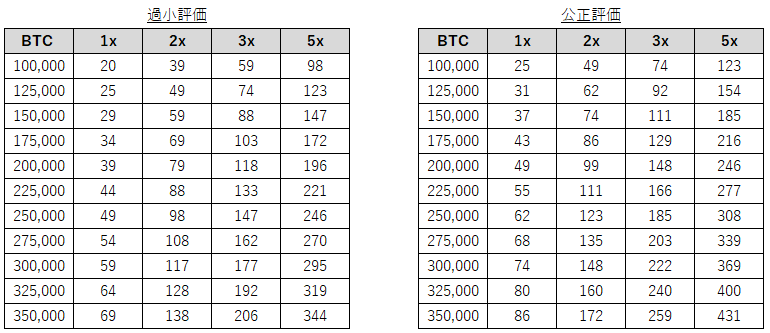

Per @jpmorgan SOTP valuation metric, @MARAHoldings HODL alone is worth almost $2BN more than $MARA's market cap - with no value being given ascribed for mining operations As we kick off the New Year, I’ll be sharing insights into $MARA that the market may be overlooking as part of our #MARAInsights series. Today, I will focus on the value of our #bitcoin reserves. As the largest publicly traded Bitcoin miner, $MARA leverages a hybrid strategy of mining and strategic BTC purchases funded by 0% convertible notes to grow BTC/share. In 2024, $MARA: - Mined over 9,000 BTC at a discount to the spot price. (~$67K cash cost per coin in 3Q24) - Acquired over 22,000 BTC via direct purchases and 0% convertible notes at an average price of ~$87,000/BTC. - Achieved a YE BTC yield per diluted share of 62.7% - Had ~7,300 BTC loaned to third parties (some of the most trusted crypto participants), generating additional returns. As of 12/31/24, $MARA holds ~45,000 BTC, valued at ~$4.2B. Applying @jpmorgan's SOTP valuation metric of 2X HODL premium, this translates to an estimated value of ~$8.4B. For context, $MARA's market cap as of 1/3/25 is ~$6.7B, yet @jpmorgan's BTC valuation multiple implies our bitcoin holdings alone could be worth $8.4B. This figure represents only $MARA's bitcoin holdings, with zero credit given to our mining operations, vertically integrated tech stack, or expanding technology business. In tomorrow's post, I’ll discuss @MARAHoldings meeting and exceeding its 2024 EH/s target. Stay tuned.