives Mining) ersetzt werden.

Wenn ein Schwergewicht wie Aviva (mit Milliarden an verwaltetem Vermögen) seine Produkte auf den XRP Ledger bringt, ist das ein massiver Vertrauensbeweis. Es zeigt, dass "Real World Assets" auf der Blockchain der neue Standard für die Finanzwelt werden.

Markus Infanger@markusinfanger

A genuinely huge moment for XRPL as traditional finance moves onchain! Aviva Investors, the global asset management business of leading UK insurer Aviva plc, has announced a partnership with @Ripple with the intention of tokenising traditional fund structures on the XRPL. Read more about how we will be working with Aviva Investors here: ripple.com/ripple-press/a…

Deutsch

Misscrpyto📉📊🚀 retweetledi

Mathematisch unausweichlich: Warum QNT 2026 in einen Supply Shock läuft.

Wir haben maximal 14,6 Millionen Token. Das ist fix. Durch das neue Update "Bring Your Own Node" (BYON) muss jetzt jeder neue Netzwerkteilnehmer QNT als Sicherheit hinterlegen ("locken").

Gleichzeitig eliminiert Quant die Inflation: Staking Rewards kommen ab sofort zu 100 % aus echten Einnahmen (Real Yield), nicht aus der Druckerpresse.

Was passiert, wenn das Angebot sinkt, aber die institutionelle Nachfrage steigt? Ich rechne es euch im neuen Video vor. 👇

Deutsch

Misscrpyto📉📊🚀 retweetledi

Binance geht "All In": 1 Milliarde Dollar Sicherheits Fonds jetzt komplett in Bitcoin!

Ein starkes Signal für Bitcoin als "Store of Value". Binance hat sein Versprechen gehalten und den Umbau des SAFU Fonds (Secure Asset Fund for Users) abgeschlossen. Innerhalb von nur 30 Tagen wurden die Reserven, die früher größtenteils in Stablecoins lagen, komplett in Bitcoin umgeschichtet.

Mit einer finalen Tranche von 4.545 BTC wurde der Plan heute vollendet. Der Fonds hält nun 15.000 BTC. Das entspricht aktuell rund 1,005 Milliarden US-Dollar (gerechnet bei einem Kurs von ~67.000 $).

Der SAFU Fonds ist die "Notfallversicherung" der Börse für ihre Nutzer (z.B. bei Hacks). Dass Binance diese kritische Reserve nun zu 100% in Bitcoin hält, ist ein massiver Vertrauensbeweis. Sie setzen darauf, dass Bitcoin langfristig der stabilste und sicherste Wertspeicher ist – sogar verlässlicher als Dollar-gebundene Stablecoins.

Transparenz ist dabei garantiert: Die Wallet Adresse ist öffentlich, jeder kann die Bestände auf der Blockchain (OnChain) überprüfen.

Binance@binance

#Binance SAFU Fund Asset Conversion – Final Update Binance has successfully completed the final tranche purchase of 4,545 BTC, finalizing the $1 billion transition of SAFU stablecoin reserves into Bitcoin. This transition was completed within 30 days of the initial announcement, as committed. SAFU now holds 15,000 #BTC, worth $1,005,000,000 USD at the time of completion (calculated at a BTC price of $67,000). SAFU BTC Address: 1BAuq7Vho2CEkVkUxbfU26LhwQjbCmWQkD Latest TXID: blockchain.com/en/explorer/tr… With SAFU Fund now fully in Bitcoin, we reinforce our belief in BTC as the premier long-term reserve asset. Thank you for your continued trust and support. We remain committed to transparency and security.

Deutsch

Misscrpyto📉📊🚀 retweetledi

New York drivers aren’t reckless. The system is. Fraud and lawsuit abuse help make NY’s auto insurance the most expensive in the nation.

Click to read more:

