Sabitlenmiş Tweet

m4n

5.9K posts

m4n retweetledi

English

according to grok, the outstanding shares was 80-117M that day.

April 19th 2023

This was during the final meme-stock frenzy for the original Bed Bath & Beyond (ticker BBBY, later BBBYQ).

On that date, over

900 million shares traded hands—extraordinarily high compared to the ~80–117 million shares outstanding at the time

(implying multiple turnovers of the float, with heavy off-exchange/dark pool activity)

Now here is the real question, as retail owned 96.9% and not many sold so how could you have this volume?

GIF

English

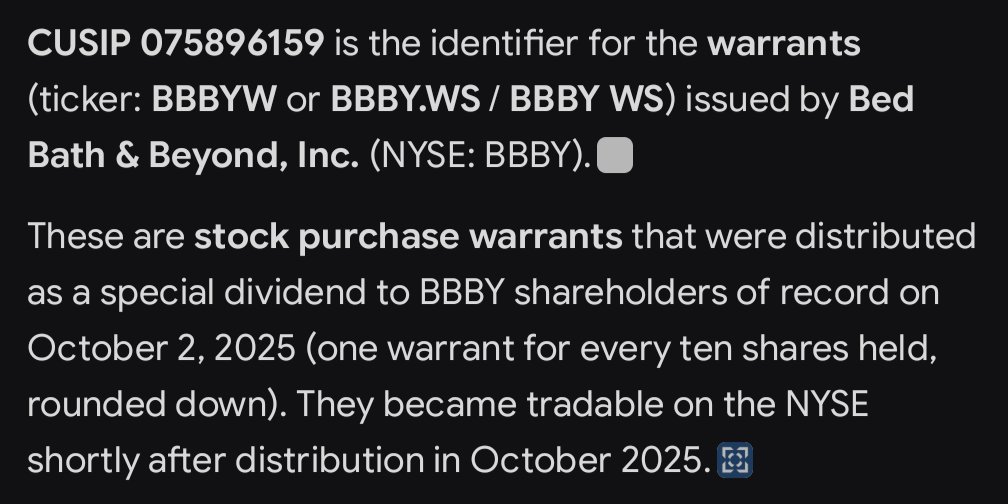

@sneak_69420 @Giggle_Pufff different CUSIPs, different entities

BBBY → 690370

BBBYQ → 075896

English

@create_q @Giggle_Pufff yes they did, check the CUSIP root number and how it is different to overstock/bbby

