Peter Warren

2.1K posts

@CoinMarketCap Bernstein is right: yield on reserves changes the stablecoin game entirely. Circle wins short-term. But the real shift is when yield passes to users, not issuers. That's DeFi's next frontier. $300B supply is a milestone. Who keeps the yield is the war.

English

LATEST: 📊 Bernstein says the CLARITY Act’s yield compromise favors Circle’s float-income model as stablecoin supply climbs above $300B.

English

@ABC Kid Rock in the second seat navigating the plane that made contact.

English

All four air crew members "successfully ejected" after two jets crashed in midair during an air show in Idaho, the Navy said in a statement Sunday, adding that the crew members were being "evaluated by medical personnel." abcnews.link/t2OTYZM

English

@Soaringeagle45 @X please don’t algo me more of this because I made the mistake of clicking on it

English

Let’s enjoy the day!!!

🤣😂🤣

COLLIERVILLE MOM DETAINED AFTER ALLEGEDLY OPENING “SIDELINE SANGRIA STATION” AT YOUTH SOCCER GAME

COLLIERVILLE, TN — Parents arriving at Rose Soccer Complex Saturday morning expecting Capri Suns and awkward small talk instead found what witnesses described as “a full-blown brunch winery experience with shin guards.”

38-year-old Brittany Calloway was reportedly escorted from a U-9 girls soccer game after allegedly setting up a folding patio bar beside Field 3 and selling “small batch mom juice” out of a monogrammed cooler during the first quarter.

According to witnesses, Brittany arrived at approximately 8:12 a.m. wearing oversized sunglasses, a floppy beach hat, and a shirt that read “IT’S CALLED SELF-CARE, KEVIN.” She allegedly unloaded a collapsible table, two fake ferns, and a handwritten drink menu from the back of a white Tahoe with a “Powered By Pinot” sticker on the rear window.

Authorities say the menu included:

• “Collierville Cabernet-ish” — $9

• “Minivan Moscato” — $11

• “Pinot Grigio & Childhood Trauma” — $13

• “Ref Whistle Riesling” — $15

• A complimentary refill for any parent whose child got put in as goalie “for character development”

Police say Brittany also had:

a battery-powered blender,

a ring light,

a Venmo QR code taped to a pumpkin spice candle,

and a Bluetooth speaker blasting early-2000s Kelly Clarkson on repeat.

One father told officers, “I honestly thought she was part of the tournament sponsorship.”

Another parent reportedly became concerned after her daughter asked, “Why does Chloe’s mom have a happy hour menu next to the orange slices?”

When approached by officers, Brittany allegedly insisted she “wasn’t technically selling alcohol” and claimed parents were simply “donating toward emotional recovery.”

“She was incredibly committed to the theme,” one officer stated. “She had punch cards. She offered us a loyalty program called ‘Sip Happens.’”

Witnesses say Brittany remained calm while being escorted away, though she allegedly attempted to hand out one final mason jar labeled “Silent Carpool Sauvignon.”

Despite the interruption, the Collierville Lady Fireballs went on to win 5-2, although several parents admitted they had absolutely no idea what the score was by halftime...

English

@Osinttechnical Can we get Kid Rock into one of these air shows?

English

Footage of the mid air collision between a pair of Navy Super Hornets/Growlers during the Gunfighter Skies Air Show at Mountain Home Air Force Base moments ago.

English

@TheBetterBull @tomwanhh You’re right, circle is completely content to give them half of everything in perpetuity 🙄

English

@tomwanhh They created USDC together 😂

Meanwhile, CEO Jeremy is mentioning x402 in the comments which is founded by Coinbase

Some of you have surface-level thinking

English

Some early signs Circle <> Coinbase relationship is quietly shifting:

• Circle's ARC token raise did not include CB Ventures

• USYC, Circle's largest tokenized treasury product, is primarily held on Binance and BNB Chain, not Coinbase or Base

• Circle Payment Network does not include Coinbase

Their business lines are converging across blockchain, tokenization, payments and stablecoins. A formal split is unlikely given the mutual benefits still on the table, but the trajectory is clear. Both sides are building toward a less dependent relationship, and the overlap will only create more friction over time.

