Neanderthal Respecter

1.2K posts

Neanderthal Respecter

@neanderthalchad

Lambo Maximalist

Katılım Ocak 2022

91 Takip Edilen112 Takipçiler

Neanderthal Respecter retweetledi

you're going to see a lot of crazy degenerate and semi-desperate RWA plays

a lot of it will mostly be some combination of stupid and illegal and people will be asking us lawyers "how can they do that?"

well, they can't, and it won't be sustainable, but they need headlines & need to be 'first'

pay attention to those building for the longer-term

English

@neanderthalchad Not an exaggeration. I know the man in this photo lol

English

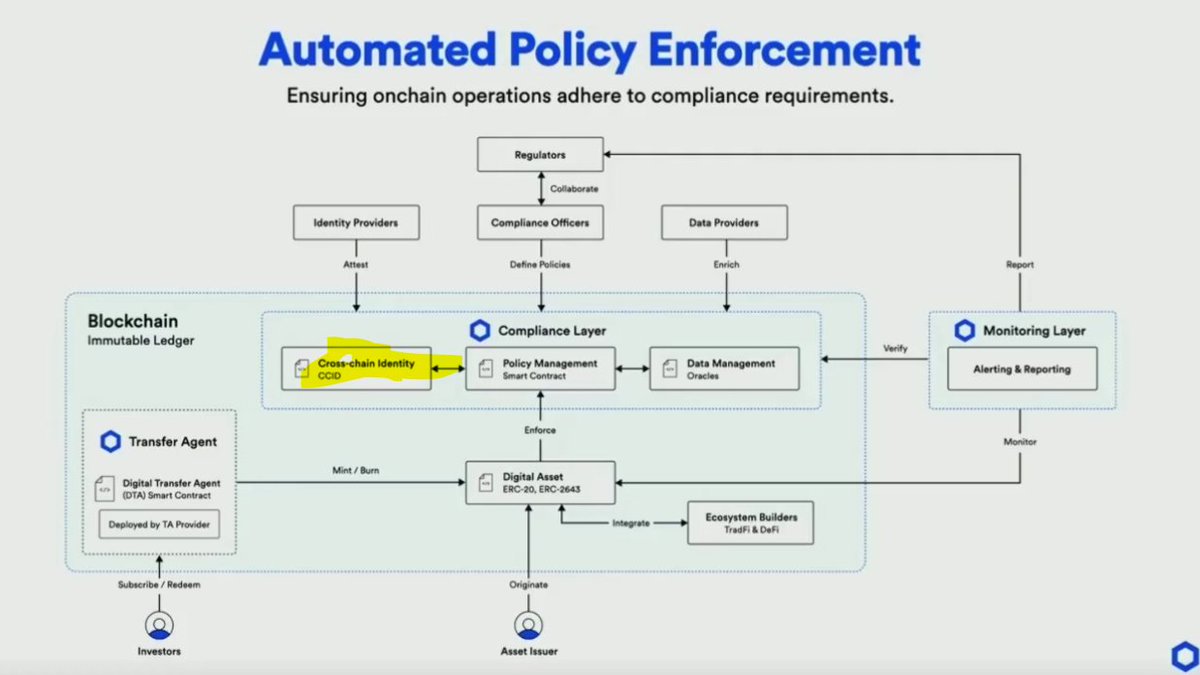

@contractlevel @0xSwish @LinkiesLeaks @chainlink @EverestDotOrg I believe their position is that there isn’t a reason to run it unprofitably, which is unfortunate. Hopefully that changes in the future.

English

@0xSwish @LinkiesLeaks @chainlink @EverestDotOrg Everest aren't running a Chainlink node, when they should have enabled their community to run nodes providing their identity data to Chainlink. It makes no sense. Literally the single most important data to the entire Chainlink network and nobody sees this.

English

Bob Reid conducts an “Ask Me Anything” session with Everest investors (2025)

English

Neanderthal Respecter retweetledi

We are building this future with $LINK. Read the whitepaper: contractlevel.com/whitepaper.pdf

English

Neanderthal Respecter retweetledi

An introductory article on Contract Level Compliance. What is it, why is it, and how does it work?

@contractlevel/introducing-contract-level-compliance-91806137c88d" target="_blank" rel="nofollow noopener">medium.com/@contractlevel…

English

Neanderthal Respecter retweetledi

they told you exactly how it would work with circular value flows right there in the logo

you only have yourselves to blame

Quinn Thompson@qthomp

Can one of the on-chain investigators confirm for me if it is true that the majority of Ondo's TVL, particularly their recent growth, is from the team's selling of $ONDO tokens with the proceeds funneled back into the protocol to give off the appearance of organic growth?

