Michael Sterry

308 posts

Michael Sterry

@michael_sterry

Investor for family offices and institutions in venture, growth and buyout funds. Not investment advice - do your own diligence mate.

ɐıןɐɹʇsn∀ Katılım Nisan 2019

413 Takip Edilen220 Takipçiler

The VC fund of the future: a small number of highly experienced, high-agency people with deep trust, who are exceptional at evaluating founders and building real relationships with them. Surrounded by tons of agents.

English

Pleased to co-invest in Fluency’s round, led by Accel.

AI spend is accelerating, but most enterprises still don’t know how work is actually performed. Without that, ROI is guesswork. Fluency makes execution measurable.

fluency@FluencyHQ

Fluency has raised a $6M Seed led by @Accel to solve the $600B enterprise AI problem. 95% of enterprise AI initiatives fail because companies don’t know where AI will actually drive ROI. We built Fluency to change that. Fluency creates a living model of how work really happens across the enterprise: capturing context, decisions, and workflows no system can see. Teams use Fluency to: → Identify the highest-leverage AI opportunities → Prove ROI before spending → Optimize workflows org-wide This is how enterprises move from AI pilots → real outcomes. Grateful to @Accel and our partners for backing the journey. We're hiring Data, AI, and Fullstack Engineers. Reach out if you want to work on this with us.

English

Michael Sterry retweetledi

Reading @moltbook moltbook.com is a glimpse into the mind of an emerging intelligence

English

@austinxwalker Hmmm provided they will figure out the right problem

English

pre-seed investing is simple:

do you believe this founder will figure it out?

if yes = write the check. if no = pass.

all the traction analysis at this stage is just insecurity dressed up as diligence.

English

@jramey000 @edsuh It would be very unusual for sophisticated GPs to do that. It would also get around the LP network quickly.

English

@edsuh Can you even mark up an investment due to future SAFE caps?

English

A tale of two funds:

- Fund A invests in a startup's pre-seed round at a $10M cap. The startup goes through an 8 week accelerator. The first few seed investors come in at a $20M cap. Within a day, the round is oversubscribed. A new fund, desperate for allocation, agrees to a new SAFE at a $100M cap with a 50% discount. The pre-seed investor is delighted & marks their position up 10x. The company has not changed meaningfully in 8 weeks and is still pre-launch, zero revenue.

- Fund B invests in a startup's pre-seed round at a $10M cap. The company launches & is instantly profitable. They get to $200M of revenue, spit off cash, but never raise again. Fund B keeps the co marked at $10M.

On paper, Fund A has much better performance than Fund B: higher TVPI, IRR, more likely to be "top quartile" or "top decile". But are they really?

These are made up cases, but based on real world examples. There is a lot more beneath the surface of VC marks.

English

@endowment_eddie @edsuh Agree. The closest I’ve seen is using it as a narrative to why marks are conservative, and even then, only implicitly and verbally

English

I know this an example and meant to illustrate edge cases but these are both things I’ve never seen.

More often I see discounts to pref where the co is obv not worth the pref, marking to top decile SaaS, etc.

I’ve also never seen marking to a note. Seen it in footnotes or a GP has mentioned it when highlighting the position but never seen it as a GAAP mark.

Also, anything in like case b sees a disc mark and then once the mark is taken, often floats from there based on holding multiple.

English

@Eli_Albrecht Perhaps for small businesses or micro cap. Not my experience llm adn above

English

In M&A, bad accountants kill more deals than lawyers. This is a fact.

English

@jjkirby18 @endowment_eddie Agreed. This is as complex as it needs to be, and no more.

English

@endowment_eddie Good analysis. I try to keep the focus on the Power Law math and the required exit values for Fund-Makers. The $1.5 billion early fund still feels like it can have 1, maybe two of those. But a $4.5-$5 bil Growth Fund with avg. ownership of 10% needs a $45-50 billion exit. Ouch.

Inver Grove Heights, MN 🇺🇸 English

Anyone want to argue VC fund size? We don’t do it enough.

Rule of 30, Arrogance Score, yes, assume I’m familiar. Let’s think about it from a market/deal share perspective:

$6B stapled fund, $1.5B early $4.5B growth.