Omar@TheOneandOmsy

How long until the Circle / Coinbase marriage gets messy? > historically $CRCL = issuer of USDC and $COIN = distributor. Coin pushes USDC, and in exchange gets half the economics w/ some adjustments > but w/ Circle now a pubco, it’s been forced into pitching a much broader growth story to investors -> today that’s become: be the infrastructure layer for global payments + real-world finance onchain > to make that a reality, Circle needs to supercharge itself by owning customers and having their flows live on their new venue, Arc > and the problem is that directly conflicts w/ Coinbase’s own ambition w/ Base to be the exchange + rails for everything, especially payments, settlement & FX > and if you look closely, things have started getting messy: cbBTC vs cirBTC = Circle stepping on Coin’s toes w/ the same product > but Circle / Arc post token raise is a much worse deal. With outside investors underwriting the chain, the incentive becomes drive all your assets + activity from everywhere else (including Base / Coinbase) to Arc: USDC balances, tokenized assets, payments, settlement & eventually FX > the two businesses, which were once symbiotic, are now competing H2H and have public shareholders / token holders to keep track of the scoreboard > inevitable that the relationship ultimately ends in divorce. Circle clearly growing up and planning on moving out of its childhood home

English

Classic DC trash 🗑️

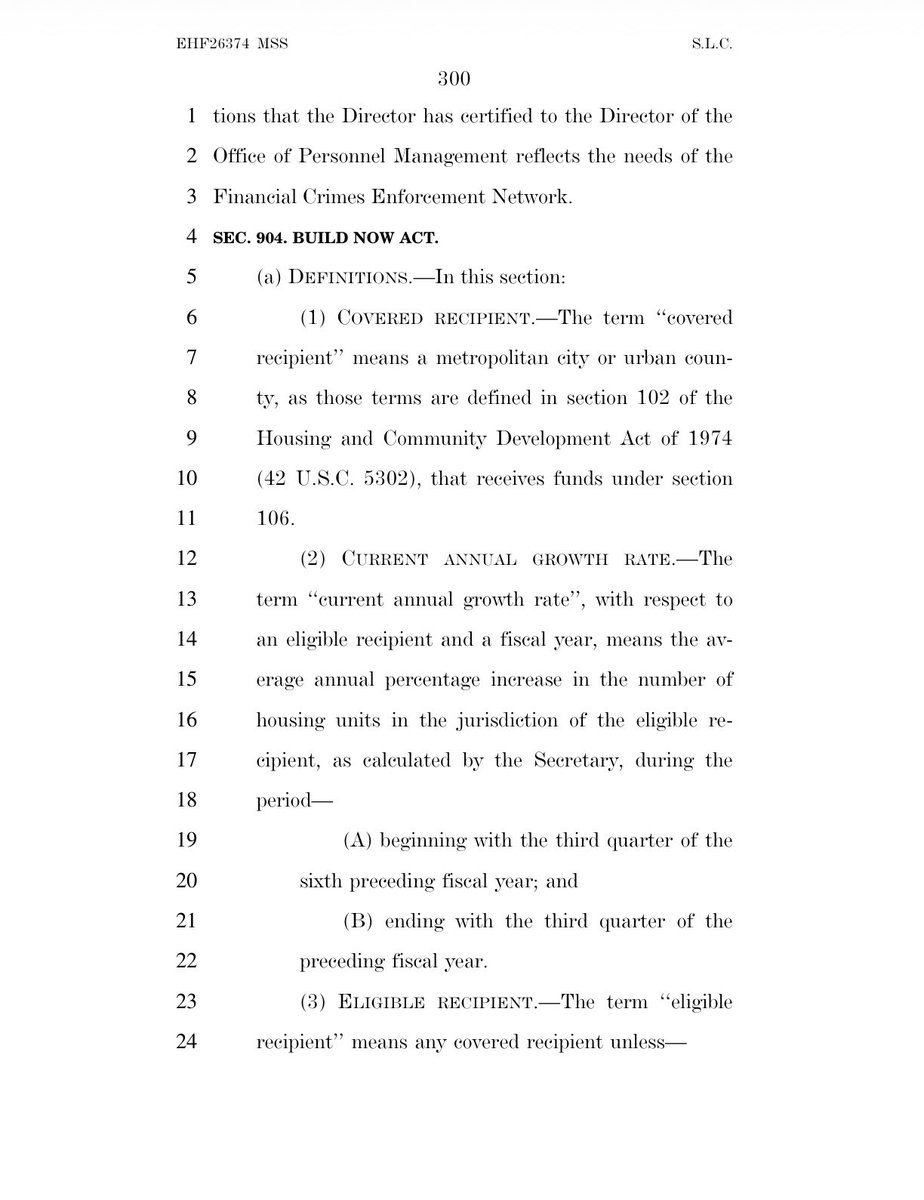

A 300+ page crypto clarity bill quietly drops the entire Build Now Act (pages 300-309) — a standalone housing pilot using CDBG grants to reward cities for building more units. Zero connection to digital assets, stablecoins, or SEC/CFTC rules.