English

@mo4nothing @Giggle_Pufff BBBYQ never issued any warrants dude

English

m4n retweetledi

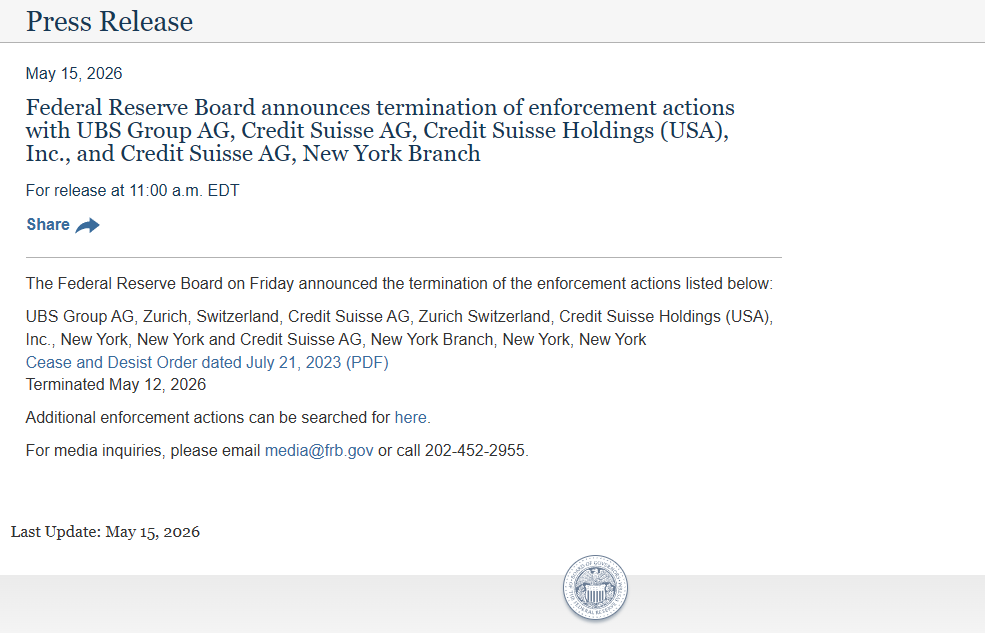

As a parting gift from Jerome Powell's Fed, they've announced as of May 15th, that its terminated enforcement actions with UBS Group AG and Credit Suisse AG (Archegos).

This stems from the "unsafe and unsound" risk management practices that caused Archegos to collapse.

And now they're off the hook. Puzzling. Or rather, troubling.

English

English

China talks didn't go well?

Crypto Rover@cryptorover

ABSOLUTE BLOODBATH IN US MARKETS 🩸 Almost $1 TRILLION has been wiped out in just 5 minutes after the market open.

English

m4n retweetledi

m4n retweetledi

m4n retweetledi

Un padre abraza a su pequeña hija, que es una mártir, como si estuviera abrazando su corazón que ha dejado de latir. Última despedida, último abrazo.