English

Any spooks wanting to move ill gotten gains in a compliant manner should consult @EverestDotOrg

WikiLeaks@wikileaks

Washington DC searches soar for "Swiss bank" (yellow), "offshore bank" (green), "wire money" (red) and "IBAN" (blue)

English

@Tetranode Easily @EverestDotOrg, who are doing some interesting vehicles for companies to raise capital on stockpiles of irl raw materials. They also have tokenized tradfi equities they are waiting to launch pending appropriate regulatory climates.

English

@EverestDotOrg @Viaarpeoficial Impressive first foray into the RWA space for @EverestDotOrg, looking forward to future offerings

English

Congrats to @Viaarpeoficial and the $GEMS community! The first of its kind in the #RWA space 👏👏

GEMS Community@GEMScommunity

💎 Our public sale of $GEMS tokens is now closed with over USD $11,500,000 SOLD 🙌 Thanks to the @GEMScommunity, our institutional clients, and our infrastructure partner @EverestDotOrg for joining us on this exciting journey of tokenizing real #RealWorldAssets!

English

@neanderthalchad @everbased it's time to buy innit

English

Neanderthal Respecter retweetledi

@pmarca another one for your records. @EverestDotOrg 's first de-banking story 🧵:

1/ As a licensed custodian facilitating stablecoin transfers on multiple chains, we needed a US bank account to receive dollars via ACH. After months of discussions, approvals, and API integrations, we were set to launch—but things took a sharp turn.

2/ The process began with detailed "flow of funds" analysis. The bank's compliance team reassured us: "Everest isn't really crypto, so this will be easy." We "program money", and operate more like a digital gift card platform....i.e. accept USD, send users a digital/tokenized dollar, and let them redeem for services, like remittances to Mexico, cloud storage or crypto.

3/ Even with compliance approval, I had to personally zoom with the CEO & President of the bank for final assurances. They wanted to "look me in the eye" and confirm we weren’t doing anything risky. After multiple assurances, we were greenlit to proceed.

4/ We spent months integrating APIs, funding marketing, and preparing for launch. Everything was set. On launch day, after passing UAT with an aggregator, we got a shocking email: "Everest can't go live because your website says you facilitate crypto."

5/ I called compliance. WTF changed? Their response: you are allowing users to purchase crypto. I pointed out nothing had changed since approval. They doubled down, and suddenly, our corp account was shut down. Later, I learned later that the CEO received a call w pressure regarding crypto.

6/ Result?

No US market entry

No Mexico remittances in 90 secs at half the cost of Western Union

No crypto purchases from users' bank accounts

Pushed into crypto winter with only EU market access

$millions in lost opportunity

7/ This isn’t just frustrating—it’s systemic de-banking of a legal business. We were approved, compliant, and transparent. Yet, at the last minute, pressure from the state derailed everything.

#DeBanking #Fintech #Crypto

English

@davidmarcus @bobreideverest @pmarca @joerogan This attitude in response to criticism is why Libra/Diem got shut down

English

@bobreideverest @pmarca @joerogan That whole story you made up in your head is pure fiction. By the time Libra was ready to launch it had more safeguards than any bank enabled payment system in the entire world. Since you’re such an expert, what’s the “catch rate” of illicit activity on existing banking rails?

English

How Libra Was Killed.

I never shared this publicly before, but since @pmarca opened the floodgates on @joerogan’s pod, it feels appropriate to shed more light on this.

As a reminder, Libra (then Diem) was an advanced, high-performance, payments-centric blockchain paired with a stablecoin that we built with my team at @Meta. It would’ve solved global payments at scale. Prior to announcing the project, we spent months briefing key regulators in DC and abroad. We then announced the project in June 2019 alongside 28 companies. Two weeks later, I was called to testify in front of both the Senate Banking Committee and the House Financial Services Committee, which was the starting point of two years of nonstop work and changes to appease lawmakers and regulators.

By spring of 2021 (yes they slow played us at every step), we had addressed every last possible regulatory concern across financial crime, money laundering, consumer protection, reserve management, buffers, and so much more, and we were ready to launch.