It’s not even subtle logrolling: throw Sen. Kennedy & Warren a bipartisan housing bone so the whole package sails through.

We want real regulatory clarity, not this sausage-making circus. Single-subject bills when? 😤

English

There appears to be a housing bill…inside the crypto bill. 🧐

Pages 300–309 lay out the ‘Build Now Act’ which looks to create a federal program designed to encourage local housing growth.

English

Add circle traces $135, Mizuho analyst Dan Dolev raises price target on $CRCL to $135.00 (from $120.00) while maintaining neutral rating.

That’s 🐓 💩 Dan.

Why not just wait until after Thursday Senate committee vote to be sure you got it right?

English

@AntiTrumpCanada Drowsiness is a known side effect of his Alzheimer’s medication. I’m not even trying to be funny. This is sad.

English

Every fucking time the cameras are on this motherfucker in the Oval Office and he’s not the one talking, he’s falling asleep. EVERY. SINGLE. TIME. The world anxiously awaits his eternal nap. The sooner the fucking better.

English

$CRCL

Was heavily in profit pre earnings. Got liquidated on the scam dump reaction, and now watch sidelined as it soars to new highs.

I love trading

English

@nobraintrader1 @zeroxkyle Haha….ok.

Stablecoins are a fad. Haha.

English

can someone explain why anyone would buy the ARC token if you could buy CRCL

this seems like the pinnacle of the whole token <> equity problem, this time you have a publicly traded stock who owns % of the token

zoomer@zoomerfied

[ ZOOMER ] CIRCLE RAISES $222 MILLION FROM BLACKROCK, APOLLO AND OTHERS IN ARC TOKEN PRESALE VALUED AT $3 BILLION: CNBC

English

What to watch tomorrow.

Wall St expects ~$715M revenue (+11% YoY)

EPS of $0.15–0.18. The EPS step-down from Q4’s $0.43 isn’t collapse — it’s the investment cycle peak, with $570–585M in 2026 opex funding Arc + CPN.

The one number that matters: USDC circulation.

Above $80B → growth accelerating ✅

Below $75B → reserve income under pressure ⚠️

Bull: CLARITY Act clears, CPN grows, Arc Mainnet confirmed.

Bear: Coinbase distribution costs compress margin, reserve yield slipping 4.1% → 3.8%.

24 analysts. 9 Buy · 11 Hold · 2 Sell. Street target $128–130.

Not financial advice. DYOR 🙏

#CRCL #Stablecoins #Crypto #Earnings

English

$CRCL reports Q1 2026 earnings TOMORROW before market open.

Circle is the world’s largest regulated stablecoin issuer. Here’s everything you need to know 🧵

FY2025 scorecard:

Revenue $2.75B (+64% YoY) · USDC in circulation $75.3B (+72%) · On-chain volume $33.3T (+384%) · Adj. EBITDA $582M (+104%) at a 54% margin.

The $70M net loss? Entirely $424M in one-time IPO stock comp. Strip that out and the cash economics are clean.

#CRCL #Stablecoins #USDC

English

@MilkRoad Moat. Moat. Moat.

Nobody’s interested in their castle.

It’s old and drafty.

English

Western Union $WU runs 360,000 active agent locations across 200+ countries and 130 currencies.

About 90% of those are outside the U.S., concentrated in the corridors where banking access is weakest and remittance demand is highest.

What has to exist around them:

Money transmitter licenses in nearly every U.S. state plus equivalent permissions in 200+ countries, accumulated over a century.