No ignores lo que sucede en #Gaza no dejes de compartir 🙏 y difundir 👇🇵🇸 🍉😥

Español

m4n retweetledi

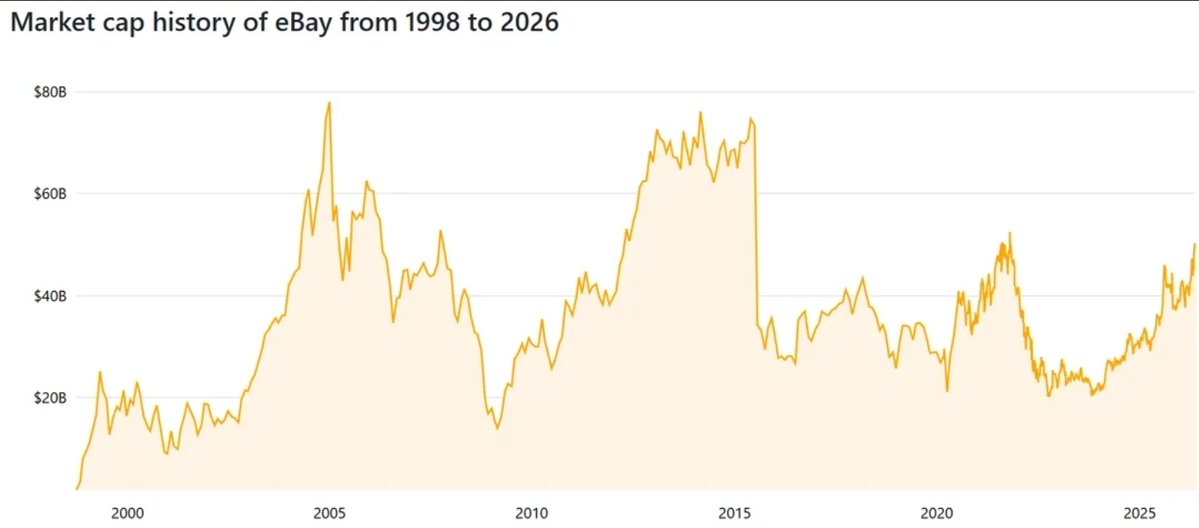

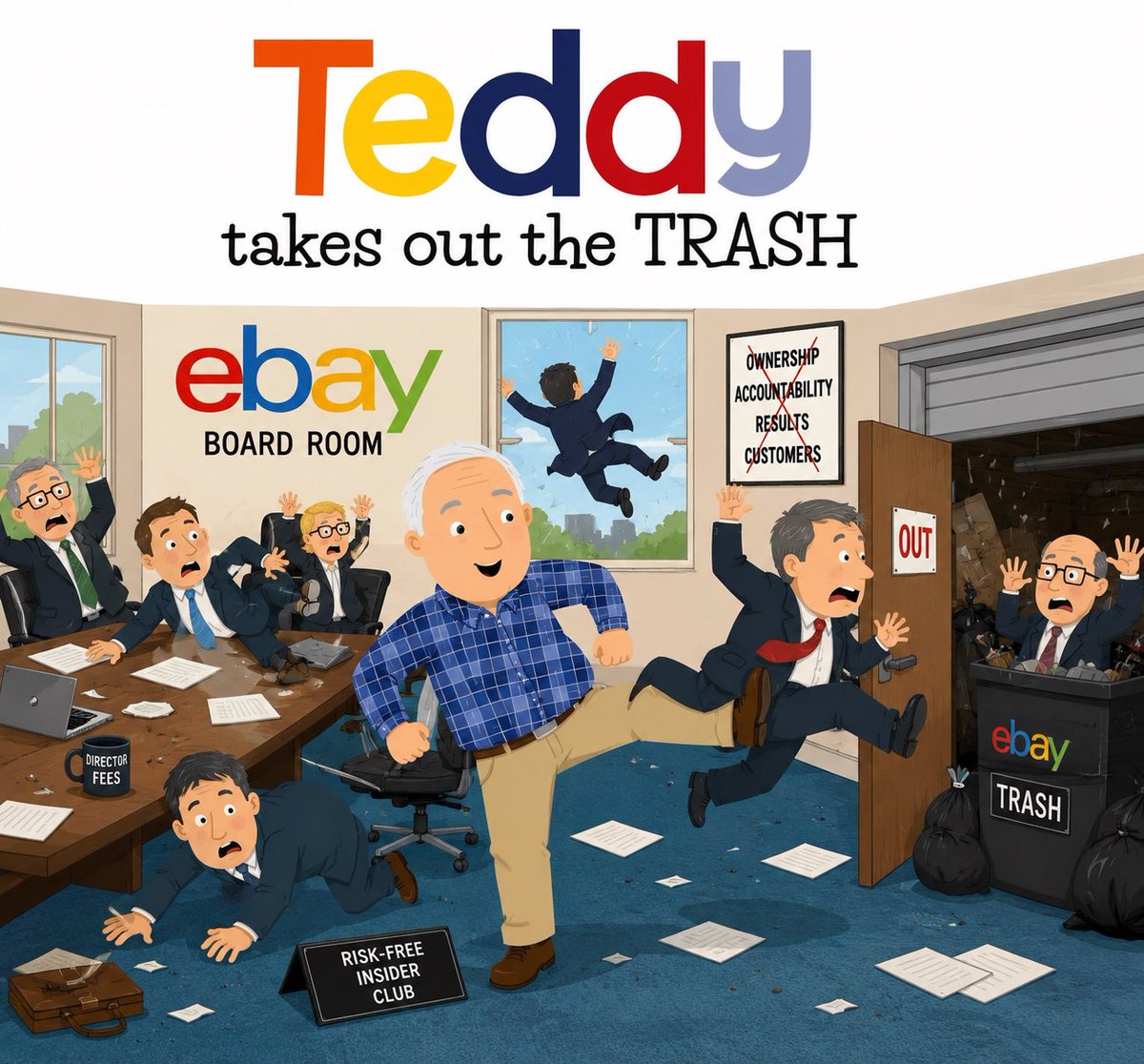

Despite the eBay board stating their strengths and performance in rejecting GameStop's acquisition offer, the historic market cap says otherwise.

While Amazon thrived post pandemic, eBay dwindled in market cap and the board became lazy, complacent and obese.

cc @ryancohen

English

m4n retweetledi

Ryan Cohen has 24 hours to accept or reschedule the interview🤝

My DMs are open @ryancohen

x.com/i/spaces/1dJrP…

English

m4n retweetledi

🚨 UPDATE: 19 MILLION exposed NGINX instances hit by the 18-year-old NGINX RCE found by AI.

Top exposure by country:

- United States: 5,340,011

- China: 2,540,008

- Germany: 1,871,780

Note on ASLR as added security: not all of these instances will have ASLR disabled, but every one of them is running a version inside the vulnerable band.