English

Misscrpyto📉📊🚀 retweetledi

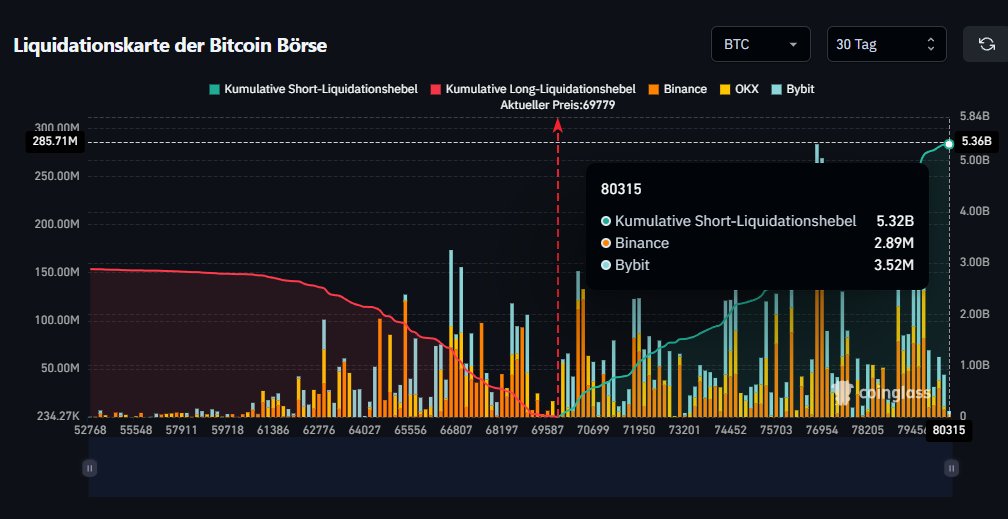

🧲 Warum Bitcoin fast "gezwungen" ist, auf 80.500 $ zu steigen!

Der Markt jagt immer die Liquidität und die Bären haben sich gerade eine riesige Zielscheibe auf den Rücken gemalt. Die aktuellen Daten zeigen nämlich ein explosives Setup: Eine gigantische Wand aus Short Positionen hat sich aufgebaut. Sollte Bitcoin die Marke von 80.500 $ erreichen, werden Wetten im Wert von 5,7 Milliarden Dollar zwangsliquidiert.

Das wirkt wie ein Magnet für die Market Maker: Dort liegt das Geld, dort will der Kurs hin. Ein klassisches Setup für einen brutalen "Short Squeeze".

Glaubt ihr, wir holen uns die Bären in der nächsten Woche? 👇

Deutsch

Misscrpyto📉📊🚀 retweetledi

🚨 FOBO ist das neue FOMO: Warum Software Aktien gerade crashen!

Vergiss die Angst, etwas zu verpassen. Die Wall Street hat jetzt FOBO, "Fear Of Becoming Obsolete" (Angst, überflüssig zu werden). Ein Blick auf die Liste zeigt tiefrote Zahlen bei Giganten wie Salesforce, Adobe oder HubSpot. Der Grund? Wir erleben gerade den brutalen Wechsel von KI als Werkzeug hin zu "Agentic AI", also KI, die den Job komplett übernimmt.

Anthropic’s neues Modell "Opus 4.6" macht klar: Wenn eine Software nur Prozesse digitalisiert, ist ihr Burggraben (Moat) weg. Sie wird nicht mehr genutzt, sie wird ersetzt.

Ist das der Anfang vom Ende für klassisches SaaS?👇

Holger Zschaepitz@Schuldensuehner

FOBO is the new FOMO. 📉 Fear Of Becoming Obsolete is ripping through the software sector. We are moving from "Generative AI" (tools) to "Agentic AI" (replacements). If your SaaS product just digitizes a process, Anthropic’s Opus 4.6 just made you vulnerable. The "moat" is gone.

Deutsch

Misscrpyto📉📊🚀 retweetledi

Wusstet ihr eigentlich, dass es dieses XRP Tool gibt? 🤔

Viele wissen gar nicht, dass ich im Hintergrund an einer Art "Schweizer Taschenmesser" für z.B. XRP Investoren gebastelt habe. Ab sofort stelle ich euch hier immer mal wieder eine Funktion vor.

👉 Hier geht's zum Tool: misscrypto.de/xrp

Heute im Fokus: Der XRP Master Hub 👇

Vergiss langweilige Charts. Hier sind die Features, die wirklich Spaß machen:

- Richlist Check: Gib deine Anzahl ein und sieh sofort: Bist du noch "Plankton", schon ein "Dolphin" oder gar ein "Whale"? (Vergleich dich mit 7,8 Mio. Wallets!)

- Potenzial Rechner: Was ist dein Portfolio wert, wenn XRP das Allzeithoch knackt oder Gold-Marketcap erreicht?

- Live Burn Monitor: Sieh in Echtzeit, wie XRP für immer vernichtet werden.

- Escrow Timer: Wann werden die nächsten 1 Mrd. XRP freigegeben?