We had worked on a slow rollout of a limited pilot that some members of the Fed’s Board of Governors were supportive of. At last, Chair Jay Powell was ready to let us move forward in a limited way. The story, as I heard it, is that Jay Powell was told by Treasury Secretary Janet Yellen at one of their biweekly meetings that allowing this project to move forward was “political suicide,” and she would not have his back if he let it happen. I wasn’t in the room when this conversation happened, so take these words with a grain of salt, but effectively this was the moment Libra was killed.

Shortly thereafter, the Fed organized calls with all the participating banks, and the Fed’s general counsel read a prepared statement to each of them, saying: “We can’t stop you from moving forward and launching, but we are not comfortable with you doing so.” And just like that, it was over.

One essential point is worth making here. There was no legal or regulatory angle left for the government or regulators to kill the project. It was 100% a political kill—one that was executed through intimidation of captive banking institutions. That was the hardest part of this story for me personally. Not that we had failed, but that America, this country I immigrated to and became a proud citizen of because of its rule of law and value system, behaved in such a way for political reasons. It was a very tough pill to swallow.

The bright side of the story, though, was the many learnings from this wild ride. By the end of the project, we had made so many concessions to get a thumbs-up that the whole design of the network became a Frankenstein of our initial ambitions.

We also learned the biggest lesson of all, which is that if you’re trying to build an open money grid for the world—eventually moving trillions of dollars a day, designed to be here 100 years from now—you have to build it on the most neutral, decentralized, unassailable network and asset, which, hands down, is Bitcoin.

And now this is what many of us who went through this scarring journey are building together at @Lightspark. And this time, we won’t stop until we get it done!

English

Neanderthal Respecter retweetledi

1/ I'm proud to have played a small part in ensuring Libra wasn’t approved. While its mission to “bank the unbanked” was admirable, its flawed design posed grave risks: enabling terrorist funding, destabilizing economies, and crippling central banks. Cloaking it as a “de-banked” issue is disingenuous.

2/ Backstory.....When Libra’s whitepaper launched in June 2019, I was working with the IMF, ADB, and central banks in Australia, New Zealand, and Samoa to improve cross-border transfers via stablecoins and identity infrastructure. Within 15 minutes of reading the paper, I flagged 4 fatal flaws.

3/ The issues I raised with @Kiffmeister at the IMF:

Governance: No safeguards on who could join the council. i.e. What happens if CCP-controlled entities buy their way in?

Token Design: A basket currency with unclear tax implications, custody, and legal frameworks.

Identity: Reliance on wallets meant no way to verify users, especially in emerging markets.

Wallet-Based Risk: Any developer could create a wallet, onboard users, and transact—no checks on risk, reporting, or identity.

4/ I continued with John, informing him “the general whitepaper dooms Libra to Dead-on-Arrival. Further, given their lack of identity (ability to verify), especially in emerging markets, Libra’s approval in its current state seems improbable to me…..I kind of hope Zuck goes forward with Libra, as it’ll be easier for me to acquire WhatsApp.)” I also noted it would hobble central banks in smaller economies.

5/ Imagine: Over 50% of Fiji switching to Libra’s token in 3 months. The central bank would be crippled, unable to borrow for schools, roads, or hospitals. Lives would be at risk. This isn’t “go fast and break things”; this is “go fast and break entire countries.”

6/ On July 4th, 2019, I gave John my input to help form the IMF/G7 responses to Libra. He called it “all hands on deck” as the G7 prepared to question the Libra initiative. I believe my feedback shaped some tough, necessary questions. While I admired Libra’s mission, its execution was reckless.

7/ Later, Libra reached out to @EverestDotOrg for help solving its identity issues: they couldn’t deduplicate users from different wallets, nor prove terrorists weren’t transacting. Everest signed an NDA with Libra, but Meta employees joined meetings without NDAs—raising serious red flags. Adding insult to injury, Everest already had the infrastructure, legal standing & license that Libra needed. TBH it was a bit heart-breaking.

8/ At the time, whispers spread that Libra was fishing for startup knowledge, so I stopped communications. Libra later evolved into Diem, fixing earlier flaws (and resembling Everest), but its credibility was irreparably damaged—by its own actions.

9/ The real story of Libra isn’t about “de-banking”; it’s about hubris and a lack of foresight. Starting a transaction network without identity verification? A recipe for disaster. The world rightly pushed back.

10/ Despite everything, I respected Libra’s mission—it mirrored Everest’s own. But the lesson here is clear: Build responsibly. Start with identity. Understand the systems you aim to disrupt. And listen to the people who know.

#Fintech #Crypto #Libra #Diem #Regulation #CrossBorderPayments #everestdotorg

English