The vulnerability is a heap buffer overflow. ASLR randomizes memory layout, which makes reliable RCE much harder because the attacker cannot predict where their payload or useful gadgets land. But the overflow itself still happens. The corrupted memory still causes the NGINX worker process to crash.

ASLR-enabled hosts are still trivially DoS-able. ASLR-disabled or non-PIE builds are RCE-able. Either way, patch ASAP!

International Cyber Digest@IntCyberDigest

‼️🚨 MAJOR IMPACT: AI just found an 18-year-old NGINX critical remote code execution vulnerability. It has been disclosed on GitHub including PoC code. - Affects NGINX 0.6.27 through 1.30.0 - Triggered via the rewrite and set directives in config - Update NGINX ASAP - NGINX is a widely used HTTP web server, be sure to check its prevalence in other products

English

m4n retweetledi

m4n retweetledi

eBay has rejected @ryancohen's bid for the company.

Ryan says the fight is not over.

The $GME CEO is playing to win.

Anthony Pompliano 🌪@APompliano

FULL INTERVIEW: @ryancohen explains his plan to acquire eBay. He unpacks his pitch to institutional investors, why eBay is so horribly run, and how Ryan plans to create billion in shareholder value. $GME $EBAY

English

m4n retweetledi

FULL INTERVIEW: @ryancohen explains his plan to acquire eBay.

He unpacks his pitch to institutional investors, why eBay is so horribly run, and how Ryan plans to create billion in shareholder value.

$GME $EBAY

English

English

@Valueinvest2099 @rnewton7777 This is just assuming GME + eBay at the terms found in the (rejected) offer made by RC

English

I asked last week,

How do you price this? (eBay + GameStop)

There are a lot of models you can try to build but ultimately I think it only really matters for me if I capture Wallstreet's sentiment. Because as I wrote in some longwinded post a few weeks back, they will have an algo parse the filing on deal close and "price" the deal by selling it to that level in the extended market when we can't trade. We have seen this repeatedly lately, that's how this whole thing works.

So my model will essentially be wrong automatically because I don't know how the street models these things precisely. And they will absolutely pin the price immediately to what they think is "fair value," via sell action. Then as new details emerge and quarterly progress on optimization and such happens, they'll evaluate the balance sheet and price it again. And again. And again.

For anybody that watched my videos, they must laugh, because in 2022 I was so optimistic all the time. Then I watched them price it to $10 and I was humbled. I simply didn't know how aggressively they could price a target down. And so I learned a measure of respect. But then I got excited again and bought in the 30s when Roaring Kitty came back and was re-humbled when we got priced back to the teens.

And even with all our balance sheet improvements, our fortress of cash, our operational profit, and our collectibles pivot, I was re-humbled again in late November and December twice. Again, back to the teens.

Does it mean we are destined to always price back to the teens? No, it simply means somebody felt compelled to price the stock down for whatever reason. Maybe they sensed weakness. Maybe there was sell side pressure post warrant issuance. Maybe options interest collapsed post Q3 earnings. I don't exactly know why we mark down so badly sometimes or mark up so much other times.

So I don't know the model to even use today on GameStop even though I recently said I like knowns and feel I know current dog-form version GameStop.

So how can I model a totally new thing? I know I'll mess it up just like I messed up cash per floor several times and still don't feel super confident in it today.

So for the time being I'm not settled on any particular model. I see the word accretive thrown around a ton. This deal could work out to be accretive in the sense that per share value could go up over the long term, yes. eBay has value that can be unlocked at scale, so the shareholder value would spill over to us as GME holders post deal optimization period.

Does that mean it moves in a straight line? No.

Could we compress back to some mark down that represents paying for eBay at premium + cash drag on 20b in loans + unoptimized eBay? Seems likely to me.

What's the mark down look like?

How fast could Cohen unlock value, deleverage, etc?