Probier es mal aus und sag mir, welchen "Rang" du auf der Richlist hast! 😉👇

Deutsch

Misscrpyto📉📊🚀 retweetledi

US Arbeitsmarkt crasht auf Rezessions Niveau! (Schlimmer als 2001?) 😳

Vergiss das "Soft Landing" Gerede, die neuen Daten sind ein echter Schocker. Die offenen Stellen in den USA sind auf 6,5 Millionen gefallen. Das ist nicht nur der tiefste Stand seit 2020, sondern liegt sogar unter dem Niveau vor der Pandemie (2018/19).

Warum das so gefährlich ist: Das Verhältnis von offenen Stellen zu Arbeitslosen ist auf 0,87 gerutscht. Im Klartext: Es gibt jetzt offiziell mehr Arbeitslose als Jobs.Dieser Wert ist sogar schlechter als während der Rezession 2001! In nur zwei Monaten sind fast 1 Million Stellen verdampft. Die Schwäche am Arbeitsmarkt beschleunigt sich also.

Der Arbeitsmarkt war bisher die Stütze der US Wirtschaft. Wenn diese wegbricht, wird eine Rezession extrem wahrscheinlich.

The Kobeissi Letter@KobeissiLetter

US job openings are now at recession levels: US job openings dropped -386,000 in December, to 6.5 million, the lowest since September 2020. Over the last 2 months, job openings have declined -907,000, the biggest 2-month drop since March 2023. The number of available vacancies has plummeted -5.6 million since the March 2022 peak. This is now below levels seen before the pandemic in 2018 and 2019, at ~7.0 million. As a result, the ratio of available vacancies to unemployed workers is down to 0.87, the lowest since February 2021, and significantly below the pre-pandemic high of 1.24. This is also below the levels recorded during the 2001 recession. US job market weakness is accelerating.

Deutsch

Misscrpyto📉📊🚀 retweetledi

Du verkaufst 1 Bitcoin, aber das Finanzamt sieht etwas ganz anderes! 👀

Viele denken, sie verkaufen den Coin, den sie gerade erst gekauft haben. Falsch! In Deutschland gilt meist das FIFO Prinzip (First In, First Out). Das heißt: Steuerlich verlässt immer dein ältester Bitcoin das Depot zuerst. Das ist oft dein größter Vorteil! Denn wenn genau dieser "alte" Coin schon über 1 Jahr bei dir liegt, ist der Gewinn komplett steuerfrei, egal zu welchem Preis du heute verkaufst.

Aber Vorsicht: Sobald du Futures handelst oder Coins wild zwischen Wallets hin- und herschiebst, wird es chaotisch. Wer hier nicht sauber trackt, zahlt am Ende drauf.

Hast du deine Haltefristen genau im Blick oder hoffst du einfach nur? 👇

Deutsch

Misscrpyto📉📊🚀 retweetledi

Vergiss den Chart! Während wir auf den Bullrun warten, nutzen 650 Millionen Menschen Krypto längst zum Überleben.

👉 Hier geht's zur kompletten Analyse & den 5 Coins: youtu.be/dTLHjlagke0

Darum geht's: Wir im Westen fragen: "Wann Lambo?". In Afrika lautet die Frage: "Wie sichere ich mein Geld vor 30% Inflation?".

Was wir hier oft übersehen: Für Millionen Menschen ohne Bankkonto ist Blockchain keine Spekulation – es ist die einzige funktionierende Infrastruktur. Das Smartphone wird zur Bank, der Stablecoin zum Sicherheitsnetz.

Im Video zeige ich dir:

- Warum der echte "Banken Exit" gerade in Afrika stattfindet.

- Wie 5 Milliarden Dollar Transaktionsgebühren gerettet werden können.

- Welche 5 Projekte (u.a. Cardano, Ripple, IOTA) dort schon heute reale Probleme lösen.

YouTube

Deutsch

Misscrpyto📉📊🚀 retweetledi

Vergiss den Chart! Während wir auf den Bullrun warten, nutzen 650 Millionen Menschen Krypto längst zum Überleben. 😳

Wir im Westen fragen: "Wann Lambo?" In Afrika lautet die Frage: "Wie sichere ich mein Geld vor 30% Inflation?". Was wir hier oft übersehen: Für Millionen Menschen ohne Bankkonto ist Blockchain keine Spekulation, es ist die einzige funktionierende Infrastruktur. Das Smartphone wird zur Bank, der Stablecoin zum Sicherheitsnetz.

Die brutale Realität, die wir im Chart nicht sehen:

- Milliarden Grab: Jährlich verschwinden 5 Milliarden Dollar in Afrika nur durch ineffiziente Bankgebühren. Überweisungen kosten oft 8-9%. Blockchain drückt das auf unter 1%.

