Sabitlenmiş Tweet

One condition. No indicator. No parameter to optimize. It filtered 80% of bad trades from a NASDAQ breakout strategy.

The condition: is the high of the entry bar above today's open?

That's it. One line of code.

If yes, the market has been trading above today's open. There's an established uptrend for the day. Enter the long breakout.

If no, the market is below today's open when your signal fires. You're not in an uptrend. You're trading noise. Skip.

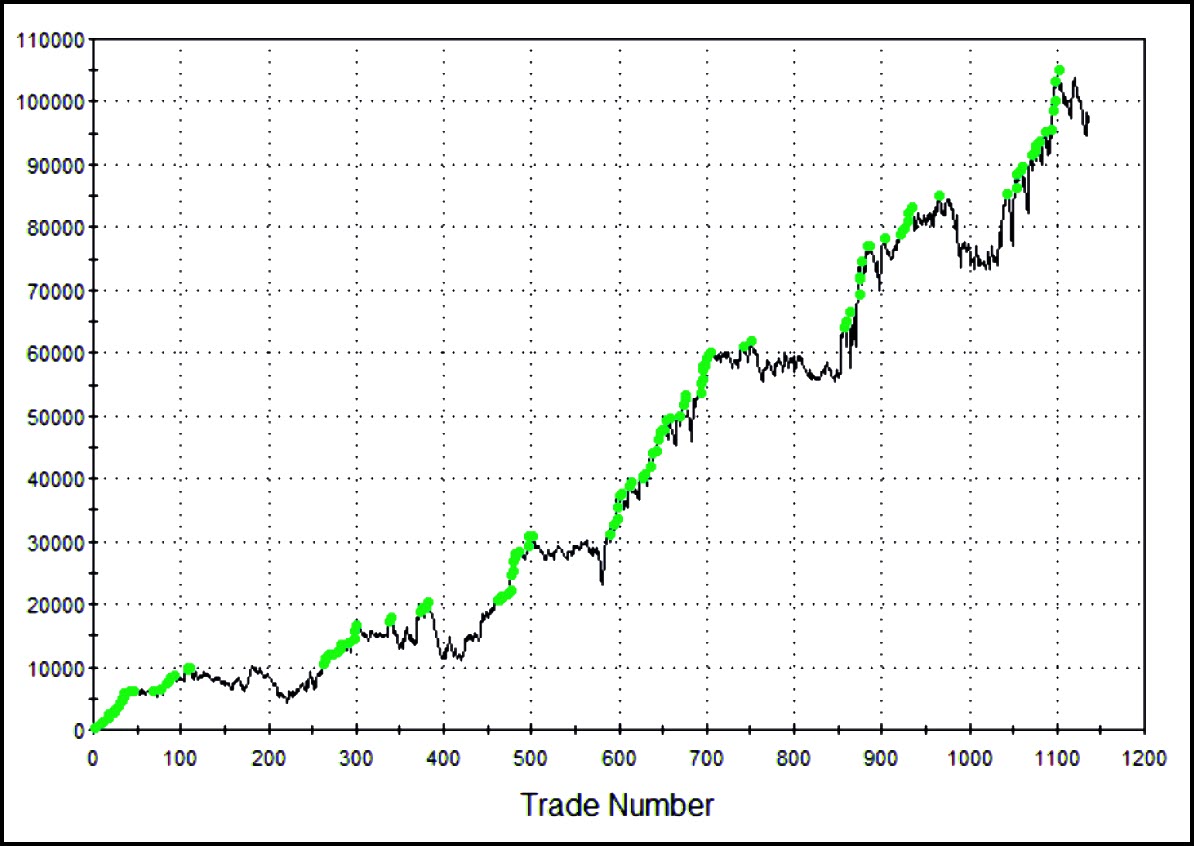

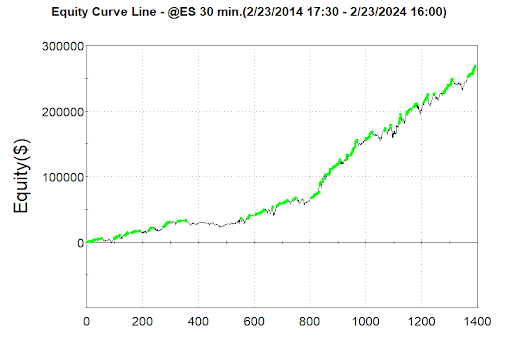

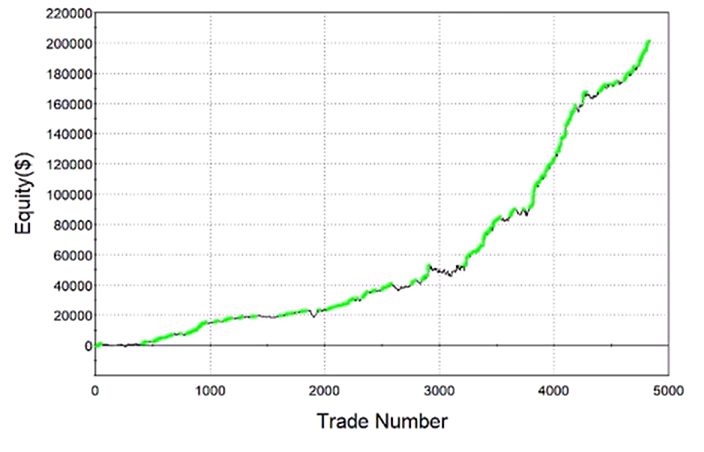

Before:

- Net profit/drawdown ratio: 5.24

- Drawdown: ~$40,000

- Average trade: $120

After:

- Net profit/drawdown ratio: 7.97

- Drawdown: ~$25,000

- Average trade: $162

Net profit went up while drawdown got cut. That's the signature of a genuine filter. It's removing the right trades, not random ones.

Why does it work? Breakout trading is about momentum. If you're buying a breakout to the upside but the market has been trading below its open all day, there's a contradiction. The price level is breaking out, but the day's direction says otherwise. Those trades are the ones that chop you up.

No parameters means no overfitting. This is pure trading logic. You could test it on any long breakout strategy, on any market, in minutes.

The power isn't in complexity. It's in asking the right question.

What's the simplest filter you've ever used?

English