Well a very simple model would be something like this,

Imagine he does de-leverage the 20b loan very quickly. If the combined company has 1.6b shares (even that is unknown), simple division shows:

$20,000,000,000 / 1,600,000,000 =

$12.50 dollars per share

That means if Ryan Cohen and leadership can cost cut super fast, pour operation profit into the loan and pay the balance down, liabilities drop off by $12.50 a share. That's what he means by "not running it hot." That's what I personally mean by paying off your mortgage as fast as possible. Leverage and margin are terrible. That's why eBay leadership doesn't want this deal right now. $20 billion financed at 7 or 8% corporate rate is enormous drag on profitability that they don't currently have.

But again, if he can work magic and pay it off very quickly, Assets - Liabilities = Shareholder Equity.

Drop liabilities by $20 billion and you immediately increase shareholder equity by $20 billion or $12.50 a share.

So while I don't know the immediate post deal compression price, I see a post leverage price as +$12.50. Because that's just basic mathematics. And that is certainly accretive. Because increasing share price on GameStop by $12.50 for leadership is significantly harder right now. That would take something like 5-10 years at current rate using a fundamentals analysis. There just isn't any fat left to cut and while we are making $600m a year or whatever, 600/488 = $1.23 a year.

But post deal, to me, looks ugly. People want to do models like:

GME $11b Market Cap + EBAY $55b = $66b

Doesn't work like that.

or,

GME $23 a share + EBAY = X

Doesn't work like that.

You have to do it how the street is doing it and they'll use some formula based on revenue, earnings, assets, liabilities, etc.

And the deal burns our assets.

The deal burns our earnings (loan coupon).

The deal burns our shareholder equity.

The deal likely adds something like $25 billion or more in Goodwill to the balance sheet because otherwise shareholder equity would actually be negative.

And I am not a fan of goodwill. It is why GameStop was overvalued when it was recklessly acquiring bad companies in 2014 and why it got marked down so badly when they dropped all the goodwill in 2019 or so.

Goodwill is, imho, nonsense financial wizardly meant to make assets - liabilities = shareholder equity still make sense on paper when it simply doesn't because of destructive acquisitions.

Not to say this is a bad deal, not at all. It is a fine deal if and only if Ryan Cohen can land it at the stated price or better and immediately extract at least $20 billion in savings to de-leverage. Because that right sizes the balance sheet, makes the phantom $12+ in goodwill share value real and protects our downside.

I watch tickers all day where stocks trade at 100 PE or 10 PE. Sure, the street could love this deal, ignore the goodwill, and send this thing (up).

But I don't know how to model that either. I don't know the rationale for why they send some stocks and not others. For example, Best Buy is trading in the gutter but the balance sheet is fine. Shareholder equity is fine. It isn't in any sort of fiscal distress. But it is out of favor, so it trades at a very low multiple. Meanwhile, name any other stock right now and it might have negative EPS, negative shareholder equity, and be weeks from insolvency, but trading at 40 PE. Why? No clue.

So on this one, I have to assume for the immediate term, as much as GameStop would now be 75% eBay 25% GameStop, it would trade post deal a bit out of favor still. Because for whatever reason, we trade as an underdog. How badly do they compress it? Do they respect goodwill or simply ignore it? Do we trade at 30b market cap or 40? Or 50?

You can build 20 different models and they will all sound great on paper. Then you'll wake up in the pre market and be trading at 16.50 or 21.50 or 32.50 and be like, Oh obviously. But it really isn't obvious at all, it is totally subjective. And the player with all the ability to price it, all the economic leverage in the world, is going to apply some model to it that is totally different than Best Buy or PayPal or whatever and they'll have all the logical reasoning for whatever it is they do.

And we'll just be a leaf on a river wondering why we couldn't see where we were going.

So it isn't that I can't price the post deal. I can. 20 different ways. And all of them will be wrong. So do your own modeling however you want, read others' models, and be skeptical of them all.

Because at this point we don't even know the final terms.

Assuming the deal closes, and I honestly believe it will, just in a long while, because closing on a house takes a long time let alone a 55b company,

Is $125 per eBay share the final accepted offer?

50% cash still?

20b in debt? At what coupon (interest rate)?

50% stock still?

At what conversion?

And is there any other angle we're missing here?