(That's a moat)

Milk Road@MilkRoad

Western Union $WU is down 70% from its 2021 high. Wall Street has written it off as a dying remittance giant getting eaten by Wise, Remitly, PayPal, and crypto. Our lead researcher, @moxt_, thinks Wall St is missing the second business growing in the background (bookmark this). Here's what he's seeing: Yes, the legacy retail business is shrinking. Q1 2026 revenue came in at $983M, margins compressed to 13% from 18-19%, EPS missed by 35-40%. That part isn't coming back. But it's one of two businesses on the same network. Digital transactions grew 21% YoY and now account for 42% of remittance volume. Travel money and bill pay revenue grew 24%. Management is guiding 2026 to 5-8% revenue growth and adjusted EPS of $1.75-$1.85, the first growth year after multiple years of decline. Either guidance is wrong, or the stock pice is. $WU runs 360,000 active agent locations across 200+ countries and 130 currencies. About 90% of those are outside the U.S., concentrated in the corridors where banking access is weakest and remittance demand is highest. Which means the moat isn't the agents themselves, but what has to exist around them: Money transmitter licenses in nearly every U.S. state plus equivalent permissions in 200+ countries, accumulated over a century. AML, KYC, sanctions screening, and FX conversion infrastructure across 130 currencies means any new entrant is looking at a 5-7 year build to replicate it. So does this network get more or less valuable when money moves onchain? The rest of the payments industry is voting with their checkbooks... - PayPal shipped $PYUSD. - Stripe paid $1.1B for Bridge. - Visa is integrating $USDC for cross-border settlement. - MoneyGram has been running a USDC off-ramp on Stellar since 2022. USDC settles in seconds, but a recipient in rural Mexico or the Philippines still needs pesos. Somebody has to handle the last mile. WU already does. @moxt_ maps four revenue streams: 1. Off-ramp fees from third-party stablecoins ($70-810M at maturity) 2. Working capital release from $USDPT ($300M one-time) 3. Reserve income on USDPT float ($12-18M recurring) 4. Internal FX/wire savings. Owning USDPT is what turns WU from a stablecoin off-ramp partner into a stablecoin company that happens to own the largest off-ramp network in the world. All of that said... the risks are real. State-by-state stablecoin reserve recognition could stall, crypto-native off-ramp specialists could fragment the opportunity, legacy pricing pressure could outpace the pivot, and ~35% of CMT revenue comes from U.S. outflows, which makes immigration policy a macro overlay. None individually kills the opportuntiy - but two together would. So is the current price of ~$9.20 enough to justify a position, or do the risks dominate? @moxt_ put a verdict on it in his latest Milk Road PRO report... To get his buy/sell verdict and the price levels he's watching, check the link in the first comment.

English

@TheDunkCentral @JakeLFischer Grizz should give them Ja and some croutons. Please. Take him.

English

The Washington Wizards will reportedly consider trading down from the No. 1 pick, per @JakeLFischer

“Winger told me directly that the Wizards will at least consider trading down. He insisted that this is ‘not a savior moment’ for Washington given that the franchise just traded for two former All-Stars in Trae Young and Anthony Davis on top of the slew of recent lottery picks it already has accumulated. He added that, in accordance with Wizards general manager Will Dawkins' prospect evaluations, Washington will not rule out a move downward if Dawkins determines there are two or three players that the Wizards are eager to come away with.”

(Via open.substack.com/pub/marcstein/…)

English

Peter Warren retweetledi

#BREAKING: Velshi: “Republicans in South Carolina advanced legislation to delay that state’s congressional primaries for two months while they draw out of existence the ONLY district represented by a Black House member, the Democratic Congressmen James Clyburn…the same James Clyburn who marched for civil rights in the segregated south, the same James Clyburn who was arrested protesting segregation in the 1960s…”🤦♀️

English

@JohnRoseforTN Haha

Tough like Trump.

Haha

Napper in chief 😴

Haha

English

@CryptoAmerica_ @EleanorTerrett @adam_minehardt @HyperliquidPC I hear you Mr Minehardt. But… I mean, maybe the Trump family should stop with the fraud. 🤷♂️

English

There is a real danger that this becomes a Democratic issue, not just a crypto issue.”

@adam_minehardt, Chief Policy Officer of @hyperliquidpc explains why crypto policy could turn into a partisan flashpoint.

English

Peter Warren retweetledi

I was told that it was an impeachable offense for Sec. Pete to spend time with his sick child.

chyea ok@chyeaok

Unbelievable : The corporations sponsoring Sean Duffy’s 7 month reality TV trip are all regulated by the department he leads. They literally paid him to take an extended vacation from doing his job.

English

English

@ProblemSniper @HeadHun95018230 @Afshar__ @waca_trader You’re right but misused the phrase bro. All good 😂

English

Clarity Act nail in the coffin for #Bitcoin $CRCL $MSTR

English