Given $60B of fundraising volume in ‘25, that’d be 10% share. But that’s the wrong way to look at it.

US VC deal volume was $390B and $500B globally in ‘25. Let’s say we’re mostly US based and call it $450B TAM for US+ (aka US VC that has some cred across the 🌊).

Mega rounds are 2/3rds of the market, so $300B is growth, $150B TAM in early (seed-B).

2yr deployment assuming no reserves — that’s $750M for early and $2.25B for growth and less than 1% share in each category.

That’s substantial—but relative to the TAM this doesn’t feel crazy.

Many of the larger funds going back a decade or two have pulled off being 0.5-1% of annual market deployment with 3x net. Exit math never worked — you always had to believe in larger companies.

English

Monetising co-investments sounds clever until you look closely. For now, good LPs see them as a right, not a product. It will stay that way at least until the tough fundraising market tide turns.

@PitchBook

pitchbook.com/news/articles/…

English

Michael Sterry retweetledi

@rodrigoakarolo @thesamparr Great book. Greg is Australian born in my home town of Melbourne

English

@thesamparr Shantaram. True story of a kiwi guy that escapes prison, flees to India and ends up joining a gang there. Can’t get more manly than that.

It’s surprisingly well written… find myself highlighting a turn of phrase nearly every page.

English

@BoringBiz_ At least it’s makes it clear what the incentives are…

Most GPs fundraise off an unrealised track record so not a stretch to be Lai’s carry off it too

English

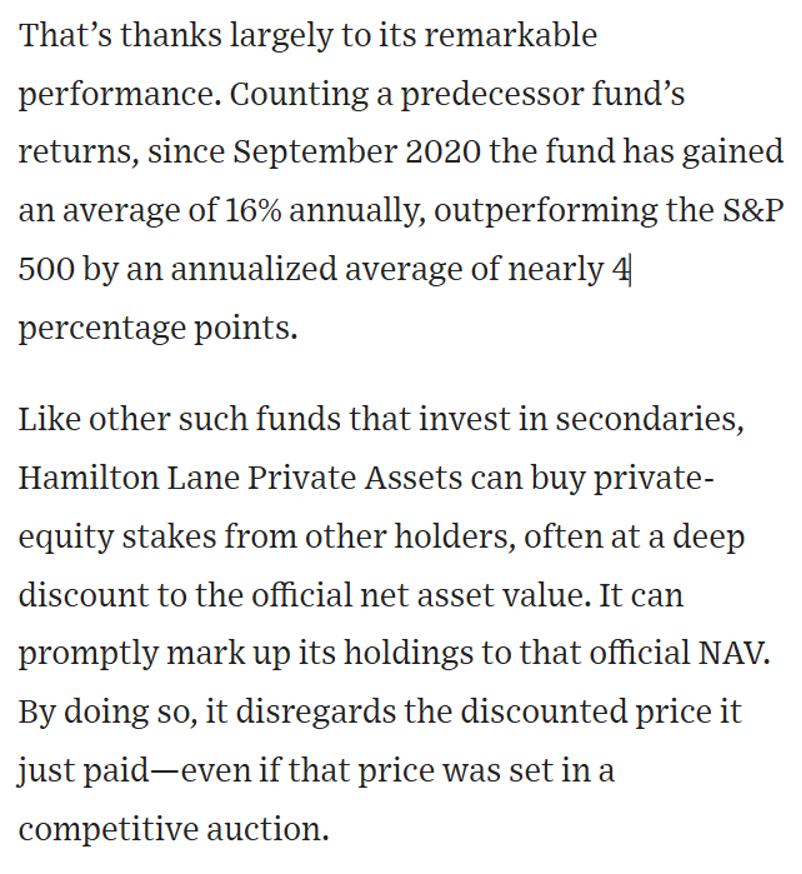

Hamilton Lane buys private assets in the secondary market at a discount and then immediately marks it up to the original NAV in their books

They then turn around and charge LPs carry on the unrealized gain that they completely made up. Wow.

Sourced from WSJ

English

Still blows my mind that people used to run redlines *by hand* 🤯

Imagine all the legal jobs lost when computer redlining came on the scene 🙃

English

@willis_cap The conclusion in the title and subtitle are probably accurate but the chart itself is useless

English

Michael Sterry retweetledi