Suppose, just for the sake of pure hopium, Cohen has outside backing in the form of a large institutional presence that wants to do a block equity finance deal where they take something like a $20b interest in the new company via common or preferred stock. Well that changes everything immediately. And that isn't altogether that unrealistic.

So it is very hard to model this right now. Be careful but have fun with it. Will it immediately send the stock? Very hard to say. But it certainly gives room for immediate upside improvement via debt paydown. And I do like that along with the other things Ryan Cohen is talking about. Because right now upside movement from a fundamentals perspective, on GameStop's balance sheet, is not bad, it is just slow. This could be fast and people want fast. But it could be volatile... I just hope people understand why.

English

m4n retweetledi

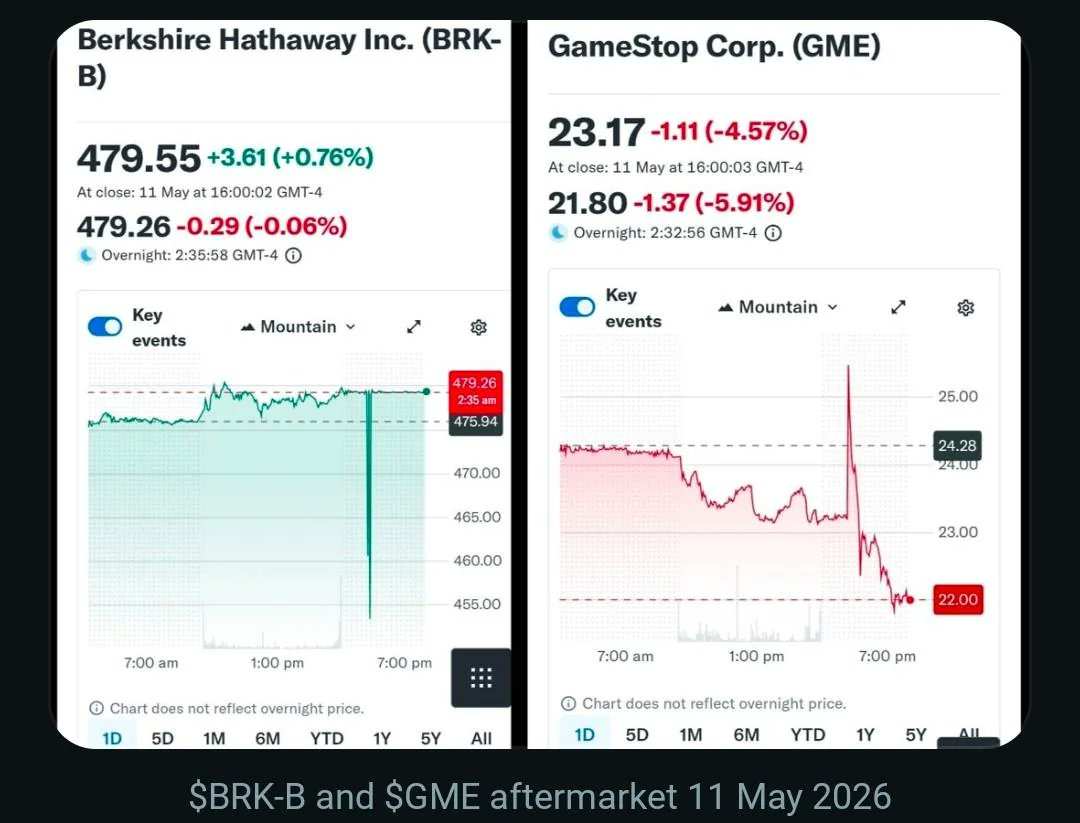

🚨 Here's something wild: right when Roaring Kitty got hacked, GameStop spiked and Berkshire dipped at basically the exact same time!

It's one more piece of proof that the toxic swap is real! $BRK is straight-up inversely correlated with $GME 🤯

Sneed@sneedweb

🚨 $GME TOXIC SWAP THREAD: The January 2021 Squeeze NEVER Ended. Here's the FULL Proof It's Still Alive in 2026 (and why MOASS is inevitable) 🔥🧵

English

m4n retweetledi

m4n retweetledi