- Bank Exit: 650 Millionen Menschen haben kein Konto. Krypto Wallets (z.B. auf Celo oder via Stellar) geben ihnen erstmals Zugang zur Weltwirtschaft.

Echte Use Cases:

- Cardano: Dezentraler Mobilfunk & Wohnraum.

- IOTA: Beschleunigt Grenzabfertigung von 14 auf 3 Tage. Ripple: Baut neue Zahlungskorridore für Institutionen.

Das ist keine Zukunftsmusik. Das läuft bereits. 👇

Deutsch

Misscrpyto📉📊🚀 retweetledi

Geld Revolution in den USA? Kevin Warsh plant das "Undenkbare"! 😳

Alle starren nur auf Zinssenkungen, aber der kommende Fed Chair Kevin Warsh plant im Hintergrund wohl etwas viel Größeres: Einen neuen "Fed Treasury Accord". Was technisch klingt, könnte die wichtigste Änderung seit den 1940ern sein. Warsh will die Zusammenarbeit zwischen Notenbank (Fed) und Finanzministerium komplett neu regeln, um die explodierenden US Schulden in den Griff zu bekommen.

Ähnlich wie im 2. Weltkrieg (als die Schulden zuletzt so hoch waren), könnte die Fed gezielt eingreifen, um die Finanzierungskosten des Staates zu drücken. Damals hieß das "Yield Curve Control": Zinsen wurden künstlich niedrig gehalten, egal was die Inflation macht.

Sollte Warsh diesen Weg gehen (mehr Liquidität, künstlich niedrige Anleiherenditen), fließt Kapital oft fluchtartig in Risk Assets. Historisch war dieses Umfeld ("Financial Repression") der perfekte Treibstoff für Gold, Aktien und Krypto.

Glaubt ihr, die Fed opfert ihre Unabhängigkeit, um den US Haushalt zu retten? 👇

Bull Theory@BullTheoryio

🚨 IS KEVIN WARSH ABOUT TO FLOOD MARKETS WITH LIQUIDITY OR TRIGGER A BOND MARKET RISK? Recently, the upcoming Fed Chair Kevin Warsh has called for a new FED TREASURY ACCORD, basically a framework that would decide how the Fed and the U.S Treasury work together on debt, money printing, and interest rates. This is not only about rate cuts. Yes, markets expect Warsh to support rate cuts over time, possibly bringing rates down toward the 2.75%–3.0% range. But the bigger story is what happens behind the scenes. Warsh has long argued that the Fed’s massive balance sheet, built through years of bond buying pulls the central bank too deep into government financing. So his plan could involve: - The Fed holding more short term Treasury bills instead of long term bonds. - A smaller overall balance sheet. - Limits on when large bond buying programs can happen. - Closer coordination with the Treasury on debt issuance. And this is where history matters. Because the U.S. has already done something very similar before. During World War II, government debt exploded from about $48 billion to over $260 billion in just six years. To manage borrowing costs, the Fed stepped in and controlled interest rates directly. Short-term yields were fixed near 0.375% and Long-term yields were capped near 2.5%. If yields tried to rise, the Fed printed money and bought bonds to push them back down. This policy is known as Yield Curve Control. It helped the government borrow cheaply during the war. But it came with consequences. Once wartime controls ended, inflation surged sharply. Real interest rates turned negative. And the Fed lost independence over monetary policy. By 1951, the system broke down and the famous Treasury Fed Accord ended yield caps. Now fast forward to today. U.S. debt levels are again near World War II levels relative to the economy. Interest payments alone are approaching $1 trillion per year. Even a small drop in long term yields would save the government tens of billions in financing costs. That fiscal pressure is why Warsh’s proposal is getting so much attention. Other countries also tried something similar. - Japan ran yield curve control from 2016 to 2024. Its central bank ended up owning more than 50% of government bonds. Yields stayed low, but the yen weakened and bond market liquidity suffered. - Australia tried a smaller version in 2020–2021. When inflation surged, they were forced into a messy exit that hurt central bank credibility. Across all these cases, the pattern was similar: Borrowing costs stayed low. Liquidity stayed high. Currencies weakened. Exits were difficult. If Warsh’s framework leads to lower real yields, rate cuts, and easier liquidity conditions, that usually supports risk assets like equities, gold, and crypto. Because when bond returns fall, capital looks for higher-return alternatives. But bonds themselves could face volatility. Less Fed support for long term yields combined with heavy Treasury issuance could steepen the yield curve and push term premiums higher and that's why this could become the most important structural shift in U.S. monetary policy since the 1940s yield curve control era.

Deutsch